Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

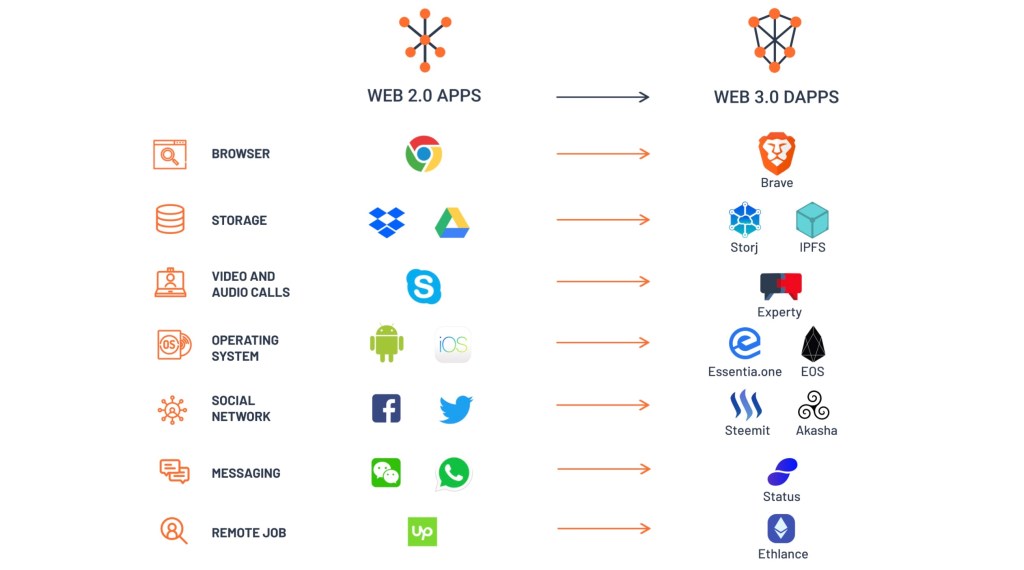

If I’d asked 100 different people at this week’s Acquire or Be Acquired to define DeFi, I’d bet $10,000 worth of ETH I’d get 100 different responses.

As I shared in yesterday morning’s remarks, decentralized finance is a complex area, with interest and usage growing exponentially over the past two years. Many aspects of financial services will be reinvented in a decentralized way — with numerous vendors working on new concepts. Given the current state of bank technology (coupled with a complex regulatory environment), financial markets are riddled with inefficiencies that new companies want to exploit.

Ours is a huge market being transformed by DeFi. But by no means the only industry being impacted. So as we wrap up our time in the Arizona desert, let me re-share one of my slides that shows changes taking place today.

Given the various investments taking place, and developments being announced, I encourage those 1,403 who joined us here to:

— Learn about smart contracts — and how these potentially replace banks and third parties in executing transactions.

— Tackle questions like “what are the benefits of incorporating blockchain technology into my services — and what are the inherent risks?”

— Focus on this year’s “wallet wars;” whereby wallet providers like Kraken, Crypto.com, MetaMask, etc. up their customer experiences to compete for clients.

This year’s event made good on my early prediction that diversification, differentiation and decentralization would be major themes. To the third one, we are just scratching the surface in terms of what’s now — and what’s next.

Fad diets, self-care recommendations and admonishments to “turn the page.”

We all know what’s coming up in our news feeds. But before we give into these New Year’s cliches, let’s take a minute to appreciate how so many were able to pivot in such unexpected ways.

Knowing that one can successfully change should serve many well in this new year.

While resilience — and perseverance — took center stage in 2020, I find culture, technology and growth showed up in new ways as well.

CULTURE, REVEALED

During the darkest of economic times, I was amazed by examples of creativity, commitment and collaboration to roll out the Small Business Administration’s Paycheck Protection Program. When social issues exploded, proud to see industry leaders stand tall against racism, prejudice, discrimination and bigotry. With work-from-home pressures challenging the concepts of teamwork and camaraderie, delighted by how banks embraced new and novel ways to communicate.

