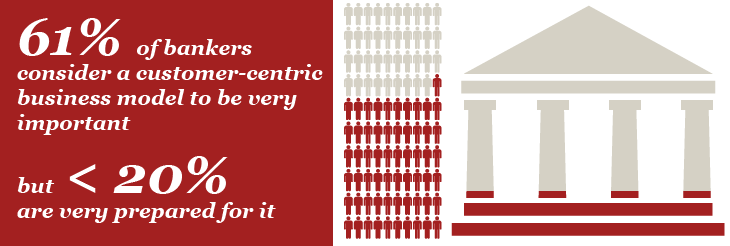

With continuous pressure on bankers to grow earnings, developing clear strategies, repeatable practices and incorporating exceptional user-experience technologies has to be high on almost every executives to-do list.

How do you bank?

By taking a pause before answering this question, you will appreciate how, regardless of age, we all expect greater pricing transparency, ease of use and always-on access to personal information as part of an integrated banking experience. The challenge for most bankers? What many consider state-of-the-art today — in terms of features and services — quickly becomes part of the norm that will be expected and insisted upon in the coming years.

At this morning’s Growing the Bank Conference, I jotted down a few thoughts that builds on this “how do you bank” query.

- When it comes to the classic build or buy technology decision, partnerships are now de rigueur — with 87% of our 240+ person audience indicating they see technology as presenting opportunities to banks (and not threats).

- Historically, banks organize themselves along a line of products; however, many have suggested re-orienting operations around customer needs and expectations.

- To retain deposits, banks should ramp up their customer relationship programs, increase cross-selling efforts and invest in product lines that attract stable deposits.

While we haven’t gotten deep into the payments space (yet), I do encourage bank executives to think about the dramatic growth in that area of banking — which continues to transform how efficiently banks connect with their customers. Likewise, I wasn’t kidding when I suggested attendees spend some time reading the OCC’s “Supporting Responsible Innovation” white paper.

Finally, a “did-you-know” that I meant to share from the stage during my conversation with Brian Read, Executive Vice President, Retail Banking, Umpqua Holdings Corp. and Umpqua Bank. According to the Federal Reserve, 85% of mobile banking users — a bank’s “most advanced” clients — still use branches from time to time. So as he shared with us, there really is a place for a physical presence in banking today.

##

*FWIW, we’re in Dallas at the Four Seasons Resort and Club Las Colinas in Dallas, Texas where the annual Byron Nelson golf tournament wrapped up yesterday evening. The picture above is of Jordan Spieth — the former number one player in the Official World Golf Ranking and two-time major winner — a gift to some of my team who were intent on getting a photo of him. As a former student of St. Marks, I will not hold it against him that he went to Jesuit, a rival high school.