WASHINGTON, DC — The bank M&A market is currently in a deep chill, thanks to the Covid-19 pandemic. It is unclear when deal activity will heat up, so who better to ask than Tom Michaud, the President & CEO, Keefe, Bruyette & Woods, A Stifel Company, as part of Bank Director’s new AOBA Summer Series. In this one-on-one, I ask him about:

The banking industry’s second quarter results;

Why bank stocks have not participated in the overall market recovery;

The medium and long term implications of the pandemic on the industry;

The area of Fintech he thinks will be the hottest for the balance of 2020; and

How the November elections might impact the banking industry.

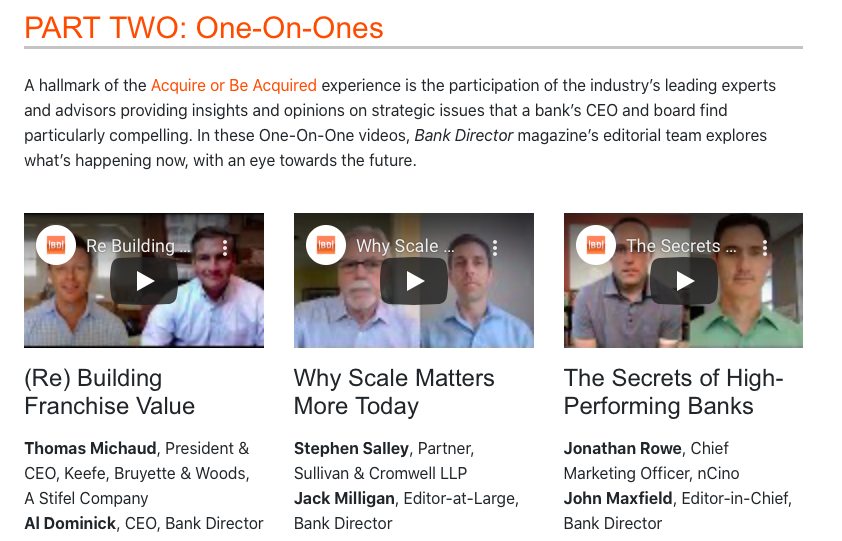

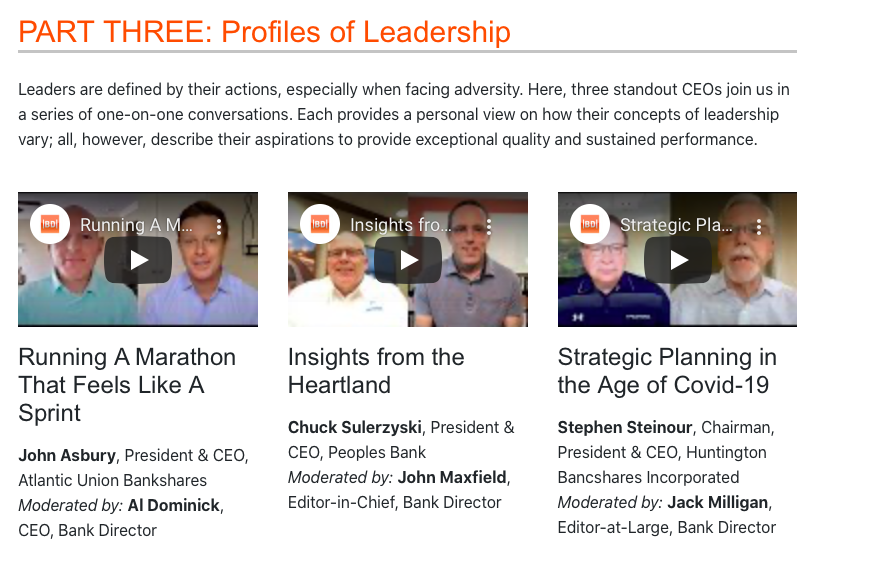

There are 10 videos in the AOBA Summer Series, with topics directed at C-suite executives or boards. We talk about how important scale has become, given compressing net interest margins, increasing efficiency ratios and climbing credit costs. We explore why banks’ technology strategy cannot be delegated. We observe why some banks will come out of this experience in a bigger, stronger position. And we look at leadership, appreciating that many executives are leading in new, more positive and impactful ways. To watch, click here.