TECHNOLOGY, FIRST

Seeing business leaders share their intelligence and experiences to help build others’ confidence stands out. So, too, does how few shied away from technology, which clearly accelerated the transformation of the financial sector. The rush to digital this spring forced banking leaders to assess their capabilities — and embrace new tools and strategies to “do something more.” As the financial sectors’ technology integration continues, this mindset of finding answers — rather than merely identifying barriers — should benefit quite a few.

GROWTH, POSSIBLE

Many banks considered JPMorgan Chase & Co, Bank of America Corp. and Citigroup as their biggest challenges and competitors entering 2020. Now, I’d wager Venmo, Square and Chime command as much attention. However, competition typically brings out the best in executives; with mergers and acquisitions activity poised to resume and new fintech relationships taking root, growing one’s bank is still possible.

##

So here’s to the optimists. Leaders are defined by their actions, and many deserve to take a well-earned bow for making their colleagues’ and clients’ lives better. While we leave a year marked by incredible unemployment, economic uncertainties and political scars, I’ve found a negative mindset never leads to a happy life. Rather than lament all that went sideways this year, I choose to commemorate the unexpected positives. As I do, I extend my best to you and yours.

With appreciation,

Al

*This reflection also appears in Bank Director’s newsletter, The Slant. A new addition to our editorial suite of products in 2020, I invite you to sign up for this free Saturday newsletter here.

WASHINGTON, DC — Since March, I’ve talked with quite a few bank CEOs about their interest in modern and secure technologies. The underlying focus? Improving the experience provided to their customers.

In parallel to such one-on-one conversations, my colleague, Emily McCormick, surveyed 157 independent directors, chief executive officers, chief operating officers and senior technology executives of U.S. banks to understand how technology drives strategy at their institutions — and how those plans have changed due to the Covid-19 pandemic.

She conducted the survey in June and July — and we just released the results in Bank Director’s 2020 Technology Survey, sponsored by CDW. Here are a few key takeaways:

Focus on Experience

Eighty-one percent of respondents say improving the customer experience drives their bank’s technology strategy; 79% seek efficiencies.

Driving the Strategy Forward

For 64% of respondents, modernizing digital applications represents an important piece of their bank’s overall technology strategy. While banks look to third-party providers for the solutions they need, they’re also participating in industry groups (37%), designating a high-level executive to focus on innovation (37%) and engaging directors through a board-level technology committee (35%). A few are taking internal innovation even further by hiring developers (12%) and/or data scientists (9%), or building an innovation lab or team (15%).

Room for Improvement

Just 13% of respondents say their small business lending process is fully digital, and 55% say commercial customers can’t apply for a loan digitally. Retail lending shows more progress; three-quarters say their process is at least partially digital.

Spending Continues to Rise

Banks budgeted a median of $900,000 for technology spending in fiscal year 2020, up from $750,000 last year. But financial institutions spent above and beyond that to respond to Covid-19, with 64% reporting increased spending due to the pandemic.

Impact on Technology Roadmaps

More than half say their bank adjusted its technology roadmap in response to the current crisis. Of these respondents, 74% want to enhance online and mobile banking capabilities. Two-thirds plan to upgrade — or have upgraded — existing technology, and 55% prioritize adding new digital lending capabilities.

Remote Work Permanent for Some

Forty-two percent say their institution plans to permanently shift more of its employees to remote work arrangements following the Covid-19 crisis; another 23% haven’t made a decision.

Interestingly, this survey reveals that fewer banks rely on their core provider to drive their technology strategy. Forty-one percent indicated that their bank relies on its core to introduce innovative solutions, down from 60% in last year’s survey. Sixty percent look to non-core providers for new solutions. Interested to learn more? I invited you to view the full results of the survey on BankDirector.com.

