Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Last October, I journeyed to Austin, Texas, to watch my first Formula One race. Like many, Netflix’s wildly popular Formula 1: Drive to Survive drew me in. That series dramatically increased the popularity of the sport in the United States, with plenty of drama on track — and off.

Inevitably, the show takes viewers inside a showdown between two cars jostling for points, separated by mere milliseconds.

While being out front has its advantages, so too does drafting your competition. Personally, I love watching/hearing a team’s crew nonchalantly imploring its driver to “push, push… push, push” over the radio. This call to click the push-to-pass mechanism on a race car —which provides a temporary jolt of speed — typically results in the hunter becoming the hunted.

So yes, speed, competition and risk-taking is on my mind as we prepare to host Bank Director’s Experience FinXTech event May 5 and 6 in the same city as the Circuit of The Americas (aka COTA).

Much like Formula One brings some of the most ambitious and creative teams together for a race, Experience FinXTech attracts some of the most inspiring minds from the deeply competitive financial services space.

Now in its seventh year, the event connects a hugely influential audience of U.S. bank leaders with technology partners at the forefront of growth and innovation. Today, as banks continue to transition towards virtual or digital strategies, fintechs become partners rather than just competitors in the race to succeed.

We’ll look not only at fintechs offering efficiencies for banks, but at fintechs offering growth and improved performance as well. As fintech guru Chris Skinner recently noted, “If you only look at technology as a cost reduction process, you never get the market opportunities. If you look at technology as a market opportunity, you get the cost savings naturally as a by-product.”

We’ll consider investor appetites, debate the pros and cons of decentralized finance and share experiences in peer exchanges.

Throughout, we’ll help participants gauge technology companies at a time when new competitors continue to target financial services.

Most Formula One races are won on the margins, with dedicated teams working tirelessly to improve performance. So too are the banks that excel — many of them with dedicated teams working with exceptional partners.

*I am delighted to return to Texas and see so many of my former friends and colleagues at Bank Director. Heck, I’ll tease Naomi Snyder (the editor-in-chief), that I found a way to use my original title for this piece I authored for BankDirector.com.

In addition, I’ll be on stage, rep’ing the team as a member of the company’s board of directors (and as a minority owner), perhaps in boots, maybe without a tie… Saying hello to so many friends from across the industry — like the team at Nymbus who graciously hosted me and some incredibly awesome folks in our industry last October at F1’s COTA race… and yes, flying the skull & crossbones for the team at Cornerstone Advisors.

This is an awesome annual event, and one worth following on social media if you’re unable to join in person. Check out @Fin_X_Tech on Twitter to keep tabs on the provocative conversations that inevitable take place.

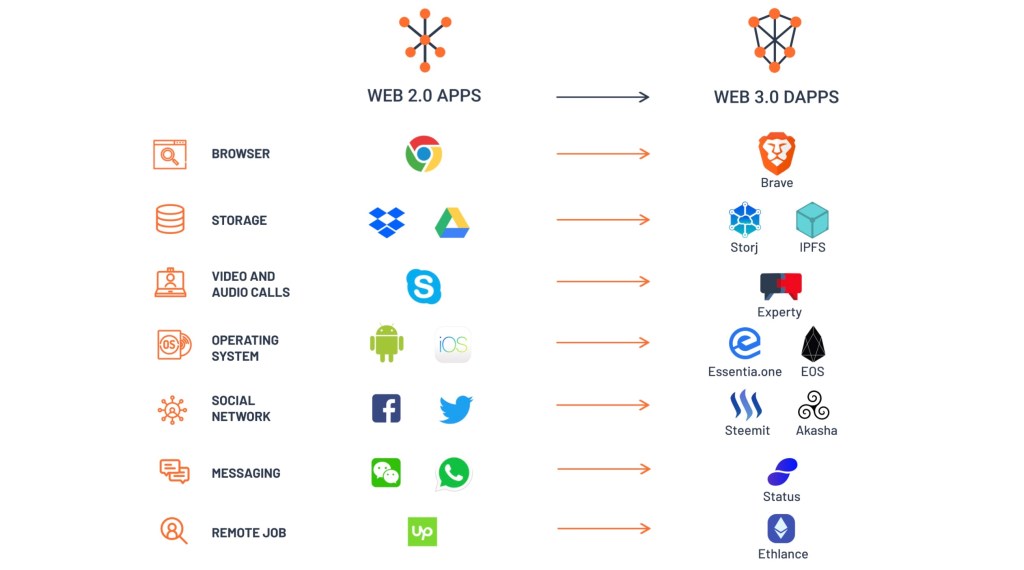

If I’d asked 100 different people at this week’s Acquire or Be Acquired to define DeFi, I’d bet $10,000 worth of ETH I’d get 100 different responses.

