Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Last October, I journeyed to Austin, Texas, to watch my first Formula One race. Like many, Netflix’s wildly popular Formula 1: Drive to Survive drew me in. That series dramatically increased the popularity of the sport in the United States, with plenty of drama on track — and off.

Inevitably, the show takes viewers inside a showdown between two cars jostling for points, separated by mere milliseconds.

While being out front has its advantages, so too does drafting your competition. Personally, I love watching/hearing a team’s crew nonchalantly imploring its driver to “push, push… push, push” over the radio. This call to click the push-to-pass mechanism on a race car —which provides a temporary jolt of speed — typically results in the hunter becoming the hunted.

So yes, speed, competition and risk-taking is on my mind as we prepare to host Bank Director’s Experience FinXTech event May 5 and 6 in the same city as the Circuit of The Americas (aka COTA).

Much like Formula One brings some of the most ambitious and creative teams together for a race, Experience FinXTech attracts some of the most inspiring minds from the deeply competitive financial services space.

Now in its seventh year, the event connects a hugely influential audience of U.S. bank leaders with technology partners at the forefront of growth and innovation. Today, as banks continue to transition towards virtual or digital strategies, fintechs become partners rather than just competitors in the race to succeed.

We’ll look not only at fintechs offering efficiencies for banks, but at fintechs offering growth and improved performance as well. As fintech guru Chris Skinner recently noted, “If you only look at technology as a cost reduction process, you never get the market opportunities. If you look at technology as a market opportunity, you get the cost savings naturally as a by-product.”

We’ll consider investor appetites, debate the pros and cons of decentralized finance and share experiences in peer exchanges.

Throughout, we’ll help participants gauge technology companies at a time when new competitors continue to target financial services.

Most Formula One races are won on the margins, with dedicated teams working tirelessly to improve performance. So too are the banks that excel — many of them with dedicated teams working with exceptional partners.

*I am delighted to return to Texas and see so many of my former friends and colleagues at Bank Director. Heck, I’ll tease Naomi Snyder (the editor-in-chief), that I found a way to use my original title for this piece I authored for BankDirector.com.

In addition, I’ll be on stage, rep’ing the team as a member of the company’s board of directors (and as a minority owner), perhaps in boots, maybe without a tie… Saying hello to so many friends from across the industry — like the team at Nymbus who graciously hosted me and some incredibly awesome folks in our industry last October at F1’s COTA race… and yes, flying the skull & crossbones for the team at Cornerstone Advisors.

This is an awesome annual event, and one worth following on social media if you’re unable to join in person. Check out @Fin_X_Tech on Twitter to keep tabs on the provocative conversations that inevitable take place.

When Robert Iger joined The Walt Disney Co. as its new CEO in 2005, the company’s storied history of animation had floundered for a decade.

So Iger turned to a competitor whose animation outpaced Disney’s own and proposed a deal.

The relationship between Pixar Animation Studios and Disney had been strained, and Iger was nervous when he called Pixar’s CEO, Steve Jobs.

The two sat down in front of a white board at Pixar’s headquarters and began listing the pros and cons of the deal. The pros had 3 items. The cons had 20, as the now-retired Iger tells it in his this Masterclass online.

“I said ‘This probably isn’t going to happen,’’’ Iger remembers. “He said, ‘Why do you say that?’”

Jobs could see that the pros had greater weight to them, despite the long list of the cons.

Ultimately, Disney did buy Pixar for more than $7 billion in 2006, improving its standing, animation and financial success. In the end, Iger says he “didn’t think it was anything but a risk worth taking.”

I read Iger’s memoir, “The Ride of a Lifetime,’’ in 2021, just as I began planning the agenda for our annual Acquire or Be Acquired Conference in Phoenix. Widely regarded as the premier event for the financial industry’s CEOs, boards and leadership teams, we are preparing to welcome nearly 1,400 to the Arizona desert this weekend. His story resonated, and not just because of the Disney/Pixar transaction.

I thought about that line of risks worth taking… and was reminded of the leadership traits Iger prizes; specifically, optimism, courage and curiosity.

Many of this year’s registered attendees wrestle with the same issues Iger confronted at Disney. They represent important brands in their markets that must respond to the monumental changes in customer expectations. They must attract and retain talent and to grow in the face of challenges.