Dreaming of a trip to Phoenix, and the Acquire or Be Acquired Conference, next January doesn’t seem so odd this summer.

WORKING FROM HOME — For decades, business leaders began to book their travel to the Arizona desert — for Bank Director’s Acquire or Be Acquired Conference — in early August. As evidenced by the nearly 1,400 at the Arizona Biltmore earlier this year, the annual event has become a true stomping ground for CEOs, executives and board members. Many laud it as the place to be for those that take the creation of franchise value seriously. I’ve even heard it referred to as the unofficial kickoff of banking’s new year.

Just seven months ago, Acquire or Be Acquired once again brought together industry leaders from across the United States to explore merger opportunities, acquisition trends and financial growth ideas. With 418 banks represented, participants considered strategies specific to lending, deposit gathering and brand-building. They talked regulation, met with exceptional fintechs and networked with their peers under sunny skies.

Not one openly worried about a global pandemic.

Yet here we are, all of us dealing with fast-moving challenges and unimaginable risks.

So what can we do to help?

This is the question that proved the catalyst for our new AOBA Summer Series. Indeed, we created this free, on-demand, compilation of thought leadership pieces to provide pragmatic information and real-world insight.

With CEOs and leadership teams being called upon to make decisions they have never been trained for, we realized the type of information typically shared in January has immediate merit this summer. So instead of waiting until winter, this new Summer Series provides both color and context to the tough decisions — those with profound long-term consequences — that confront executives every day.

Ten videos comprise the AOBA Summer Series, with topics appropriate for the C-suite’s or board’s consideration. Streaming on BankDirector.com, we talk about how important scale has become in the banking industry… how one’s technology strategy cannot be delegated… how it certainly seems that there will be banks that come out of this in a bigger, stronger state. Here’s a screen-grab of what you’ll come across:

In one-on-one conversations like these, we acknowledge how net interest margins are compressing — which will drive up efficiency ratios — and credit costs are climbing. And we look at leadership, appreciating that many are leading in new, more positive and impactful ways. In addition, this new series provides:

A SNAPSHOT ON CURRENT CONDITIONS At our January Acquire or Be Acquired Conference, Tom Michaud, President & CEO, Keefe, Bruyette & Woods, A Stifel Company, provided his outlook for the industry. Now, we ask him to update his perspectives on M&A activity and share his take on the potential implications of the pandemic.

HOW FINTECHS FIT A growing number of technology companies have been founded to serve the banking industry. Not all of them have what it takes to satisfy bankers. During various sessions we learn how a variety of banks approach innovation — and the specific attributes a leadership team should look for in a new fintech relationship.

THE LEVERS OF VALUE CREATION With nCino’s CMO, Jonathan Rowe, our Editor-in-Chief talks about the levers of creating value vis-a-vis the flywheel of banking. Together, they explain how certain technologies promote efficiency, which promotes prudence, thereby promoting profits, which can then be invested in technology, starting the cycle all over again.

Hearing from investment bankers, attorneys, accountants, fintechs, investors and — yes, other bankers — about the outlook for growth and change in the industry proves a hallmark for Acquire or Be Acquired, be it in-person or online.

As this new series makes clear, The future is being written in ways unimaginable just a few months ago. We invite you to watch how industry leaders are making sense of the current chaos for free on BankDirector.com.

Large buyers are not in the bank M&A game right now; indeed, banks $25Bn and below continue to drive M&A activity. Case-in-point, 95% of total M&A deals since 2011 have buyer assets less than $25Bn. Might this change in 2018?

PHOENIX, AZ — Michael Porter, the noted economist, researcher and teacher, once said, “strategy is about making choices, trade-offs; it’s about deliberately choosing to be different. The essence of strategy is choosing what not to do. No one can tell you which rules to break, but you can acquire more skill in determining which rules to break given your talents and circumstances right now.”

Porter’s perspectives came back to me while listening to KBW’s CEO, Tom Michaud. Yesterday morning, Tom talked about the strategic paths that a bank’s CEO might consider in the years to come. As he shared, pressure from investors to deploy capital stimulated M&A discussions in 2017 — and will continue to impact deals in 2018. He also noted that pressure placed on deposit costs, as interest rates rise, contributes to the potential acceleration of bank consolidation. These were just two of the many notes I jotted down during the first day of our annual event. Broadly speaking, what I heard fell into five categories:

1. Economic trends

2. Regulatory trends

3. Small business lending trends

4. Management succession trends

5. Technological innovation trends

Many banks enter 2018 with steady, albeit slow loan growth — while recognizing modest margin improvement as they continue to focus on controlling expenses. Accordingly, I thought to elaborate on the issues I found interesting and/or compelling. Feel free to comment below if other points caught your eye or ear.

