Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Last week, I had the pleasure of spending a few minutes with Tom Fitzgerald and Caleb Stevens on their Community Bank Podcast. Produced by SouthState’s Correspondent Division, the two dedicate their pod to helping community bankers grow themselves, their team — and their profits. For about 23 minutes, the three of us explored:

Oh yes, and I botched my ice cream analogy early on. As someone with a sweet tooth, I meant to reference Baskin & Robbins‘ 31 flavors of ice cream while talking leadership characteristics. As a child in Needham, MA, the idea that I’d have to choose between chocolate, coffee, oreo, cookie dough, etc posed a real challenge — especially as we’d go as a post-dentist treat! So when Caleb asks me about key facets of leadership in banking today, please understand my Covid-brain took me back to those fun childhood memories… which is how I wound up bellyflopping on the analogy!!

WASHINGTON, DC — The bank M&A market is currently in a deep chill, thanks to the Covid-19 pandemic. It is unclear when deal activity will heat up, so who better to ask than Tom Michaud, the President & CEO, Keefe, Bruyette & Woods, A Stifel Company, as part of Bank Director’s new AOBA Summer Series. In this one-on-one, I ask him about:

There are 10 videos in the AOBA Summer Series, with topics directed at C-suite executives or boards. We talk about how important scale has become, given compressing net interest margins, increasing efficiency ratios and climbing credit costs. We explore why banks’ technology strategy cannot be delegated. We observe why some banks will come out of this experience in a bigger, stronger position. And we look at leadership, appreciating that many executives are leading in new, more positive and impactful ways. To watch, click here.

Dreaming of a trip to Phoenix, and the Acquire or Be Acquired Conference, next January doesn’t seem so odd this summer.

WORKING FROM HOME — For decades, business leaders began to book their travel to the Arizona desert — for Bank Director’s Acquire or Be Acquired Conference — in early August. As evidenced by the nearly 1,400 at the Arizona Biltmore earlier this year, the annual event has become a true stomping ground for CEOs, executives and board members. Many laud it as the place to be for those that take the creation of franchise value seriously. I’ve even heard it referred to as the unofficial kickoff of banking’s new year.

Just seven months ago, Acquire or Be Acquired once again brought together industry leaders from across the United States to explore merger opportunities, acquisition trends and financial growth ideas. With 418 banks represented, participants considered strategies specific to lending, deposit gathering and brand-building. They talked regulation, met with exceptional fintechs and networked with their peers under sunny skies.

Not one openly worried about a global pandemic.

Yet here we are, all of us dealing with fast-moving challenges and unimaginable risks.

So what can we do to help?

This is the question that proved the catalyst for our new AOBA Summer Series. Indeed, we created this free, on-demand, compilation of thought leadership pieces to provide pragmatic information and real-world insight.

With CEOs and leadership teams being called upon to make decisions they have never been trained for, we realized the type of information typically shared in January has immediate merit this summer. So instead of waiting until winter, this new Summer Series provides both color and context to the tough decisions — those with profound long-term consequences — that confront executives every day.

Ten videos comprise the AOBA Summer Series, with topics appropriate for the C-suite’s or board’s consideration. Streaming on BankDirector.com, we talk about how important scale has become in the banking industry… how one’s technology strategy cannot be delegated… how it certainly seems that there will be banks that come out of this in a bigger, stronger state. Here’s a screen-grab of what you’ll come across:

In one-on-one conversations like these, we acknowledge how net interest margins are compressing — which will drive up efficiency ratios — and credit costs are climbing. And we look at leadership, appreciating that many are leading in new, more positive and impactful ways. In addition, this new series provides:

A SNAPSHOT ON CURRENT CONDITIONS

At our January Acquire or Be Acquired Conference, Tom Michaud, President & CEO, Keefe, Bruyette & Woods, A Stifel Company, provided his outlook for the industry. Now, we ask him to update his perspectives on M&A activity and share his take on the potential implications of the pandemic.

HOW FINTECHS FIT

A growing number of technology companies have been founded to serve the banking industry. Not all of them have what it takes to satisfy bankers. During various sessions we learn how a variety of banks approach innovation — and the specific attributes a leadership team should look for in a new fintech relationship.

THE LEVERS OF VALUE CREATION

With nCino’s CMO, Jonathan Rowe, our Editor-in-Chief talks about the levers of creating value vis-a-vis the flywheel of banking. Together, they explain how certain technologies promote efficiency, which promotes prudence, thereby promoting profits, which can then be invested in technology, starting the cycle all over again.