WASHINGTON, DC — The bank M&A market is currently in a deep chill, thanks to the Covid-19 pandemic. It is unclear when deal activity will heat up, so who better to ask than Tom Michaud, the President & CEO, Keefe, Bruyette & Woods, A Stifel Company, as part of Bank Director’s new AOBA Summer Series. In this one-on-one, I ask him about:

There are 10 videos in the AOBA Summer Series, with topics directed at C-suite executives or boards. We talk about how important scale has become, given compressing net interest margins, increasing efficiency ratios and climbing credit costs. We explore why banks’ technology strategy cannot be delegated. We observe why some banks will come out of this experience in a bigger, stronger position. And we look at leadership, appreciating that many executives are leading in new, more positive and impactful ways. To watch, click here.

WASHINGTON, DC — By the time the NFL announced plans to host the draft from various remote locations, nearly every other sports league had postponed or canceled their events.

The decision raised eyebrows.

The NFL draft has become a must-attend in-person event, as evidenced by the record-breaking 600,000 turnout in Nashville, Tennessee, last year. As a fan, I wondered if the league was putting their own interests too far ahead of others by going forward with a new, unproven format just to keep to this activity on the calendar.

It turns out, the digital nature of the three-day event resonated in many positive ways. The draft was viewed by 55 million viewers over the three-day event, according to the league. Naturally, some of the viewership reflected an appetite for new, non-pandemic related content. But from a business perspective, it showed how migrating an in-person event entirely online could, in a pinch, work.

As we all try our best to live normal lives from our homes, the NFL’s success with the draft gives me confidence in our decision to go remote with our annual Experience FinXTech.

Much as the NFL drew a great audience to Music City last year, so too were we excited to welcome a stellar audience to Bank Director’s hometown in early May. Just as the NFL figured out how to provide viewers with new glimpses into their team’s futures, so too will our Experience FinXTech as we move online. Ours will just be in terms of how and where financial technology companies and financial institutions might develop relationships that beget future successes.

Experience FinXTech parallels the NFL draft based on the concept of team-building. Just as every NFL franchise faces its own challenges, so too does every financial institution. Indeed, the ever-expanding digital chasm between the biggest banks and community institutions remains a major strategic challenge in terms of talent, tools and dollars spent.

While there is no one-size-fits-all approach to building a team, there are lessons that executives and leadership teams might entertain from their peers during a program like this one. Indeed, we have heard and seen incredible examples of community banks pulling together to serve their constituents as best they can, however they can, during this time. This program allows us to share examples.

Bank Director’s desire to help community banks succeed in all circumstances provides an impetus for moving to video and webinars instead of waiting until the late fall to meet in person. Helping banks and fintechs get smarter about immediate opportunities to develop meaningful relationships is incredibly relevant. The time is now to assess a business strategy and make decisions that could reshape your institution’s future. Access to timely, verified and reliable information is something we didn’t want to delay in providing.

Indeed, Experience FinXTech will touch on areas where technology can assist banks to provide counseling, assistance and a personal touch to their existing and potential customers. In addition, we talk about authentication. The need to embrace the cloud. Filling in the missing pieces in the digital commercial banking product set.

Beginning on May 5, we take a pragmatic approach to new business relationships, collaborations and strategic investments. We offer virtual demonstrations to help viewers see proven technologies available to banks with regards to security, data and analytics, internal systems, lending, digital banking, payments, compliance and the customer experience.

With so many elements of our economy being challenged, we know our “next normal” will look very different from what we’ve become accustomed to. Connecting interests, and ideas, to help banks and fintechs navigate their futures is why we ultimately decided to offer this year’s experience online, for free, to anyone interested in joining us.

I look forward to welcoming people to this year’s Experience FinXTech and promise that references to certain NFL teams will be kept to a minimum.

_ _ _

Thanks to the support of these companies, we are able to extend complimentary registration for Experience FinXTech. To sign up, please click here.

WASHINGTON, DC — How should you position your bank for the future — or, for that matter, the present? This is one of the most perplexing questions challenging leadership teams right now. It is not a new consideration; indeed, the industry has been in a constant state of evolution for as long as anyone on our team can remember. Yet lately, it has taken on a new, possibly more existential sense of urgency.

Fortunately, there are examples of banks, of different sizes and a variety of business models, keeping pace with changing consumer expectations and commercial clients’ needs. The industry seems to be responding to the ongoing digital revolution in banking in three ways.