Economic Trends

FJ Capital authored a piece in late October that noted how, as the Fed progresses further into the tightening phase of the interest rate cycle, banks will find it more difficult to fund loan growth by raising new low‐cost deposits. Their view, which I heard echoed here, is banks with low‐cost core deposits will become more valuable over the next few years as banks wrestle with increased funding costs. In addition to this idea, I made note that banks with a strong deposit base could be more attractive to buyers as interest rates rise. However, a remark I’ve heard at past events re-emerged here. Namely, making a small bank profitable is hard; exiting, even harder.

Regulatory Trends

Given the audience here, I wasn’t surprised by the continued talk of removing the synthetic $10Bn designation. If the Fed, FDIC and OCC raise the $50Bn threshold as spelled out in Dodd Frank, we could see more banks in the $20Bn – $40Bn range come together. Given that large regional banks usually can pay high prices for smaller targets, unleashing this capacity could reignite more M&A and boost community bank valuations. In addition, the Community Reinvestment Act remains a major headwind in bank mergers. Many here want improvements in the CRA process, which in turn could reduce regulatory risk for bank M&A.

Small business lending

When it comes to the lifeblood of most banks — small business lending — a recurring question has been where and how community banks can take market share from larger banks. My two cents: closing loans faster is key, as is structuring loans to fit specific borrower profiles while being supremely responsive to the customer. Oh, and credit is a big theme right now — and the best clients typically have the best credit.

Management succession

An inescapable comment / observation: aging management teams and board members has been a primary driver of bank consolidation of late. I noted that the average age of a public bank CEO and Chairman is 60 and 66, respectively. It was suggested that this demographic alone plays a key factor in the next few year’s consolidation activity.

Technological trends

When it comes to bank mergers, one of the big drivers of deals is the rise in technology-driven competition (*along with regulatory costs and executive-succession concerns). I sense that most traditional banks haven’t really figured out the digital migration process we’ve embraced as a world. Finally, it appears that the biggest banks are winning the war for retail deposits. This is an issue that many management teams and boards should be discussing…

_ _ _

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.

Making banking digital, personalized and in compliance with regulatory expectations remains an ongoing challenge for the financial industry. This is just one reason why a successful merger — or acquisition — involves more than just finding the right cultural match and negotiating a good deal.