Hearing from investment bankers, attorneys, accountants, fintechs, investors and — yes, other bankers — about the outlook for growth and change in the industry proves a hallmark for Acquire or Be Acquired, be it in-person or online.

As this new series makes clear, The future is being written in ways unimaginable just a few months ago. We invite you to watch how industry leaders are making sense of the current chaos for free on BankDirector.com.

WASHINGTON, DC — To get a sense of what trended at Bank Director’s 25th annual Acquire or Be Acquired conference, here’s a link to five video check-ins. All 2 minutes or less in length, these summarize various topics and trends shared with 1,300+ attendees.

Acquire or Be Acquired Conference

January 26-28, 2020 | Arizona Biltmore Resort | Phoenix, AZ

For early-bird registration, please click here.

WASHINGTON, DC — So, there’s this guy named Warren Buffet who has a few thoughts on business. This Nebraska-based investor once opined “I’d rather pay a fair price for a wonderful company than a wonderful price for a fair company.” Quite sagacious — and appropriate to share in advance of our 25th annual Acquire or Be Acquired Conference which takes place January 27-29 at the JW Marriott Phoenix Desert Ridge in Arizona.

Since we last hit the desert, several regional banks have been active in the M&A market — and may continue to look for merger opportunities to build up scale. In addition, we’ve seen how tax reform had a big impact on the industry, with many making investments to grow their business.

Now, with the government shutdown straining our economy, big banks beating community banks on the digital front and shifting team & cultural dynamics, we have a lot of ground to cover over two-and-a-half days. Interested to see what we have planned? Take a look at the full agenda.

While I am excited to reconnect with quite a few folks, I am particularly interested in a number of strategic issues that will be discussed. For instance:

For those joining us in Arizona, I encourage men to bring a sports coat or a jacket for the evenings as we plan to be outside for our receptions and the desert quickly cools off once the sun sets. In addition, the rumors of people being in their seats at 7:15 – 7:30 on Sunday morning? 100% true. We start at 7:45 AM and there are quite a few pictures from last January’s event if you need visual proof.

Finally, the digital materials for the conference can be found on BankDirector.com. Once you register on-site, you’ll be given a passcode to access the materials that can be used throughout the event.

_ _ _

Whether you are able to join us in person or are simply interested in following the conference conversations via our social channels, I invite you to follow @AlDominick @BankDirector and @Fin_X_Tech on Twitter. Search & follow #AOBA19 to see what is being shared with and by our attendees. If you are going to be with us in Arizona and we’re not already connected here on LinkedIn, drop me a note and let’s fix that.

WASHINGTON, DC — Can community banks out-compete JP Morgan, BofA and Wells Fargo? This is the elephant in the room awaiting 853 bank executives and board members — representing 432 Banks — at our upcoming Acquire or Be Acquired Conference. The lights don’t officially come up on our 25th annual event at the JW Marriott Phoenix Desert Ridge until Sunday, January 27. So in advance, three big questions I anticipate fielding in the desert.

As noted by H2 Ventures and KPMG, Amazon is providing payment services and loans to merchants on its platform, while Facebook recently secured an electronic money licence in Ireland. Alibaba, Baidu and Tencent have become dominant operators in China’s $5.5 trillion payments industry. Add in Fiserv’s recent $22B acquisition of First Data and Plaid’s of Quovo and we might be seeing the start of a consolidation trend in the financial technology sector. Will such investments and tie-ups draw the attention of big technology companies to the financial services industry?