As I shared in yesterday morning’s remarks, decentralized finance is a complex area, with interest and usage growing exponentially over the past two years. Many aspects of financial services will be reinvented in a decentralized way — with numerous vendors working on new concepts. Given the current state of bank technology (coupled with a complex regulatory environment), financial markets are riddled with inefficiencies that new companies want to exploit.

Ours is a huge market being transformed by DeFi. But by no means the only industry being impacted. So as we wrap up our time in the Arizona desert, let me re-share one of my slides that shows changes taking place today.

Given the various investments taking place, and developments being announced, I encourage those 1,403 who joined us here to:

— Learn about smart contracts — and how these potentially replace banks and third parties in executing transactions.

— Tackle questions like “what are the benefits of incorporating blockchain technology into my services — and what are the inherent risks?”

— Focus on this year’s “wallet wars;” whereby wallet providers like Kraken, Crypto.com, MetaMask, etc. up their customer experiences to compete for clients.

This year’s event made good on my early prediction that diversification, differentiation and decentralization would be major themes. To the third one, we are just scratching the surface in terms of what’s now — and what’s next.

When Robert Iger joined The Walt Disney Co. as its new CEO in 2005, the company’s storied history of animation had floundered for a decade.

So Iger turned to a competitor whose animation outpaced Disney’s own and proposed a deal.

The relationship between Pixar Animation Studios and Disney had been strained, and Iger was nervous when he called Pixar’s CEO, Steve Jobs.

The two sat down in front of a white board at Pixar’s headquarters and began listing the pros and cons of the deal. The pros had 3 items. The cons had 20, as the now-retired Iger tells it in his this Masterclass online.

“I said ‘This probably isn’t going to happen,’’’ Iger remembers. “He said, ‘Why do you say that?’”

Jobs could see that the pros had greater weight to them, despite the long list of the cons.

Ultimately, Disney did buy Pixar for more than $7 billion in 2006, improving its standing, animation and financial success. In the end, Iger says he “didn’t think it was anything but a risk worth taking.”

I read Iger’s memoir, “The Ride of a Lifetime,’’ in 2021, just as I began planning the agenda for our annual Acquire or Be Acquired Conference in Phoenix. Widely regarded as the premier event for the financial industry’s CEOs, boards and leadership teams, we are preparing to welcome nearly 1,400 to the Arizona desert this weekend. His story resonated, and not just because of the Disney/Pixar transaction.

I thought about that line of risks worth taking… and was reminded of the leadership traits Iger prizes; specifically, optimism, courage and curiosity.

Many of this year’s registered attendees wrestle with the same issues Iger confronted at Disney. They represent important brands in their markets that must respond to the monumental changes in customer expectations. They must attract and retain talent and to grow in the face of challenges.

While some look to 2022 with a sense of apprehension — thanks to Covid variant uncertainty, inflation, supply chain bottlenecks and potential regulatory changes — I feel quite the pep in my step this January.

I celebrate the opportunity with our team to return, in-person, to the JW Marriott Desert Ridge. With so many registered to join us Jan. 30 through Feb. 1, I know I am not alone in my excitement to be with people again in real life.

So what’s in store for those joining us? Conversations around:

Naturally, we discuss the various growth opportunities available to participants. We talk about recent merger transactions, market reactions and integration hurdles. We hear about the importance of marrying bank strategy with technology investment. We explore what’s going on in Washington with respect to regulation, and we acknowledge the pressure to grow earnings and the need to diversify the business.

As the convergence of traditional banking and fintech continues to accelerate, we again offer FinXTech sessions dedicated to delivering growth. We unpack concepts like banking as a service, stablecoins, Web3, embedded finance and open banking.