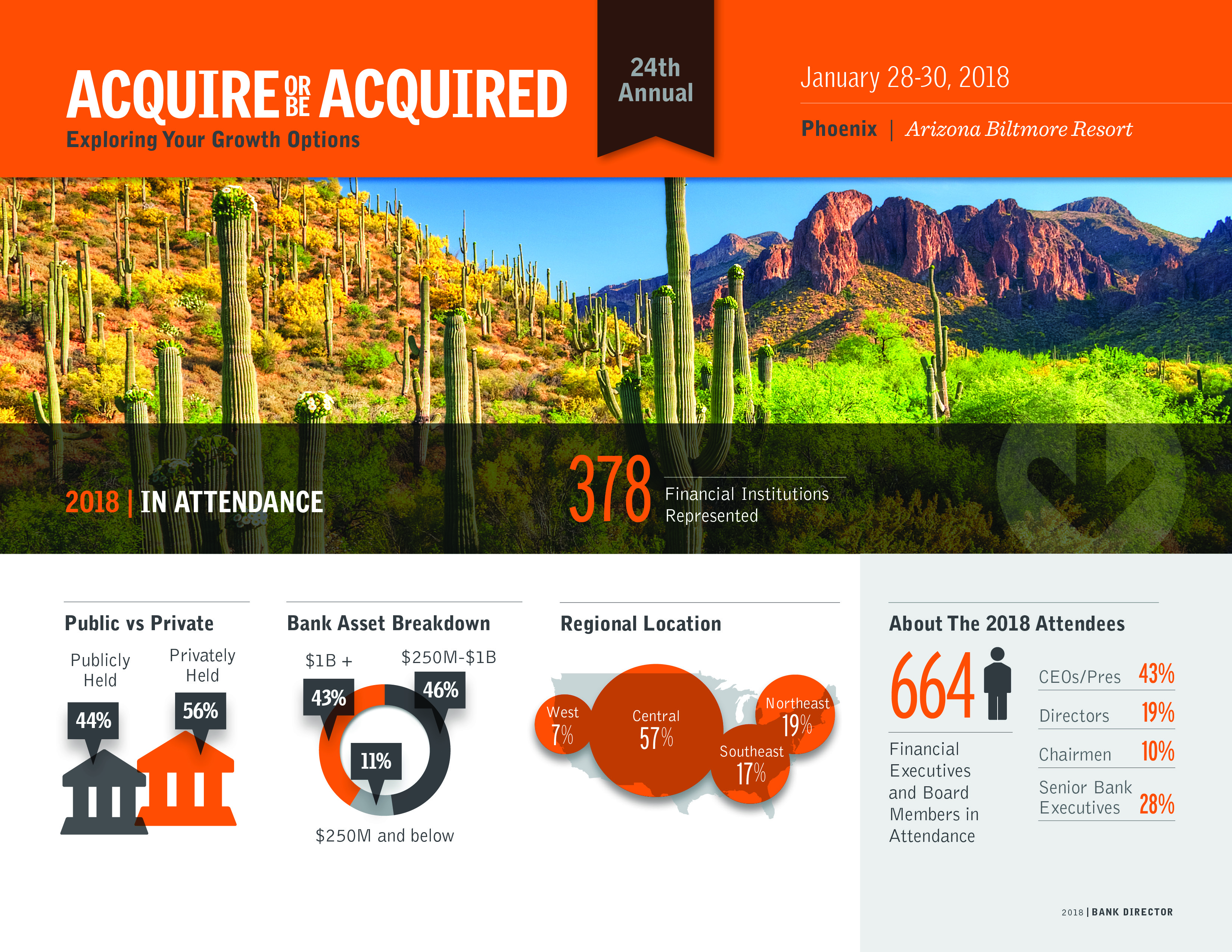

PHOENIX, AZ — As the sun comes up on the Arizona Biltmore, I have a huge smile on my face. Indeed, our team is READY to host the premier financial growth event for bank CEOs, senior management and members of the board: Bank Director’s 24th annual Acquire or Be Acquired Conference. This exclusive event brings together key leaders from across the financial industry to explore merger & acquisition strategies, financial growth opportunities and emerging areas of potential collaboration.

The festivities begin later today with a welcoming reception on the Biltmore’s main lawn for all 1,125 of our registered attendees. But before my team starts to welcome people, let me share what I am looking forward to over the next 72 hours:

Saying hello to as many of the 241 bank CEOs from banks HQ’d in 45 states as I can;

Greeting 669 members of a bank’s board;

Hosting 127 executives with C-level titles (e.g. CFO, CMO and CTO);

Entertaining predictions related to pricing and consolidation trends;

Hearing how a bank’s CEO & board establishes their pricing discipline;

Confirming that banks with strong tangible book value multiples are dominating M&A;

Listening to the approaches one might take to acquire a privately-held/closely-held institution;

Learning how boards debate the size they need to be in the next five years;

Engaging in conversations about aligning current talent with future growth aspirations;

Juxtaposing economic expectations against the possibilities for de novos and IPOs in 2018;

Getting smarter on the current operating environment for banks — and what it might become;

Popping into Show ’n Tells that showcase models for cooperation between banks and FinTechs;

Predicting the intersection of banking and technology with executives from companies like Salesforce, nCino and PrecisionLender;

Noting the emerging opportunities available to banks vis-a-vis payments, data and analytics;

Identifying due diligence pitfalls — and how to avoid them;

Testing the assumption that buyers will continue to capitalize on the strength of their shares to meet seller pricing expectations to seal stock-driven deals;

Showing how and where banks can invest in cloud-based software;

Encouraging conversations about partnerships, collaboration and enablement;

Addressing three primary risks facing banks — cyber, credit and market; and

Welcoming so many exceptional speakers to the stage, starting with Tom Michaud, President & CEO of Keefe, Bruyette & Woods, Inc., a Stifel Company, tomorrow morning.

