On Sunday, January 25, we kick off Bank Director’s 21st annual “Acquire or Be Acquired” Conference (@bankdirector and #AOBA15) at the luxurious Phoenician resort in Scottsdale, Arizona. I am so very excited to be a part of this three day event — and am supremely proud of our team that is gearing up to host more than 800 men and women. With so many smart, talented and experienced speakers on the agenda, let me share a primer on a few terms and topics that will come up. In addition, you will find several links to recent research studies that will be cited before I share one example of the type of issues being both presented and addressed at “AOBA.”

Colorful Language

Just as M&A is a colorful — and complex — issue, so too are the words, terms and considerations used by attorneys, investment bankers and consultants in management meetings, in the boardroom or at the negotiating table. Here are three terms I thought to both share and define in advance of AOBA (ay-o-bah):

- Triangular merger: This happens when the acquirer creates a holding company to acquire the target and both the acquirer and the target become subsidiaries of the holding company.

- Cost of capital: You could say this is the cost to a company of its capital, but another way to look at it simply is this: the minimum return you need to generate for your investors, both shareholders and debt holders. This is what it costs you to operate and pay them back for their investment.

- Fixed exchange ratio: This is the fixed amount for which the seller exchanges its shares for the acquirer’s shares. If the buyer’s stock price falls significantly post-announcement, that could mean the seller is getting significantly less value.

Again, these are but three of the many terms one can expect to hear when it comes to structuring, pricing and negotiating a bank merger or acquisition.

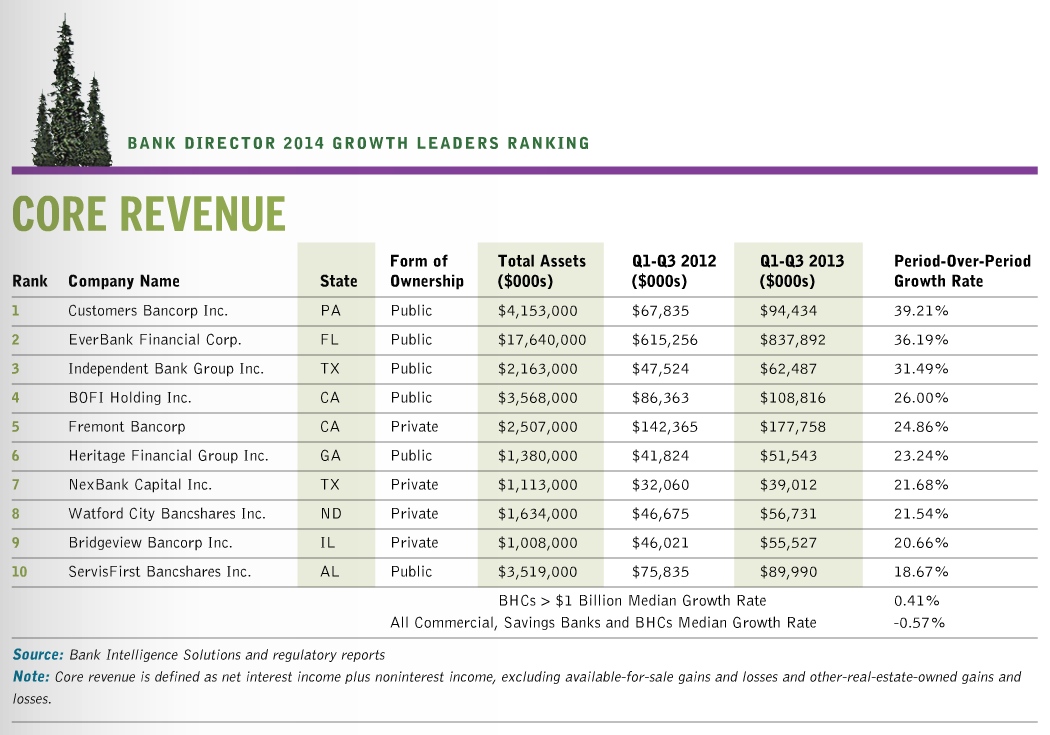

Research Reports

Throughout the year, our team asks officers and directors of financial institutions to share their thoughts on board-specific issues — like growth and more specifically, mergers & acquisitions. Allow me to share an overview on these two research reports along with links to the full results:

- 2014 Growth Strategy Survey (Summary Report)

Of note: 84% of the officers and board members who responded to this Growth Strategy Survey, sponsored by the technology firm CDW, say that today’s highly competitive environment is their institutions’ greatest challenge when it comes to organic growth — a challenge further exacerbated by the increasing number of challengers from outside the industry primed to steal business from traditional banks.

- 2014 Bank M&A Survey (Summary Report)

Of note: There’s no shortage of financial institutions seeking an acquisition in 2015, but fewer banks plan to sell than last year, according to the bank CEOs, senior officers and board members who completed Bank Director’s 2015 Bank M&A Survey, sponsored by Crowe Horwath LLP.

Valuing a Bank

Understanding what one’s bank is really worth today is hugely important. Whether buying, selling or simply growing organically, a bank needs metrics in place to know and grow its valuation. On BankDirector.com this past October, I shared why earnings are becoming more important than tangible book value (Why Book Value Isn’t the Only Way to Measure a Bank). Clearly, a bank that generates greater returns to shareholders is more valuable; thus, the emphasis on earnings and returns rather than book value. Yes, investors and buyers will always use book value as a way to measure the worth of banks. Still, I anticipate conversations at the conference that builds on the idea that as the market improves and more acquisitions are announced, we should expect to see more attention to earnings and price-to-earnings as a way to value banks.

##

Please feel free to comment on today’s piece below or share a thought via Twitter (I’m @aldominick). More to come from the “much-warmer-than-Washingon DC” Arizona desert and Acquire or Be Acquired in the days to come.