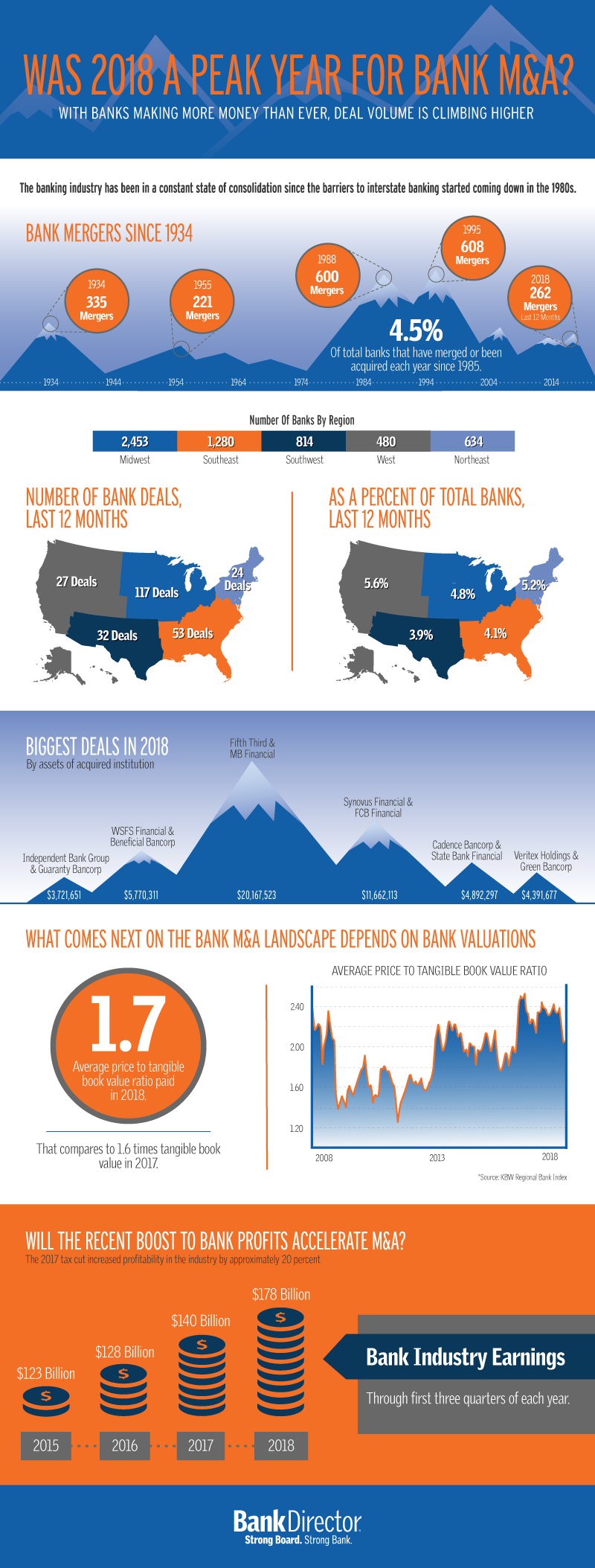

When I heard the rumor that BBVA might be buying UK-based Atom Bank — one of the proverbial European challenger banks — I started to look at acquisition trends here in the U.S. Case-in-point, we put together the following graphic in December for BankDirector.com

We know that some community banks have been holding out hopes of higher pricing multiples or for a strategic partner. These institutions might find the window of opportunity to stage an exit isn’t as open as it was just a few years ago. This doesn’t mean the window has shut — but I do think an honest assessment of what’s realistic, at the board level, is appropriate.

A NY Times op-ed piece posits that the bond market reveals growing cracks in the financial system. Authored by Sheila Bair, the former chairwoman of the FDIC, and Gaurav Vasisht, director of financial regulation at the Volcker Alliance, it warns that “regulators are not doing enough to make sure that banks are prepared.” While the duo calls for thicker capital cushions for big banks and tighter leveraged loan underwriting standards, I wonder how executives joining us in Arizona feel about this potential threat to our economy?

_ _ _

As the premier bank M&A event for bank CEOs, senior management and board members, Bank Director’s 25th annual Acquire or Be Acquired Conference brings together key bank leaders from across the country to explore merger & acquisition strategies and financial growth opportunities. If you’re joining us in the desert, I’ll share a few FYIs later this week. If you’re unable to join us in Phoenix, AZ, I’ll be tweeting from @aldominick and using #AOBA19 when sharing on social platforms like LinkedIn.

Quickly:

WASHINGTON, DC — As the last few hours of July tick by, our team continues to build towards next winter(!) and the premier bank M&A event for CEOs, senior management and board members: Bank Director’s annual Acquire or Be Acquired Conference. This special event brings together key bank leaders from across the country to explore merger & acquisition strategies, consolidation trends and financial growth opportunities.

Earlier this year, we welcomed 1,200+ to the Arizona desert — and anticipate a similar audience when we return a week before next year’s Super Bowl. We’ve recently added a lot of new information on January’s program to BankDirector.com; if you’re interested to see what we’re planning, I invite you to take a look.

In addition to Acquire or Be Acquired, I am really excited to host two conferences before we return to the desert. On September 10-11 at the Four Seasons Hotel Chicago, we host our very popular Bank Board Training Forum. This two-day program provides bank directors with the education and training needed to address the issues and challenges facing them in today’s ever competitive, highly regulated and rapidly evolving banking and financial services industry.