While some look to 2022 with a sense of apprehension — thanks to Covid variant uncertainty, inflation, supply chain bottlenecks and potential regulatory changes — I feel quite the pep in my step this January.

I celebrate the opportunity with our team to return, in-person, to the JW Marriott Desert Ridge. With so many registered to join us Jan. 30 through Feb. 1, I know I am not alone in my excitement to be with people again in real life.

So what’s in store for those joining us? Conversations around:

Naturally, we discuss the various growth opportunities available to participants. We talk about recent merger transactions, market reactions and integration hurdles. We hear about the importance of marrying bank strategy with technology investment. We explore what’s going on in Washington with respect to regulation, and we acknowledge the pressure to grow earnings and the need to diversify the business.

As the convergence of traditional banking and fintech continues to accelerate, we again offer FinXTech sessions dedicated to delivering growth. We unpack concepts like banking as a service, stablecoins, Web3, embedded finance and open banking.

Acquire or Be Acquired has long been a meeting ground for those that take the creation of franchise value very seriously — a topic even more nuanced in today’s increasingly digital world. The risk takers will be with us, which is great company to keep. Indeed, “there’s no way you can achieve great gains without taking great chances,’’ Iger says. “Success is boundless.”

To follow along with this year’s event, I invite you to bookmark this blog, visit BankDirector.com and search #AOBA22 on LinkedIn and Twitter.

Earlier this week, I welcomed officers and directors from across the United States to Nashville, TN. From a stage (and not a Zoom), I asked them:

What are your options as we head into the Fall? No, not your personal ability to buy or sell an asset or security. Rather, the options you, as a leaders of your bank, see for the institution you are a part of today?

Strategically speaking, this is a fundamental issue for those in a leadership position to address.

Sure, there are topics that will dominate boardroom discussions — such as diversifying earnings streams and differentiating the bank’s reputation relative to others.

But let me ask you: who are your competitors? By extension, who are the peer groups that you should be basing your performance against? Once answering these, what options do you know are available, right now, that can put space between your bank and their business? Further, what options do you need to create in order to stay both relevant, and competitive in the months ahead?

Creating “optionality” is a concept that continues to rattle around in my mind. Indeed, it ties into the concept of franchise value and is one that members of a bank’s board need to prioritize. It opens conversations around delivery methods and channels, business relationships and partnerships — and yes, growth opportunities (be it organic or through acquisition).

As we talked about in Nashville, banks are under enormous pressure to prepare for an unknown future. Ahead of this year’s exclusive in-person event, I came up with three basic questions I find timely and relevant. Take a read and let me know if you agree.

Last week, I had the pleasure of spending a few minutes with Tom Fitzgerald and Caleb Stevens on their Community Bank Podcast. Produced by SouthState’s Correspondent Division, the two dedicate their pod to helping community bankers grow themselves, their team — and their profits. For about 23 minutes, the three of us explored:

Oh yes, and I botched my ice cream analogy early on. As someone with a sweet tooth, I meant to reference Baskin & Robbins‘ 31 flavors of ice cream while talking leadership characteristics. As a child in Needham, MA, the idea that I’d have to choose between chocolate, coffee, oreo, cookie dough, etc posed a real challenge — especially as we’d go as a post-dentist treat! So when Caleb asks me about key facets of leadership in banking today, please understand my Covid-brain took me back to those fun childhood memories… which is how I wound up bellyflopping on the analogy!!

“Trying to cut your way out of falling profit and revenue is like trying to lift a bucket by standing inside it and pulling up on the handles. It feels like progress but it’s a lot of wasted energy to go nowhere.”

One of the biggest changes, ever, is going on in the financial sector. So I talked with Greg Carmichael, the chairman and CEO of Cincinnati-based Fifth Third Bancorp, about staying relevant and competitive. As the business of banking undergoes significant technological transformation, I found his views on legacy system modernization particularly compelling:

In my experience, many banks are rooted in legacy technology — and just starting out on their multi-year digital / delivery transformation. So as part of Bank Director’s Inspired By Acquire or Be Acquired program on BankDirector.com, we explore this issue in the context of growth options and opportunities. To access this premium content — which includes my full conversation with Greg — register or log-in here.