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.

Nationwide consolidation in the banking space will continue; at least, that is my sense based on conversations and presentations at Crowe Horwath’s Bank Leadership and Profitability Improvement Conference.

_ _ _

So much of this morning was spent talking about growth through mergers and acquisitions (M&A) that I couldn’t help but flash back to January’s Acquire or Be Acquired conference. Thematically, I went into that event expecting the unexpected. Given this morning’s presentations on growing one’s bank, I believe that mindset still holds water.

For example, Tom Michaud, the president and CEO of Keefe, Bruyette & Woods, described 2016 and 2017 as one bumpy ride. From recession fears to lower-for-longer rates, the initial euphoria after the presidential election (at least in terms of stock prices, which went up 27% – 30%) to the uncertainty of regulatory relief, he reminded us of where we are coming from relative to where we might be heading. I am always curious to hear what Tom thinks about the state of banking; below, ten things I learned from him this morning:

The interest rate outlook is a bit cloudier than it was in November;

Regional banks have had excellent earnings per share growth relative to the overall market;

We have an active pace of consolidation — nearly 5% of the industry is merging;

The most prolific acquirers can buy 2, maybe 3 banks, at best each year;

M&A deals are getting bigger — not ’97 or ’98 levels, but bigger than where they’ve been;

Large buyers are not in the game right now — buyers $25Bn and below continue to drive M&A activity (case-in-point, 95% of total M&A deals since 2011 have buyer assets less than $25Bn);

Buyers are completing their acquisitions in 6 months or less;

Banks with strong tangible book value multiples are dominating M&A;

There have been 37 bank IPOs since 2013 — and the market today is open to small bank IPOs; and

Following Tom’s presentation, we doubled down on growing-the-bank type topics with a session involving Rick Childs, a partner at Crowe Horwath, Jim Ryan, the CFO at Old National Bancorp, Jim Consagra, EVP and COO at United Bancshares and Bryce Fowler, chief financial officer at Triumph Bancorp.

From pricing discipline to acquisitions of privately-held/closely-held companies, the guys made clear that “there are only so many deals out there.” They shared how boards need to determine the size they want to be, honestly assess the talent they have relative to such aspirations and determine how growth through M&A aligns with enterprise risk management positioning. Essentially, their remarks made clear that a successful merger or acquisition involves more than just finding the right match and negotiating a good deal.

##

As I shared with yesterday’s post, my thanks to Crowe Horwath, Stifel, Keefe Bruyette & Woods and Luse Gorman for putting together this year’s Bank Leadership and Profitability Improvement Conference at The Inn at Spanish Bay in Pebble Beach, California.

Key takeaways from one of my favorite summer banking events, Crowe Horwath’s Bank Leadership and Profitability Improvement Conference.

_ _ _

This morning, on the first of my two flights from Washington National to Monterey, California, I learned that Walmart customers might soon be able to get installment loans for big-ticket items through Affirm, a San Francisco-based FinTech I first wrote about in 2014 (For Banks, the Sky IS Falling). Per the Wall Street Journal, the companies reportedly are nearing an agreement on a pilot program. This potential partnership caught my eye as I prepared for today and tomorrow’s conference. Indeed, relationships like these make clear that when it comes to growth and efficiency, the digital distribution of financial goods and services is a significant issue for the banking industry.

This idea took further shape when I walked into the conference center at the Inn at Spanish Bay. Immediately upon entering the room, I found John Epperson, a partner at Crowe and Jay Tuli, senior vice president retail banking and residential lending at Leader Bank, sharing their opinions on partnership strategies involving banks and FinTechs. From the stage, they touched on increasing net interest margins via improved pricing strategies on commercial loans, approaches to streamline mortgage application processes, ideas to reduce staff counts for loan administration processes and how to improve customer experiences through online rent payment solutions.

Their perspectives lined up with those we recently shared on BankDirector.com. To wit, “many banks have realized advantages of bank-FinTech partnerships, including access to assets and customers. Since most community banks serve discreet markets, even a relatively simple loan purchase arrangement can unlock new customer relationships and diversify geographic concentrations of credit. Further, a FinTech partnership can help a bank serve its legacy customers; for instance, by enabling the bank to offer small dollar loans to commercial customers that the bank might not otherwise be able to efficiently originate on its own.”

