As we talked about at FinTech Day last Tuesday, technology will play a fundamental role in changing the dynamics of banking, be it shining a light on out-dated practices to dramatically enriching the services and experiences being offered to customers.

By Al Dominick, President & CEO, Bank Director

As our editor-in-chief recently wrote, “technology has always been integral to banking, bringing both speed and efficiency to a transaction-intensive business. But in recent years, technology has stepped onto center stage as a prime component in every bank’s growth and distribution strategy. Technology has, in effect, gone from being a way to save money (a crucial function that it still fulfills) to a way to make money. Much of this activity is being driven by the continued growth of mobile and online banking.”

During a panel session entitled “Banking’s New DNA,” I noted how numerous financial technology companies are developing new strategies, practices and products that will dramatically influence the future of banking. Within this period of transformation, where considerable market share is up for grabs, I believe ambitious banks can leapfrog both traditional and new rivals.

I find the narrative that relates to banks and fintech companies has changed from the confrontational talk that existed just a year or two ago. As we found at this year’s FinTech Day in New York City, far more fintech players are expressing their enthusiasm to partner and collaborate with banking institutions who count their strengths and advantages as strong adherence to regulations, brand visibility, size, scale, trust and security. For me, considering such a partnership affords a bank’s leadership team an important chance to look in the mirror and ask:

- Are we exceeding our customer’s digital experience expectations?

- How do we know if we’re staying relevant?

- Do we have a “Department of No” mindset?

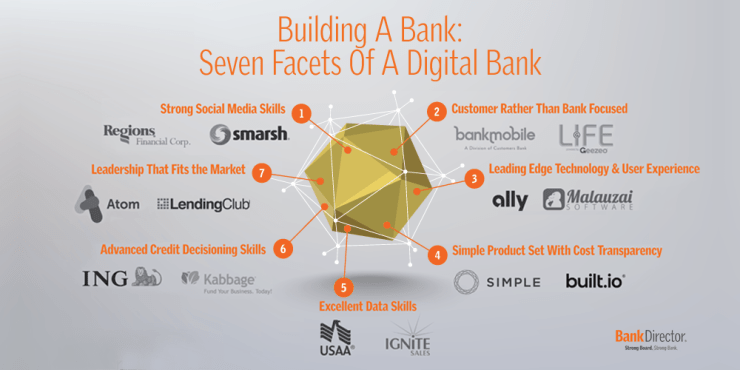

I elaborate on these pieces in an article now up on BankDirector.com; to read it, please click here. Likewise, take a look at the seven facets of building a digital bank. When it comes to the DNA one needs to compete in the future, I find these elements essential to any operation.

Feel free to comment on these questions and the elements shared above. What else do you think could/should be added and considered?