Acquire or Be Acquired has long been a meeting ground for those that take the creation of franchise value very seriously — a topic even more nuanced in today’s increasingly digital world. The risk takers will be with us, which is great company to keep. Indeed, “there’s no way you can achieve great gains without taking great chances,’’ Iger says. “Success is boundless.”

To follow along with this year’s event, I invite you to bookmark this blog, visit BankDirector.com and search #AOBA22 on LinkedIn and Twitter.

398 banks.

865 bankers.

279 President/CEOs… 54 CEOs… 45 Chairman/CEOs…

1,335 registered attendees (*so far!)

Yes, it is almost time to return to the JW Marriott Desert Ridge in Phoenix, Arizona for Acquire or Be Acquired. In advance, I invite you to “meet” the Bank Director | FinXTech team that’s been working for months on this great event taking place January 30 – February 1.

Earlier this week, I welcomed officers and directors from across the United States to Nashville, TN. From a stage (and not a Zoom), I asked them:

What are your options as we head into the Fall? No, not your personal ability to buy or sell an asset or security. Rather, the options you, as a leaders of your bank, see for the institution you are a part of today?

Strategically speaking, this is a fundamental issue for those in a leadership position to address.

Sure, there are topics that will dominate boardroom discussions — such as diversifying earnings streams and differentiating the bank’s reputation relative to others.

But let me ask you: who are your competitors? By extension, who are the peer groups that you should be basing your performance against? Once answering these, what options do you know are available, right now, that can put space between your bank and their business? Further, what options do you need to create in order to stay both relevant, and competitive in the months ahead?

Creating “optionality” is a concept that continues to rattle around in my mind. Indeed, it ties into the concept of franchise value and is one that members of a bank’s board need to prioritize. It opens conversations around delivery methods and channels, business relationships and partnerships — and yes, growth opportunities (be it organic or through acquisition).

As we talked about in Nashville, banks are under enormous pressure to prepare for an unknown future. Ahead of this year’s exclusive in-person event, I came up with three basic questions I find timely and relevant. Take a read and let me know if you agree.

Last week, I had the pleasure of spending a few minutes with Tom Fitzgerald and Caleb Stevens on their Community Bank Podcast. Produced by SouthState’s Correspondent Division, the two dedicate their pod to helping community bankers grow themselves, their team — and their profits. For about 23 minutes, the three of us explored:

Oh yes, and I botched my ice cream analogy early on. As someone with a sweet tooth, I meant to reference Baskin & Robbins‘ 31 flavors of ice cream while talking leadership characteristics. As a child in Needham, MA, the idea that I’d have to choose between chocolate, coffee, oreo, cookie dough, etc posed a real challenge — especially as we’d go as a post-dentist treat! So when Caleb asks me about key facets of leadership in banking today, please understand my Covid-brain took me back to those fun childhood memories… which is how I wound up bellyflopping on the analogy!!

The premier slugger and center-fielder for the Los Angeles Angels is an eight-time All-Star and three-time American League MVP — winning the award in 2014, 2016, and 2019 while finishing second in the 2012, 2013, 2015 and 2018 votes.

According to ESPN, he’s the best player going into this new season, based on his record for nearly a decade.

So, how did Mike Trout fall to the 25th pick in the Major League Baseball draft in 2009?

Sure, there were some can’t-miss prospects alongside him. The Washington Nationals pegged Stephen Strasburg to be their ace — and selected him with the first pick. He’s no slouch himself — 112 wins, three All-Star games and a World Series title later, the organization has no regrets.

But back in 2009, 24 names were called before Mike Trout, this once in a generation player, heard his. Many of them never reached the majors, let alone Trout’s level.

Professional sports’ drafts are all about taking risks, dreaming big and building for a franchise’s future. These decisions ultimately impact wins, losses and financial futures of organizations for years to come.

For those charged with improving their teams, technology and delivery models, the implications of Mike Trout’s draft should give you pause. With so many technology companies stealing headlines these days, the question about “who’s next” in the financial technology space parallels what baseball teams go through each year.

Ask yourself: How do you and your colleagues look at what’s available? How do you evaluate a future potential fit? How do you commit to another business that can propel you forward, or leave you lamenting what could have been?

So much of a bank’s future depends on its leadership team’s ambition and appetite to take chances today. Inevitably, I find business leaders returning to two basic questions when it comes to a new potential business relationship:

A baseball appears to have two seams; in reality, they’re 216 individual stitches. Similarly for banks, multiple small decisions add up to a big picture.