Of all the difficult issues that bank leadership must deal with, I am inclined to place technology at the top of the list. Banks have long been reliant on technology to run their operations, but in recent years, technology has become a primary driver of retail and small business banking strategy. John and Jay simply reinforced this belief.

In addition to their thoughts on collaboration, this afternoon’s sessions focused on ‘Liquidity and Balance Sheet Management,’ ‘Fiscal Policy During Regulatory Uncertainty’ and ‘Managing Your Brand in a Digital World.’ While I took note of a number of issues, three points really stood out:

Yes, banks can make money while managing decreasing margins and a flat yield curve.

Asset growth without earnings growth is a concern for many because of loan pricing.

How a CFO sets a target(s) for interest rate risk may start with an “it depends” type response — but gets nuanced quickly thereafter.

Finally, I’m not holding my breath on the industry receiving regulatory relief any time soon. I get the sense many here aren’t either. But it would be nice to see some business people brought in to run various agencies and I’m looking forward to the perspectives of tomorrow’s first guest speaker, Congressman John Ratcliffe.

##

My thanks to Crowe Horwath, Stifel, Keefe Bruyette & Woods + Luse Gorman for putting together this year’s Bank Leadership and Profitability Improvement Conference at The Inn at Spanish Bay in Pebble Beach, California. I’ll check in with additional takeaways based on tomorrow’s presentations.

We could see over 200 merger transactions despite a declining number of banks in 2017.

There is a clear trend on M&A pricing multiples being driven by bank profitability and asset quality.

For banks, too little capital is not the only issue — too much capital and the inability to produce sufficient returns on capital is equally problematic.

_ _ _

What is my bank worth? How will the changing tax environment affect bank values? When is the right time to buy (or sell) a bank? What are the most significant factors affecting bank value? These were just some of the questions surfaced this morning here in Arizona. In this video recap of Sunday morning’s presentations at Bank Director’s Acquire or Be Acquired Conference, I share a few observations about the conversations taking place around issues such as these.

Given the focus of this three-day event, I anticipate many subsequent presentations building off of these points. For those interested in issues such as these, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and its @Fin_X_Tech platform, and search & follow #AOBA17 to see what is being shared with (and by) our attendees.

In just 20 days, we raise the lights on our 23rd annual Acquire or Be Acquired Conference. This is Bank Director’s biggest event of the year, one primarily focused on banking’s “great game” — mergers and acquisitions. My team has spent considerable time and energy developing a spectacular event focused on growth-related topics that range from exploring a merger to preparing for an acquisition; growing loans to capturing efficiencies; managing capital to partnering with fintech companies. To see the full agenda, click here.

Widely regarded as one of the banking industry’s premier events, we have more than 1,000 people registered to attend AOBA later this month — an all-time high. We couldn’t do this alone, and over the course of these 2 ½ days, executives from many of our industry’s leading professional services firms and product companies share their perspectives on “what’s now” and “what’s next.” I invite you to take a look at all of the corporate sponsors joining us:

As I shared in a recent post, bank executives and their boards face some major issues without clear answers. Before heading out west, I’ll share more about the banks (and 660+ bankers) joining us at the JW Marriott Phoenix Desert Ridge Resort & Spa. Until then, I invite you to learn more about the companies supporting this conference by hopping over to bankdirector.com. To follow the conversations happening around this conference on Twitter, I’m @aldominick and we are using #AOBA17.

I am in Seattle to host a peer exchange at the Four Seasons — one focused on emerging legal, regulatory and risk issues facing members of the board of financial institutions. As eager as I am to welcome participants to this beautiful property and city, I have to admit that my attention this morning centers on M&A in the fintech space (thanks to this piece I authored for BankDirector.com). So before the day ramps up, I thought to re-post my perspectives on interesting deals that are reshaping banking.

It’s no secret that what has been happening in the fintech space is attracting more attention from the world of banking. It’s hard to ignore the fact that venture capital invested $10 billion in fintech startups in 2014, compared to just $3 billion in 2013, according to an Accenture analysis of CB Insights data. But watching M&A in the fintech space shows that these startups are much more likely to pair with others or get acquired by incumbents than they are to go public with an initial public offering, as noted by bank analyst Tai DiMaio in a KBW podcast recently. “Together, through partnerships, acquisitions or direct investments, you can really have a situation where both parties benefit [the fintech company and the established player],’’ he says. That may lend credence to my initial suspicions that there are more opportunities in fintech for banks than threats to established players and that these startups really need to pair up to be successful.