WASHINGTON, DC — Five years ago, Bank Director published a special supplement to our quarterly magazine — one dedicated to the intersection of banking and technology. A precursor to our FinXTech efforts, this fifteen-page series of case studies explained advances in technology. All, to help bankers address specific business challenges that remain relevant in 2021.

At the time, financial technology elicited grumbles about disruption or displacement… while sparking interest in new applications for mobile banking. In 2015, 68% of American adults connected to the Internet with smartphones or mobile devices. That figure, courtesy of the Pew Research Center, figures to be much higher today.

Five years ago, banks faced pressures to grow revenue and reduce expenses. Time hasn’t changed that equation for banks.

Certainly, there was, and is, money to be both made and saved in banking. Some of the more ambitious companies, who want to stay relevant and solve their customers’ problems, trimmed expenses while growing revenues.

This supplement provides a fun history lesson as to how they did.

On behalf of our Bank Director | FinXTech team, please enjoy this special historical supplement. You will find certain themes as relevant today as they were when this supplement first mailed.

Fad diets, self-care recommendations and admonishments to “turn the page.”

We all know what’s coming up in our news feeds. But before we give into these New Year’s cliches, let’s take a minute to appreciate how so many were able to pivot in such unexpected ways.

Knowing that one can successfully change should serve many well in this new year.

While resilience — and perseverance — took center stage in 2020, I find culture, technology and growth showed up in new ways as well.

CULTURE, REVEALED

During the darkest of economic times, I was amazed by examples of creativity, commitment and collaboration to roll out the Small Business Administration’s Paycheck Protection Program. When social issues exploded, proud to see industry leaders stand tall against racism, prejudice, discrimination and bigotry. With work-from-home pressures challenging the concepts of teamwork and camaraderie, delighted by how banks embraced new and novel ways to communicate.

TECHNOLOGY, FIRST

Seeing business leaders share their intelligence and experiences to help build others’ confidence stands out. So, too, does how few shied away from technology, which clearly accelerated the transformation of the financial sector. The rush to digital this spring forced banking leaders to assess their capabilities — and embrace new tools and strategies to “do something more.” As the financial sectors’ technology integration continues, this mindset of finding answers — rather than merely identifying barriers — should benefit quite a few.

GROWTH, POSSIBLE

Many banks considered JPMorgan Chase & Co, Bank of America Corp. and Citigroup as their biggest challenges and competitors entering 2020. Now, I’d wager Venmo, Square and Chime command as much attention. However, competition typically brings out the best in executives; with mergers and acquisitions activity poised to resume and new fintech relationships taking root, growing one’s bank is still possible.

##

So here’s to the optimists. Leaders are defined by their actions, and many deserve to take a well-earned bow for making their colleagues’ and clients’ lives better. While we leave a year marked by incredible unemployment, economic uncertainties and political scars, I’ve found a negative mindset never leads to a happy life. Rather than lament all that went sideways this year, I choose to commemorate the unexpected positives. As I do, I extend my best to you and yours.

With appreciation,

Al

*This reflection also appears in Bank Director’s newsletter, The Slant. A new addition to our editorial suite of products in 2020, I invite you to sign up for this free Saturday newsletter here.

WASHINGTON, DC — In 2017, Bank Director magazine featured a story titled “The API Effect.” It showed how banks could earn revenue by using application programming interfaces, or APIs. It considered the pros (and cons) of banks turning themselves into technology platforms. And it concluded with a prediction:

APIs will be so prevalent in five years that banks who are not leveraging them will be similar to banks that don’t offer a mobile banking application.

Less than three years later, the banking industry is on a fast track to proving that hypothesis.

Let’s start with the basics. An application program interface, or API, controls interactions between software and systems. As the American Banker recently shared, “APIs are the glue of the internet and allow digital businesses to interact seamlessly. Banks create a digital-first business model by offering services, such as treasury or loan origination, through APIs in an open-banking system.”

So to help bank executives better understand the promise and potential of APIs, our team developed a special FinXTech Intelligence Report. In it, we explore use cases with a focus on banking, and detail the forces driving adoption of the technology among financial institutions of all sizes.