#1: Forge Your Own Digital Frontier

The biggest banks—those like JPMorgan Chase & Co., Bank of America Corp. and Wells Fargo & Co.—have the resources to forge their own paths on the digital frontier. These banks spend as much as $11 billion a year each on technology. Each hires thousands of programmers to conceptualize digital solutions for customers. And you know what? Their results are impressive.

As many as three-quarters of deposit transactions are completed digitally at these banks (take a minute and let that number sink in). A growing share of sales, account openings and money transfers take place over these banks’ digital channels as well. This allows these banks to winnow down their branch networks meaningfully while still gaining retail deposit market share.

*IMO, the next step in their evolution is to combine digital delivery channels with insights gleaned from data. It’s by marrying the two, I believe, that banks can gain a competitive advantage by improving the financial lives of their customers.

#2: Look Outside For Tailored Solutions

Just below the biggest banks are super-regional and regional banks. They too are fully embracing technology, although they tend to look outside their organizations for tailored solutions that will help them compete in this new era (rather than develop the solutions themselves).

These banks talk about integration as a competitive advantage. They argue that they can quickly and nimbly integrate digital solutions developed elsewhere—growing without a burdensome branch network while also benefiting from the latest technologies without bearing the risk and cost of developing many of those solutions themselves. It is a way, in other words, for them to have their cake and eat it too.

U.S. Bancorp and PNC Financial Services Group fall into this category. Both are reconfiguring their delivery channels, reallocating funds that would be spent on expanding and updating their branch networks to digital investments.

In theory, this makes it possible for these banks to expand into new geographic markets with far fewer branches. Indeed, U.S. Bancorp announced recently that it will use a combination of digital channels and new branches to establish a physical retail beachhead in Charlotte, North Carolina. PNC Financial is doing the same in Dallas, Texas, among other markets.

#3: Go Off-the-Shelf

Finally, smaller community banks are adopting off-the-shelf solutions offered by their core providers—Fidelity National Information Services (FIS), Fiserv and Jack Henry & Associates.

This approach can be both a blessing and a curse. It is a blessing because these solutions have enabled upwards of 90 percent of community banks to offer mobile banking applications—table stakes nowadays in the industry. It is a curse because it further concentrates the reliance of community banks on a triumvirate of service providers.

In the final analysis, however, it is important to appreciate that smaller banks based outside of major metropolitan areas still have a leg up when it comes to tried-and-true relationship banking. Their share of loans and deposits in their local markets could even grow if the major money-center banks continue fleeing smaller markets in favor of big cities.

Smaller regional and community banks dominate small business loans in their markets—a fact that was recently underscored by LendingClub Corp.’s decision to close its small business lending unit. These loans still require local expertise—the type of expertise that resides in their hometown banks. The same is true of agriculture loans.

Let’s Not Forget: Banks Are Still Banks

Trust is still the top factor cited by customers in the selection process. And loans must still be underwritten in a responsible way if a bank wants to survive the irregular, but not infrequent, cycles that define our economy. The net result is that some community banks are not only surviving in this new digital era, they are thriving.

But this isn’t a call to complacency—far from it.

WASHINGTON, DC — At this time two years ago, optimism swept across the banking sector. The change in administration gave us a steepened yield curve. Investors predicted improved economic growth. Many anticipated regulatory relief and the prospect of major corporate tax cuts.

The future of banking looked promising.

Now, pragmatism has worn that luster. Many have concerns about the growing divide between the biggest banks and everyone else. Throughout 2018, moderate loan and dull deposit growth proved persistent themes for banks.

The future appears far more challenging.

As the year winds down, I find the cyclical nature of banking of particular interest. While an optimist by nature, I fear we’re entering a harder operating environment.

Against this backdrop, I take some comfort in a new book by Dorris Kearns Goodwin, “Leadership in Turbulent Times.” Goodwin provides anecdotes about controlling negative emotions, like President Abraham Lincoln’s “hot letters”—his own missives of his frustrations he then put aside, hoping he’d never have to send what he’d written.