Take BlackRock’s announcement in August that it will acquire FutureAdvisor, a leading digital wealth management platform with technology-enabled investment advice capabilities (a so-called “robo advisor.”) With some $4.7 trillion in assets under management, BlackRock offers investment management, risk management and advisory services to institutional and retail clients worldwide—so this deal certainly caught my attention.

According to FT Partners, the investment bank that served as exclusive advisor to BlackRock, the combination of FutureAdvisor’s tech-enabled advice capabilities with Blackrock’s investment and risk management solutions “empowers partners to meet the growing demand among consumers to engage with technology to gain insights on their investment portfolios.” This should be seen as a competitive move to traditional institutions, as demand for such information “is particularly strong among the mass-affluent, who account for ~30 percent of investable assets in the U.S.”

Likewise, I am constantly impressed with Capital One Financial Corp., an institution that has very publicly shared its goal of being more of a technology company than a bank. To leapfrog the competition, Capital One is quite upfront in their desire to to deliver new tech-based features faster then any other bank. As our industry changes, the chief financial officer, Rob Alexander, opines that the winners will be the ones that become technology-focused businesses—and not remain old school banking companies. This attitude explains why Capital One was the top performing bank in Bank Director’s Bank Performance Scorecard this year.

Case-in-point, Capital One acquired money management app Level Money earlier this year to help consumers keep track of their spendable cash and savings. Prior to that, it acquired San Francisco-based design firm Adaptive Path “to further improve its user experience with digital.” Over the past three years, the company has also added e-commerce platform AmeriCommerce, digital marketing agency PushPoint, spending tracker Bundle and mobile startup BankOns.

When they aren’t being bought by banks, some tech companies are combining forces instead. Envestnet, a Chicago-based provider of online investment tools, acquired a provider of personal finance tools to banks, Yodlee, in a cash-and-stock transaction that valued Yodlee at about $590 million. By combining wealth management products with personal financial management tools, you see how non-banks are taking steps to stay competitive and gain scale.

Against this backdrop, Prosper Marketplace’s tie up with BillGuard really struck me as compelling. As a leading online marketplace for consumer credit that connects borrowers with investors, Prosper’s acquisition of BillGuard marked the first time an alternative lender is merging with a personal financial management service provider. While the combination of strong lending and financial management services by a non-bank institution is rare, I suspect we will see more deals like this one struck between non-traditional financial players.

There is a pattern I’m seeing when it comes to M&A in the financial space. Banks may get bought for potential earnings and cost savings, in addition to their contributions to the scale of a business. Fintech companies also are bought for scale, but they are mostly bringing in new and innovative ways to meet customers’ needs, as well as top-notch technology platforms. They often offer a more simple and intuitive approach to customer problems. And that is why it’s important to keep an eye on M&A in the fintech space. There may be more opportunity there than threat.

I mentioned this from the stage earlier today… every January, Bank Director hosts a huge event in Arizona focused on bank mergers and acquisitions. Known as “AOBA,” our Acquire or Be Acquired conference has grown significantly over the years (this year, we welcomed some 800 to the desert). After the banking M&A market tumbled to a 20-year low in 2009 of just 109 transactions, it has gradually recovered from the effects of the crisis. In fact, there were 288 bank and thrift deals last year, which was a considerable improvement on volume of 224 deals in 2013. As our editorial team has noted, the buying and selling of banks has been the industry’s great game for the last couple of decades, but it’s a game that not all banks can — or want to — play. Indeed, many bank CEOs have a preference to grow organically, and its to these growth efforts that we base today and tomorrow’s program.

Key Takeaway

To kick things off, we invited Fred Cannon, Executive Vice President & Director of Research at KBW, to share his thoughts on what constitutes franchise value. While he opened with a straight-forward equation to quantify franchise value over time — (ROE – Cost of Equity) × Market Premium — what really stuck with me during his presentation is the fact that a logo does not create franchise value, a brand does. As he made clear, it is contextual (e.g. by industry’s served, technologies leveraged and clients maintained) and requires focus (e.g. you can’t be all things to all people). Most notably, small and focused institutions trump small and complex ones.