Divided into five parts, we explore:

— Market trends driving the adoption of APIs;

— Actionable API use cases for growing revenue and creating efficiencies;

— An in-depth case study of TAB Bank, which reimagined its data infrastructure with APIs;

— Key considerations for leadership teams developing an API strategy; and

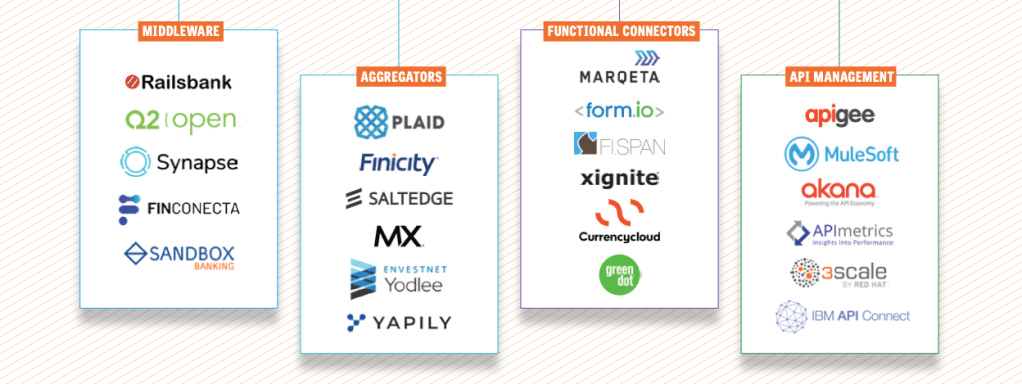

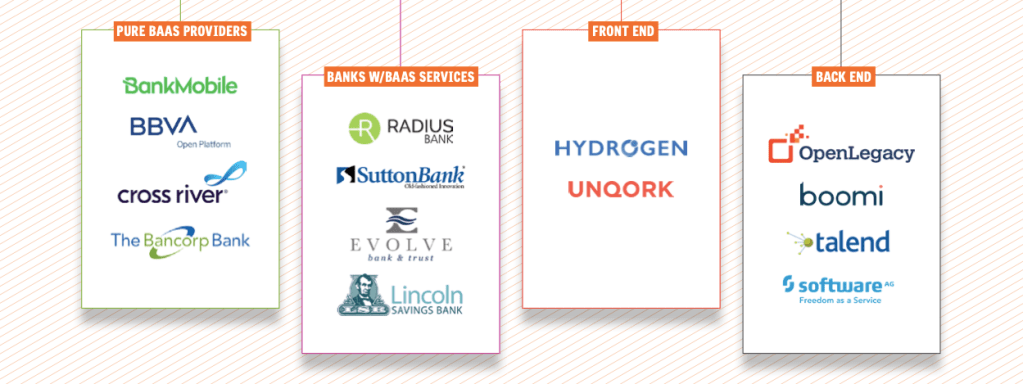

— A map of the API provider landscape, highlighting the leading companies enabling API transformation.

Kudos to the talented Amber Buker for spearheading this effort. As she makes clear, there are several ways for banks to implement APIs. Some will work with their cores (e.g. FIS, Fiserv and Jack Henry) to access the necessary connectivity. Ready-made APIs from fintech providers can quickly address the most common connectivity requirements.

For more complex use cases — like large banks running on old mainframes — the line from systems of record to end users could be longer, with several providers along the path. Regardless of where you are on your journey, understanding the landscape of API providers helps banks get a firmer grasp on the technology and start conceptualizing the scale and design of their potential API project.

To learn more about how banks use APIs, I invited you to download, for free, our FinXTech Intelligence Report, APIs: New Opportunities for Revenue and Efficiency.

WASHINGTON, DC — Last month, our team celebrated ten years of “Bank Director 2.0.” As I look back on what we’ve accomplished, a few projects stand out. Today, I’m shining a light on the development of our FinXTech Platform, which we built specifically for financial institutions.

Bank Director’s FinXTech debuted on March 1, 2016 at Nasdaq’s MarketSite in Times Square. Positioned at the intersection of Financial Institutions and Technology Leaders, FinXTech connects key decision makers across the financial sector around shared areas of interest.

We initially focused on bank technology companies providing solutions geared to Security, leveraging Data + Analytics, making better Lending decisions, getting smarter with Payments, enhancing Digital Banking, streamlining Compliance and/or improving the Customer Experience.