So in that spirit, consider this my “Lincoln letter” to a bank’s CEO and board, albeit with an optimist’s take.

Please pay attention to the vast amounts being spent on digital advertising.

The Interactive Advertising Bureau (IAB) and PwC estimate U.S. digital ad spending will hit $100 billion by year-end. This number might shock those thinking about where and how they want to tell their bank’s story through videos, social media and other digital means. Nonetheless, considering what’s being spent to court the attention of your “loyal” constituents might spark new ideas for where to invest time and effort.

When thinking tech, intertwine conversations about talent.

With venture capitalists still pouring money into startups offering basic banking services, potential employees have even more options to spend their energy and creativity. For any bank, the demand for the talent needed to deliver new digital capabilities will significantly outpace the available labor pool. If you don’t have a team now, I worry your bank might be challenged to successfully create meaningful technology partnerships.

Culture is eating strategy (and new initiatives) for breakfast, lunch and dinner.

Many executives have talked with me about how they’re working hard to ensure the bank’s existing culture keeps pace with the evolution of the industry. We all deal with execution risk—but as that old saying goes, if all you ever do is all you’ve ever done, then all you’ll ever get is all you’ve ever gotten.

Windows of opportunity most certainly exist. What those windows are, and how long they remain open, remains a moving target — one we intend to focus on next month at our 25th annual Acquire or Be Acquired Conference, Jan. 27-29 at the JW Marriott Phoenix Desert Ridge in Phoenix, Arizona.

*This first ran in Bank Director’s weekly newsletter, The Slant, on December 8.

Quickly:

CHICAGO — Guess what? As institutions continue to seek out growth and efficiencies through technology, they in turn expose themselves to new risks and liabilities. Understanding the two-sided nature of this proverbial coin reflects just one of the many nuanced conversations that took place during our annual Bank Audit & Risk Committees Conference. If you’re not familiar with this exclusive event, we invite bank leaders from across the country to take a broad and strategic view at the risk landscape, while also focusing on specific actions to improve a bank’s performance.

Indeed, our team put together an agenda filled with opportunities to improve existing audit and risk functions. In addition, we surfaced new ideas around issues and topics such as cybersecurity, credit quality, blockchain, rising interest rates and financial reporting.

Personally, I was thrilled to welcome more than 400 men and women to the Swissotel Chicago — with over 300 participants comprising bank CEOs, chairmen, board members, CFOs, CROs, senior executives and internal auditors. Throughout our time together, we took the opportunity to pose a series of questions to this hugely influential and knowledgeable audience. As we discovered, the increasing level of U.S. debt proved the biggest macroeconomic concern for this group by a wide margin. Yes, we polled this group using an audience response device and found 52% placed this issue as their top concern — far outpacing the 15% who cited a potential recession and 13% who pointed towards a political crisis.

Such in-person polling provides quite a bit of insight as to where we might be heading as an industry and an economy. What follows are five additional survey results from this year’s event on how this experienced audience feels about various hot topics.

54% = Technology changes and FinTech

20% = Recession risk and loan quality

17% = Flattening yield curve

6% = Pushed out by consolidation

4% = Regulatory scrutiny

78% = We face stiff competition; deposit pricing will be a key concern

13% = Our ability to compete for deposits will improve as rates rise

9% = Unsure

50% = No

35% = Yes, but for a short period of time

10% = Yes, I’m deeply concerned

4% = Unsure

23% = Updates to internal processes / infrastructure

22% = Cost of RegTech solutions

21% = Identifying valid solutions

17% = Vetting providers / third party management

15% = Internal skills

3% = Regulatory acceptance

78% = No

18% = Yes

4% = Unsure

I’ll keep my observations on these findings to personal conversations… That said, from improving risk oversight, mastering new reporting requirements and staying ahead on compliance, this year’s conference provided practical takeaways for participants to bring back to their banks. Curious to see what we covered? I encourage you to take a look at BankDirector.com or search for @BankDirector and #BDAudit18 on Twitter.