Trending Topics

Anecdotally, the issues I took note of where, in no particular order:

Banks must be selective when integrating new technology into their systems.

The ability to analyze data proves fundamental to one’s ability to innovate.

When it comes to “data-driven decisions,” the proverbial life cycle can be thought of as (1) capture (2) store (3) analyze (4) act.

You don’t need a big deposit franchise to be a strong performing bank (for example, take a look at County Bancorp in Wisconsin)

We’ve heard this before, but size does matter… and as the size of bank’s balance sheet progresses to $10 billion, publicly traded banks generate stronger profitability and capture healthier valuations.

Picked Up Pieces

A really full day here in New Orleans, LA — with quite a few spirited discussions/debates. Here are some of the more salient points I made note of throughout the day:

Selling services to large, highly regulated organization is a real challenge to many tech companies.

Shadow banking? Maybe its time I start calling them “Challenger banks.”

A few sidebar conversations about Wells Fargo’s incubator program, which the San Francisco bank began last August… interest in how the program involves direct investment in a select group of startups and six months of mentoring for their leaders.

To see what’s being written and said here in New Orleans, I invite you to follow @bankdirector, @aldominick + #BDGrow15.

As you probably deduced from the picture above, I’m in Chicago for Bank Director’s annual Chairman & CEO Peer Exchange. While the conversations between peers took place behind closed doors, we teed things up with various presentations. An early one — focused on FinTech — inspired today’s post and this specific question: as a bank executive, what do you get when you add these three variables:

Stricter capital requirements (which reduces a bank’s ability to lend) + Increased scrutiny around “high-risk” lending (decreasing the amount of bank financing available) + Increases in consumer product pricing (say goodbye to price-sensitive customers)

The unfortunate answer?

Opportunity; albeit, for non-bank financial services companies to underprice banks and take significant business from traditional players. Nowhere is this more clear then in the lending space. Through alternative financial service providers, borrowers are able to access credit at lower borrowing costs. So who are banks competing with right now? Here is but a short list:

FastPay, who provides specialized credit lines to digital businesses as an advance on receivables.

Kabbage, a company primarily engaged in providing short-term working capital and merchant cash advance.

OnDeck, in business to provide inventory financing, medium-term business loans.

Realty Mogul, a peer-to-peer real estate marketplace for accredited investors to invest in pre-vetted investment properties.

BetterFinance, which provides short-term loans for consumers to pay monthly bills and purchase smartphones.

Lenddo, an online platform that utilizes a borrower’s social network to determine credit-worthiness.

Lendup, a short-term online lender that seeks to help consumers establish credit and avoid the cycle of debt.

Prosper, an online marketplace for borrowers to create and list loans, with retail and institutional investors funding the loans.

SoFi, an online network helping recent graduates refinance student loans through alumni network.

As unregulated competition heats up, bank CEOs and Chairmen continue to seek ways to not just stay relevant but to stand out. Unfortunately, the math isn’t always in their favor, especially when alternative lenders enjoy operating costs far below banks and are not subject to the same reserve requirements as an institution. As we were reminded, consumers and small businesses don’t really care where they borrow money from, as as long as they can borrow the money they want.

##

Thanks to Halle Benett, Managing Director, Head of Diversified Financials Investment Banking, Keefe, Bruyette & Woods, A Stifel Company for inspiring this post. He joined us yesterday morning at the Four Seasons Chicago and laid out the fundamental shifts in banking that have opened the door for these new competitors. I thought the math he shared with the audience was elegant both in its simplicity — and profound in its potential results. Let me know what you think with a comment below or message via Twitter (@aldominick).

To kick things off today, we took a look at those banks reshaping the banking industry. With M&A providing an avenue for banks to drive improved operating leverage, earnings, efficiency and scale, we focused on the emergence of mid-sized regional banks that are growing through the consolidation of smaller banks. My thanks to Jack Kopnisky, President & CEO, Sterling National Bank & Sterling Bancorp (NYSE: STL), Ben Plotkin, Vice Chairman of the Board, Stifel Financial Corp (NYSE: SF) and Frank Sorrentino, Chairman & CEO, ConnectOne Bank (NASDAQ: CNOB) for sharing their time and opinions in their session entitled “The New” Consolidators this morning.