As our brand (and team) grew, we heard from a number of bank executives about the challenges they faced in discovering potential technology partners and solutions. To help solve this issue, we built FinXTech Connect.

Sorting through the technology landscape is no easy feat. Nor is finding, comparing and vetting potential technology partners. But week-by-week, and month-by-month, we added to this proprietary platform by engaging with bankers and fintech executives alike. All the while, asking (whenever we could) bankers who they wanted to learn more about at events like our annual Summit or Experience FinXTech events.

Banks today are in the eye of a digital revolution storm. A reality brought about, in no small part, by this year’s Covid-19 pandemic. So I am proud that the work we do helps banks make smarter business decisions that ultimately help their clients and communities. To wit, the various relationships struck up between banks and fintechs to turn the SBA’s PPP program into a reality.

As we look ahead, I’m excited to see Bank Director’s editorial team continue to carefully vet potential partners with a history of financial performance and proven roster of financial industry clients. For those companies working with financial institutions that would like to be considered for inclusion in FinXTech Connect, I invite you to submit your company for consideration.

WASHINGTON, DC — Since March, I’ve talked with quite a few bank CEOs about their interest in modern and secure technologies. The underlying focus? Improving the experience provided to their customers.

In parallel to such one-on-one conversations, my colleague, Emily McCormick, surveyed 157 independent directors, chief executive officers, chief operating officers and senior technology executives of U.S. banks to understand how technology drives strategy at their institutions — and how those plans have changed due to the Covid-19 pandemic.

She conducted the survey in June and July — and we just released the results in Bank Director’s 2020 Technology Survey, sponsored by CDW. Here are a few key takeaways:

Focus on Experience

Eighty-one percent of respondents say improving the customer experience drives their bank’s technology strategy; 79% seek efficiencies.

Driving the Strategy Forward

For 64% of respondents, modernizing digital applications represents an important piece of their bank’s overall technology strategy. While banks look to third-party providers for the solutions they need, they’re also participating in industry groups (37%), designating a high-level executive to focus on innovation (37%) and engaging directors through a board-level technology committee (35%). A few are taking internal innovation even further by hiring developers (12%) and/or data scientists (9%), or building an innovation lab or team (15%).

Room for Improvement

Just 13% of respondents say their small business lending process is fully digital, and 55% say commercial customers can’t apply for a loan digitally. Retail lending shows more progress; three-quarters say their process is at least partially digital.

Spending Continues to Rise

Banks budgeted a median of $900,000 for technology spending in fiscal year 2020, up from $750,000 last year. But financial institutions spent above and beyond that to respond to Covid-19, with 64% reporting increased spending due to the pandemic.

Impact on Technology Roadmaps

More than half say their bank adjusted its technology roadmap in response to the current crisis. Of these respondents, 74% want to enhance online and mobile banking capabilities. Two-thirds plan to upgrade — or have upgraded — existing technology, and 55% prioritize adding new digital lending capabilities.

Remote Work Permanent for Some

Forty-two percent say their institution plans to permanently shift more of its employees to remote work arrangements following the Covid-19 crisis; another 23% haven’t made a decision.

Interestingly, this survey reveals that fewer banks rely on their core provider to drive their technology strategy. Forty-one percent indicated that their bank relies on its core to introduce innovative solutions, down from 60% in last year’s survey. Sixty percent look to non-core providers for new solutions. Interested to learn more? I invited you to view the full results of the survey on BankDirector.com.

WASHINGTON, DC — The bank M&A market is currently in a deep chill, thanks to the Covid-19 pandemic. It is unclear when deal activity will heat up, so who better to ask than Tom Michaud, the President & CEO, Keefe, Bruyette & Woods, A Stifel Company, as part of Bank Director’s new AOBA Summer Series. In this one-on-one, I ask him about:

There are 10 videos in the AOBA Summer Series, with topics directed at C-suite executives or boards. We talk about how important scale has become, given compressing net interest margins, increasing efficiency ratios and climbing credit costs. We explore why banks’ technology strategy cannot be delegated. We observe why some banks will come out of this experience in a bigger, stronger position. And we look at leadership, appreciating that many executives are leading in new, more positive and impactful ways. To watch, click here.