My first post in 2015 focused on three “up & coming” fintech companies: Wealthfront (an automated investment service), Kabbage (an online business loan provider) and Dwolla (a major player in real-time payment processing). Since writing that piece, I’ve kept tabs on their successes while learning about other interesting and compelling businesses in the financial community. So today, five more that I am keen on.

By Al Dominick // @aldominick

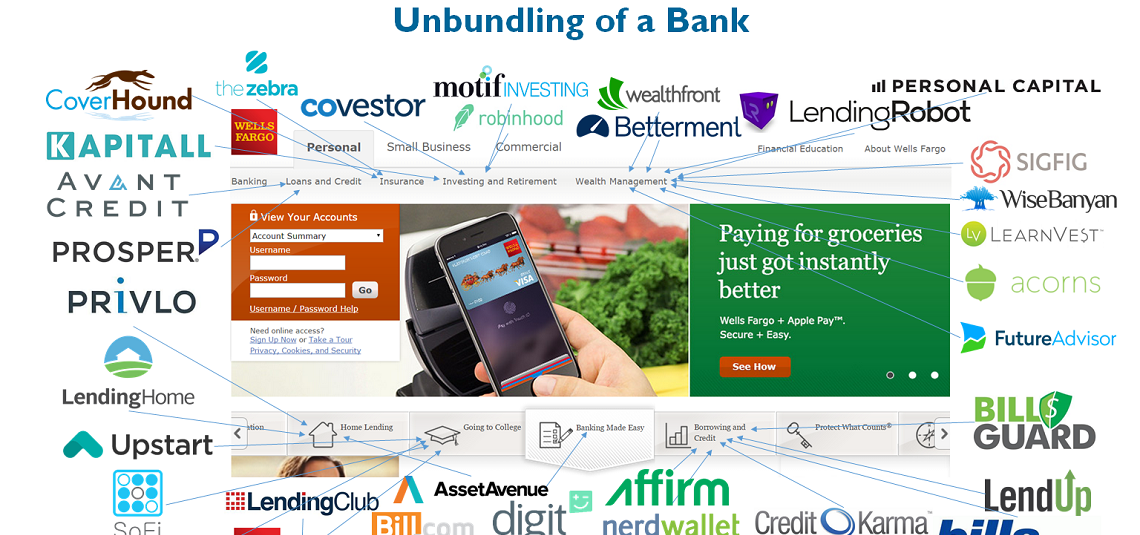

With continuous pressure to innovate, I’m not surprised to see traditional financial institutions learning from new challengers, adapting their offerings and identifying opportunities to collaborate with emerging players. From tokenization to integrated payments, security tools to alternative lending platforms, the investments (and efforts) being made throughout the financial sector continues to impress and amaze me. As I shared in 15 Banks and Fintechs Doing it Right, there are very real and immediate opportunities to expand what banking means to individual and business customers. Personally, I am excited by the work being done by quite a few companies and what follows are five businesses I’ve learned more about while recently traveling between D.C., San Francisco and New York City:

i2c, a global card processing company, provides back-end processing and settlement for cards, virtual accounts and mobile payments. What’s interesting about them? According to a brief shared by Bridge by Deloitte (a web platform connecting enterprises with startups to accelerate innovation and growth), i2c recently teamed up with Oxfam, Visa and Philippines-based UnionBank to channel funds to people in disaster-affected communities through prepaid cards.

With Money20/20 fast approaching, expect to see a lot of #payments trending on twitter. Trending in terms of financial investment: Adyen, a company receiving a lot of attention for wrapping up a huge round of funding that values the payment service provider at $2.3B. Adyen, which provides its services to a number of large organizations including Facebook and Netflix, excels in having a highly integrated platform, unlike others with multiple platforms.

When it comes to technology “powering the new wave of mortgage lending,” take a look at the work being done at BlendLabs. Developing software & data applications for mortgage lenders, the company acknowledges that “accommodating complex rules and regulation changes is time-consuming and costly.” For this reason, the company has quietly rolled out technology that empowers some of the country’s largest lenders to originate mortgages more efficiently and compliantly than ever before while offering their borrowers a more compelling user experience.

As the head of a company, I know first-hand how much time and effort is spent on efforts and ideas designed to maximize revenue and profits. So the promise and premise of nCino is hugely attractive. Co-founded by a fellow W&L grad (and the former CEO of S1) nCino is the leader in cloud banking. With banks like Enterprise in St. Louis (lead by a CEO that I have huge respect for) as customers, take a look at their Bank Operating System, a comprehensive, fully-integrated banking management system that was created by bankers for bankers that sits alongside a bank’s core operating system.

While not solely focused on the financial industry, Narrative Science is a leader in advanced natural language generation. Serving customers in a number of industries, including marketing services, education, financial services and government, their relationship with USAA and MasterCard caught my eye. As FinXTech’s Chief Visionary Officer recently shared with me, the Chicago-based enterprise software company created artificial intelligence that mines data for important information and transforms it into language for written reports.

##

In addition to these U.S.-based companies, you might look at how Fidor, a digital bank in Europe that offers all-electronic consumer banking services, links interest rates to Facebook likes and give cash rewards based on customers’ level of interaction with the bank (e.g. how many customer financial questions answered). Clearly, the fabric of the financial industry continues to evolve as new technology players emerge, institutions like Fidor expand their footprint and traditional participants transform their business models. So if you follow me on twitter (@aldominick), let me know of other fintech companies you’re impressed by these days.

38.976623

-77.056203