Just as an Apple store conveys a community and market presence, so too does a bank’s branch. While younger customers may no longer visit more than a front-of-the-house ATM, I do think many of us choose our bank based on their proximity to where we live and work. Today’s tip sheet builds on this thought — beginning with a look at the economics of deposit taking, followed by a visual reminder of our industry’s size before ending with an acquisition by a a big-bank based in Madrid.

Face-to-Face Trumps Technology?

To borrow a few lines from a recent CDW white paper, as the U.S. financial industry emerges from the recent financial crisis, “the surviving institutions are leaner and more focused than ever before. In some cases, this means lowering overhead — doing more with less — to effectively maintain operations.” While the future of banks proved a popular conversation starter during my travels around Washington D.C. and New York City this week, it is a report shared by Fred Cannon — the Director of Research at Keefe, Bruyette and Woods — that caught my eye. I am a big fan of Fred’s prose and the perspectives he offered in “Branch Banking in Retreat” demonstrates that real branch transformation continues to elude many financial institutions. To wit:

“The economics of bank deposit taking is poor in the age of Bernanke and Yellen (low rates) and Durbin (reduced fees). But beyond rates and politics, technology is also undermining the role of traditional branches as the payment system has moved sharply towards electronics in the last decade… Yet, overall banks are responding slowly to the changes in economics and technology of branching. While the number of bank branches has fallen since 2009, the population per branch in the U.S. is still at the same level as the mid-1990s.”

Most branch transformation initiatives I have seen seek to simultaneously reduce costs while improving sales. Here, size matters. Smaller banks can re-invent themselves faster than the big guys; however, its the biggest banks that can financially absorb the most risk in terms of rolling out something new (and expensive).

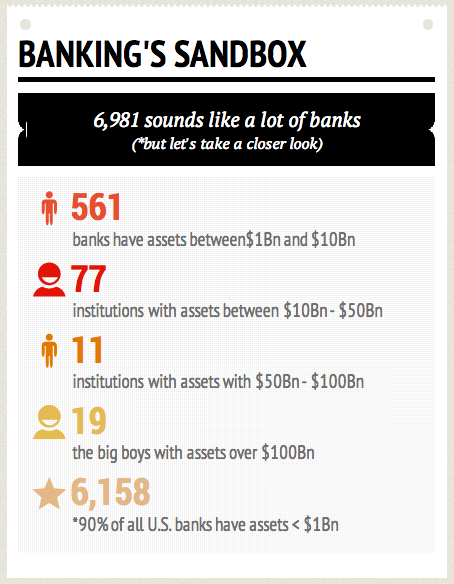

A Visual Reminder That Financial Size Matters

Fred’s research piece, focused on small and mid-sized banks along with the BofA’s and Wells Fargo’s of the country, inspired me to create the following infographic. I’ve shared variations of these statistics in prior posts — and thought to illustrate how our industry breaks down in terms of asset size.

(*note: while I hoped to serve this infographic up in a dynamic way, the image I created from Infogr.am isn’t embedding in WordPress. Still, you get an idea of the market with this screenshot)

Old School Acquires New School

For smaller institutions, the size (and ability to scale) of their larger counterparts can be cause for alarm. Indeed, Accenture shared “becoming a truly digital business is key to how we innovate and differentiate ourselves from our competitors. And if the last decade has been the playground of the digital start-ups, the coming decade will see the emergence of the traditional companies as the digital giants.” I was thinking about this as I read the New York Times’ Dealbook story “BBVA Buys Banking Start-Up Simple for $117 Million.”

This acquisition is notable as the buyer of this upstart is a 150-year old financial services corporation that operates in a number of markets, is a leading player in the Spanish market, as well as one of the top 15 banks in the U.S. and a strategic investor in banks in Turkey and China. As noted by TechCrunch, “while not itself a bank, Simple operates as an intermediary between users and FDIC-insured institutions to provide users with access to data around their financial history, as well as tracking of expenditures and savings goals, with automated purchase data collected when its customers use their Simple Visa debit card.” I wonder if this acquisition starts a consolidation trend of bigger banks buying newer fintech players to accelerate — while differentiating — their offerings…

Aloha Friday!

Reblogged this on Heart of the Matter and commented:

If you can’t beat ’em, join ’em. Al echoes some of my own thoughts on BBVA’s purchase of Simple: Could this start a wave of fintech purchases by big banks?

LikeLike

The Simple purchase by BBVA was not about technology or business model. It was marketing spend by BBVA to get its name into the public sphere (in the US). This is the ONLY way one can justify the purchase price given that the technology is easily cloned and Simple’s customer base is likely of little economic value.

LikeLike

Serge – I initially saw BBVA’s pickup of Simple as a “buy vs. build” decision… thanks for sharing your POV.

LikeLike