Quickly:

- When it comes to talk about bank mergers and acquisitions, It has been written that the questions rarely change — but the conversations prove irresistible.

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

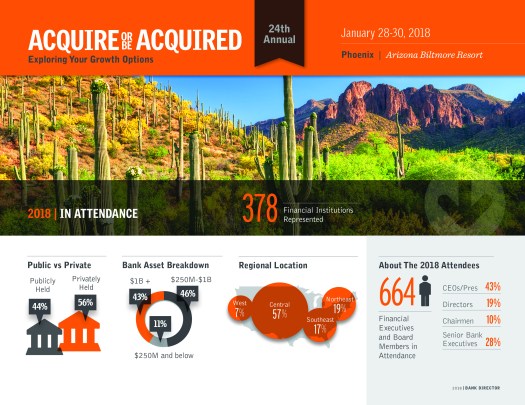

PHOENIX, AZ — If you’re with us here at the Arizona Biltmore for Bank Director’s annual Acquire or Be Acquired Conference, you’ve heard that banks with low‐cost core deposits continue to attract interest from acquirers. So as banks wrestle with increased funding costs, that observation sparked an idea about what constitutes the “three Cs” of banking today:

- Compliance

- Cost Control

- Consolidation

For instance, having good on-going relations with one’s regulators is hugely important. In fact, I heard several prominent attorneys share that regulatory risk remains the greatest obstacle to completing an M&A deal. So having the bank in position to act quickly and confidently when an opportunity arises is a major advantage in today’s competitive M&A environment. I take this to mean no enforcement actions, satisfactory CRA, good HCR results, etc.

As was discussed yesterday afternoon, when an acquirer can present a credible narrative that a potential deal is consistent with a well-considered strategy — and that the company has the infrastructure appropriate to the new organization, you find a well received merger.

In terms of consolidation, we saw a number of presentations note the 261 bank M&A deals, worth an aggregate $26.38 billion, announced in 2017. As a point of reference, 241 deals were announced — worth an aggregate $26.79 billion — in 2016. According to S&P Global Market Intelligence, the median deal value-to-tangible common equity ratio climbed significantly in 2017 to 160.6%, compared to 130.6% for 2016. Last December alone, 32 deals worth a combined $1.84 billion were announced and the median deal value-to-tangible common equity ratio was 156.5%.

Throughout the fourth quarter, there were 74 bank deals announced in the US, which was the most active quarter since 83 deals were announced in the fourth quarter of 2015. However, last quarter’s $4.4 billion aggregate deal value was the lowest since the third quarter of 2015, which totaled $3.43 billion.

These are by no means the only Cs in banking. Credit, core technology providers, (tax) cuts… all, huge issues. So along these lines, I made note of a few more issues for buyers, for sellers — and for those wishing to remain independent. Take a look:

If you are interested in following the final day of the conference via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector, or search #AOBA18 to see what is being shared with (and by) our nearly 1,200 attendees.