Just as baseball teams need to be realistic in terms of allocating capital, so do financial institutions when considering their tech spend. No financial services company can choose a relationship that guarantees success.

Like any good general manager, a banking leader needs to prioritize what’s the right fit for the team. Some banks and credit unions may modernize back-office technology, which has the potential to improve efficiency, reduce errors and free up resources for growth. Others may look at solutions that improve customer experiences or drive sales.

Regardless of where you are in your current approach to technology, you need courage to take the first step — and the discipline to take the next. While your team might miss on a Mike Trout, take comfort that there is more than one way to build a team.

Doing your own homework on who’s out there might just net you an MVP.

“Trying to cut your way out of falling profit and revenue is like trying to lift a bucket by standing inside it and pulling up on the handles. It feels like progress but it’s a lot of wasted energy to go nowhere.”

One of the biggest changes, ever, is going on in the financial sector. So I talked with Greg Carmichael, the chairman and CEO of Cincinnati-based Fifth Third Bancorp, about staying relevant and competitive. As the business of banking undergoes significant technological transformation, I found his views on legacy system modernization particularly compelling:

In my experience, many banks are rooted in legacy technology — and just starting out on their multi-year digital / delivery transformation. So as part of Bank Director’s Inspired By Acquire or Be Acquired program on BankDirector.com, we explore this issue in the context of growth options and opportunities. To access this premium content — which includes my full conversation with Greg — register or log-in here.

One sentence on LinkedIn sparked today’s post.

Yes, a comment shared by a fellow W&L alum, Melissa Sawyer, inspired me. She noted:

“Much attention is being paid to the well-orchestrated CEO transitions at Merck and Amazon this week, which reinforce the important role that thoughtful succession planning and good governance play in corporate America.“

A partner in the law firm of Sullivan & Cromwell, I interviewed Melissa as part of our Looking Ahead series in 2019. Since meeting her, I continue to find her perspectives on governance and regulatory issues timely — and spot on.

So when I saw her take on Kenneth Frazier’s and Jeff Bezos’ career decisions this morning, my mind immediately went to a conversation I had with the former CEO of U.S. Bank about his well orchestrated succession plan.

Filmed in advance of our exclusive Inspired By Acquire or Be Acquired “content pop-up,” Richard Davis provided valuable insight into sharing intelligence to build others up. He also explained the steps he took to position his successor, Andy Cecere, for success. Rather than edit my conversation down to just that clip, here is the full conversation between Richard (now President & CEO, Make-A-Wish Foundation of America), and me.

We start by talking about culture, purposes and values (1:21). Next, how industry leaders can inspire the societies and communities they serve (5:06). We talked about laying the foundation for a well received transition (8:20) before exploring the equation IQ+EQ+CQ (12:22). Finally, how companies become places that employees want to work for (15:49).

*Another dot to connect? Our Editor-at-Large, Jack Milligan, talked with the Senior Chairman of Melissa’s law firm, Rodgin Cohen, as part of this digital program. The two explored the heightened cybersecurity threats facing banks today, his outlook for bank M&A in 2021 and how regulation could change under the Biden Administration. For those with access to Inspired By Acquire or Be Acquired’s exclusive digital content, take a look at An Interview with Rodgin Cohen.

WASHINGTON, DC — It turns out, Bono knew something about banking.

Thirty-four years ago, an Irish band came up with an album that sounded revolutionary for its time. U2’s “The Joshua Tree” went on to sell more than 25 million copies, firmly positioning it as one of the world’s best-selling albums. Hits like “I Still Haven’t Found What I’m Looking For” remain in heavy rotation on the radio, television and movies.

Talk about staying relevant. As it turns out, U2 had some wisdom for us all.

Relevance is one of those concepts that drives so many business decisions. For Bank Director, the term carries special importance, as we postpone our annual Acquire or Be Acquired Conference to January 30 through Feb. 1, 2022. In past years, this special event drew more than 1,300 bankers, bank directors and advisors to discuss concepts of relevance and competition in Phoenix.

While we wait for our return to the Arizona desert, we got to work on a new digital offering to fill the sizable peer-insight chasm that now exists.