Quickly:

PHOENIX — I’ve spent the past few days with bank leaders, technology executives, investors and analysts interested to explore emerging trends, opportunities and challenges facing many as they look to grow and scale their businesses. So as I prepare to head home to DC after some wonderfully exciting days at Bank Director’s annual FinXTech Summit, a few highlights from my time in the desert.

For me, one of the signature pieces of this year’s program occurred on Thursday evening. Under the stars, we recognized ten partnerships, each of which exemplified how banks and financial technology companies work together to better serve existing customers, attract new ones, improve efficiencies, bolster security and promote innovation. The finalists for this year’s Best of FinXTech Awards can be seen in this video.

We introduced these awards in 2016 to identify and recognize those partnerships that exemplify how collaborative efforts can lead to innovative solutions and growth in the banking industry. This year, we focused on three areas of business creativity:

The winners? Radius Bank and Alloy for Startup Innovation, CBW Bank and Yantra Financial Technology for Innovative Solution of the Year and Citizens Financial Group and Fundation for Best of FinXTech Partnership. To learn more about each, check out this cover story on BankDirector.com

https://twitter.com/ValidisGlobal/status/994635200331177984

Well played with the ZZ Top reference — now we just needs to grow out that beard and drop a pair of RayBans into the shot.

During our time in the desert, we shared a number of videos on BankDirector.com. The page with all videos can be found on FinXTech Annual Summit: Focusing on What’s Possible. To get a sense of what these short videos look like, here is an example:

Thanks to all those who joined us at the Phoenician. For more ideas and insight from this year’s event, I invite you to take a look at what we’ve shared on BankDirector.com (*no registration required).

Quickly:

PHOENIX — Many financial institutions face a creativity crisis. Legacy systems and monolithic structures stifle real change at many traditional banks — while newer technology leaders move quickly to pick up the slack. During the first day of our annual FinXTech Summit at the Phoenician, I picked up on a few practical ideas to break down a few of the most common barriers to innovation inside financial institutions.

As our managing editor, Jake Lowary, wrote for BankDirector.com this morning, “the cultural and philosophical divides between banks and fintech companies is still very apparent, but the two groups have generally come to agree that it’s far more lucrative to establish positive relationships that benefit each, as well as their customers, than face off on opposite ends of the business landscape.”

So with this in mind, I invite you to follow the conference conversations via our social channels, where our team continues to shares ideas and information from Day 2 of this event using @BankDirector and @Fin_X_Tech on Twitter. In addition, you can search & follow #FinXTech18 to see what’s being shared with (and by) our attendees.

Quickly:

PHOENIX — As we kicked off this year’s FinXTech Summit, I found myself engaged in a conversation about how (and why) banks might “freeze and wrap” their data using their current core system while moving their customer engagement and analytics into the cloud. While this was my first time hearing that particular description/approach, the underlying logic certainly applies for many of the bankers joining us at the Phoenician. In fact, it inspired this short video shot during today’s lunch.

As a company, we’ve been writing about banks realizing that the benefits of cloud computing outweigh added security risks for a while now. But it strikes me that interest in cloud-based platforms has been on the rise of late. As our friends at Blend shared on BankDirector.com, “the cloud presents opportunities for enhanced efficiencies and flexibility — without any security trade-offs — so it’s no surprise that we’re seeing more organizations shift to the software as a service (SaaS) model.”

Interested to see what a move into the cloud might means for banks? Take a look at these five cloud-based companies:

I’ll check in later tonight to recap several presentations that explore what makes for a strong, digitally-solid bank. Before that posts, I invite you to follow the conference conversations via our social channels. You can follow me @AlDominick on Twitter — and our team shares ideas and information through @BankDirector plus our @Fin_X_Tech platform. Finally, search & follow #FinXTech18 to see what’s being shared with (and by) our attendees.

##

FWIW, my reference to Amazon.com, Salesforce.com and Oracle in this video traces back to January 2, when Bloomberg reported the first two were “actively working to replace Oracle software running on crucial business systems with lower cost open-source database software.” For more: Amazon, Salesforce Shifting Business Away From Oracle: Report