Quickly:

- Making banking digital, personalized and in compliance with regulatory expectations remains an ongoing challenge for the financial industry. This is just one reason why a successful merger — or acquisition — involves more than just finding the right cultural match and negotiating a good deal.

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

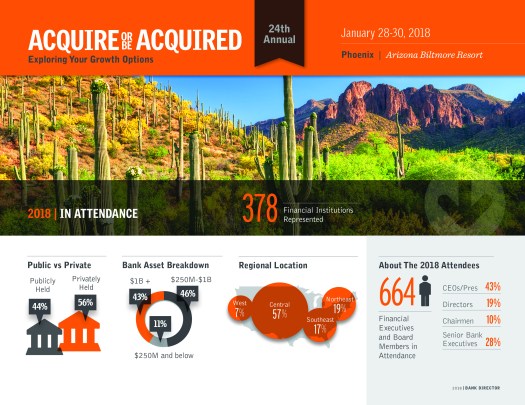

PHOENIX, AZ — As the sun comes up on the Arizona Biltmore, I have a huge smile on my face. Indeed, our team is READY to host the premier financial growth event for bank CEOs, senior management and members of the board: Bank Director’s 24th annual Acquire or Be Acquired Conference. This exclusive event brings together key leaders from across the financial industry to explore merger & acquisition strategies, financial growth opportunities and emerging areas of potential collaboration.

The festivities begin later today with a welcoming reception on the Biltmore’s main lawn for all 1,125 of our registered attendees. But before my team starts to welcome people, let me share what I am looking forward to over the next 72 hours:

- Saying hello to as many of the 241 bank CEOs from banks HQ’d in 45 states as I can;

- Greeting 669 members of a bank’s board;

- Hosting 127 executives with C-level titles (e.g. CFO, CMO and CTO);

- Entertaining predictions related to pricing and consolidation trends;

- Hearing how a bank’s CEO & board establishes their pricing discipline;

- Confirming that banks with strong tangible book value multiples are dominating M&A;

- Listening to the approaches one might take to acquire a privately-held/closely-held institution;

- Learning how boards debate the size they need to be in the next five years;

- Engaging in conversations about aligning current talent with future growth aspirations;

- Juxtaposing economic expectations against the possibilities for de novos and IPOs in 2018;

- Getting smarter on the current operating environment for banks — and what it might become;

- Popping into Show ’n Tells that showcase models for cooperation between banks and FinTechs;

- Predicting the intersection of banking and technology with executives from companies like Salesforce, nCino and PrecisionLender;

- Noting the emerging opportunities available to banks vis-a-vis payments, data and analytics;

- Moderating this year’s Seidman Panel, one comprised of bank CEOs from Fifth Third, Cross River Bank and Southern Missouri Bancorp;

- Identifying due diligence pitfalls — and how to avoid them;

- Testing the assumption that buyers will continue to capitalize on the strength of their shares to meet seller pricing expectations to seal stock-driven deals;

- Showing how and where banks can invest in cloud-based software;

- Encouraging conversations about partnerships, collaboration and enablement;

- Addressing three primary risks facing banks — cyber, credit and market; and

- Welcoming so many exceptional speakers to the stage, starting with Tom Michaud, President & CEO of Keefe, Bruyette & Woods, Inc., a Stifel Company, tomorrow morning.

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.