The result: Inspired By Acquire or Be Acquired.

Think of this as a new pop-up website, one that disappears after a few glorious weeks. Available exclusively on BankDirector.com, this on-demand package consists of timely short-form videos, CEO interviews, live “ask me anything”-type sessions and proprietary research. Topics range from building value to doing a deal, enhancing culture to addressing competition — and yes, technology’s continued impact on our industry.

Everything within this board-level intelligence package provides insight from exceptionally experienced investment bankers, attorneys, consultants, accountants, fintech executives and bank CEOs. So with a nod towards Paul David Hewson (aka Bono) and his bandmates in U2, here’s a loose interpretation of how three of their Joshua Tree songs are relevant to bank leadership teams.

(The question all dealmakers ask themselves.)

Many aspects of an M&A deal are quantifiable: think dilution, valuation and cost savings. But perhaps the most important aspect — whether the deal ultimately makes strategic sense — is not. As regional banks continue to pair off with their peers, I talked with a successful dealmaker, Bryan Jordan, the CEO of First Horizon National Corp., about mergers of equals.

(Banks can help clients when they need it most.)

A flood of new small businesses emerged in 2020. In the third quarter 2020 alone, more than 1.5 million new business applications were filed in the United States, according to the U.S. Census Bureau, nearly double the figure for the same period the year before. Small businesses need help from banks as they wander the streets of their new ventures. So, I asked Dorothy Savarese, the Chair and CEO of Cape Cod 5, how her community bank positions itself to help these new business customers. One part of her answer really resonated with me, as you’ll see in this short video clip.

(Slow to embrace new opportunities? Don’t let this become your song.)

With the rising demand for more compelling delivery solutions, banks continue to find themselves in competition with technology companies. Here, open banking provides real opportunities for incumbents to partner with newer players. Ideally, such relationships provide customers greater ownership over their financial information, a point reinforced by Michael Coghlan, the CEO of BrightFi.

These short videos provide a snapshot of the conversations and presentations that will be available February 4. To find out more about Inspired By Acquire or Be Acquired, I invite you to take a longer look at what’s on our two-week playlist.

Fad diets, self-care recommendations and admonishments to “turn the page.”

We all know what’s coming up in our news feeds. But before we give into these New Year’s cliches, let’s take a minute to appreciate how so many were able to pivot in such unexpected ways.

Knowing that one can successfully change should serve many well in this new year.

While resilience — and perseverance — took center stage in 2020, I find culture, technology and growth showed up in new ways as well.

CULTURE, REVEALED

During the darkest of economic times, I was amazed by examples of creativity, commitment and collaboration to roll out the Small Business Administration’s Paycheck Protection Program. When social issues exploded, proud to see industry leaders stand tall against racism, prejudice, discrimination and bigotry. With work-from-home pressures challenging the concepts of teamwork and camaraderie, delighted by how banks embraced new and novel ways to communicate.

TECHNOLOGY, FIRST

Seeing business leaders share their intelligence and experiences to help build others’ confidence stands out. So, too, does how few shied away from technology, which clearly accelerated the transformation of the financial sector. The rush to digital this spring forced banking leaders to assess their capabilities — and embrace new tools and strategies to “do something more.” As the financial sectors’ technology integration continues, this mindset of finding answers — rather than merely identifying barriers — should benefit quite a few.

GROWTH, POSSIBLE

Many banks considered JPMorgan Chase & Co, Bank of America Corp. and Citigroup as their biggest challenges and competitors entering 2020. Now, I’d wager Venmo, Square and Chime command as much attention. However, competition typically brings out the best in executives; with mergers and acquisitions activity poised to resume and new fintech relationships taking root, growing one’s bank is still possible.

##

So here’s to the optimists. Leaders are defined by their actions, and many deserve to take a well-earned bow for making their colleagues’ and clients’ lives better. While we leave a year marked by incredible unemployment, economic uncertainties and political scars, I’ve found a negative mindset never leads to a happy life. Rather than lament all that went sideways this year, I choose to commemorate the unexpected positives. As I do, I extend my best to you and yours.

With appreciation,

Al

*This reflection also appears in Bank Director’s newsletter, The Slant. A new addition to our editorial suite of products in 2020, I invite you to sign up for this free Saturday newsletter here.