From November 5 – 7, at the Four Seasons Resort & Club Dallas at Las Colinas (a short hop from DFW airport), we convene Bank Director’s annual Bank Compensation & Talent Conference to focus on the recruitment, development and compensation of a bank’s most essential talent. While in Dallas, leading advisers share their perspectives on building and supporting the best teams by providing first-hand information on the strategies and plans being used by successful banks today.

If you’re interested in any of these three exceptional programs, you can learn more here.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

PHOENIX, AZ — Michael Porter, the noted economist, researcher and teacher, once said, “strategy is about making choices, trade-offs; it’s about deliberately choosing to be different. The essence of strategy is choosing what not to do. No one can tell you which rules to break, but you can acquire more skill in determining which rules to break given your talents and circumstances right now.”

Porter’s perspectives came back to me while listening to KBW’s CEO, Tom Michaud. Yesterday morning, Tom talked about the strategic paths that a bank’s CEO might consider in the years to come. As he shared, pressure from investors to deploy capital stimulated M&A discussions in 2017 — and will continue to impact deals in 2018. He also noted that pressure placed on deposit costs, as interest rates rise, contributes to the potential acceleration of bank consolidation. These were just two of the many notes I jotted down during the first day of our annual event. Broadly speaking, what I heard fell into five categories:

1. Economic trends

2. Regulatory trends

3. Small business lending trends

4. Management succession trends

5. Technological innovation trends

Many banks enter 2018 with steady, albeit slow loan growth — while recognizing modest margin improvement as they continue to focus on controlling expenses. Accordingly, I thought to elaborate on the issues I found interesting and/or compelling. Feel free to comment below if other points caught your eye or ear.

FJ Capital authored a piece in late October that noted how, as the Fed progresses further into the tightening phase of the interest rate cycle, banks will find it more difficult to fund loan growth by raising new low‐cost deposits. Their view, which I heard echoed here, is banks with low‐cost core deposits will become more valuable over the next few years as banks wrestle with increased funding costs. In addition to this idea, I made note that banks with a strong deposit base could be more attractive to buyers as interest rates rise. However, a remark I’ve heard at past events re-emerged here. Namely, making a small bank profitable is hard; exiting, even harder.

Given the audience here, I wasn’t surprised by the continued talk of removing the synthetic $10Bn designation. If the Fed, FDIC and OCC raise the $50Bn threshold as spelled out in Dodd Frank, we could see more banks in the $20Bn – $40Bn range come together. Given that large regional banks usually can pay high prices for smaller targets, unleashing this capacity could reignite more M&A and boost community bank valuations. In addition, the Community Reinvestment Act remains a major headwind in bank mergers. Many here want improvements in the CRA process, which in turn could reduce regulatory risk for bank M&A.

When it comes to the lifeblood of most banks — small business lending — a recurring question has been where and how community banks can take market share from larger banks. My two cents: closing loans faster is key, as is structuring loans to fit specific borrower profiles while being supremely responsive to the customer. Oh, and credit is a big theme right now — and the best clients typically have the best credit.

An inescapable comment / observation: aging management teams and board members has been a primary driver of bank consolidation of late. I noted that the average age of a public bank CEO and Chairman is 60 and 66, respectively. It was suggested that this demographic alone plays a key factor in the next few year’s consolidation activity.

When it comes to bank mergers, one of the big drivers of deals is the rise in technology-driven competition (*along with regulatory costs and executive-succession concerns). I sense that most traditional banks haven’t really figured out the digital migration process we’ve embraced as a world. Finally, it appears that the biggest banks are winning the war for retail deposits. This is an issue that many management teams and boards should be discussing…

_ _ _

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

PHOENIX, AZ — For all the talk of bank consolidation, there are still 5,700+ banks in the United States. But let’s not kid ourselves. For many community banks today, earnings pressures + regulatory and compliance costs + the continued impact of technology = a recurring challenge.

While the number of banks in business will inevitably shrink over the next 10 years — perhaps being cut in half — I remain bullish on the overall future of this industry. If December’s tax reform spurs capital spending and job creation by small- and medium-sized businesses, many of the banks joining us here in Arizona stand to benefit. But will the recent tax cut induce companies to invest more than they already planned to? This is but one of a number of questions I look forward to asking on stage through the first day of Bank Director’s Acquire or Be Acquired Conference.

Below, ten more questions I anticipate asking:

We have an exciting — and full day — coming up at the Arizona Biltmore. To keep track of the conversations via Twitter, I invite you to follow @AlDominick @BankDirector and @Fin_X_Tech. In addition, to see all that is shared with (and by) our attendees, we’re using the conference hashtag #AOBA18.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

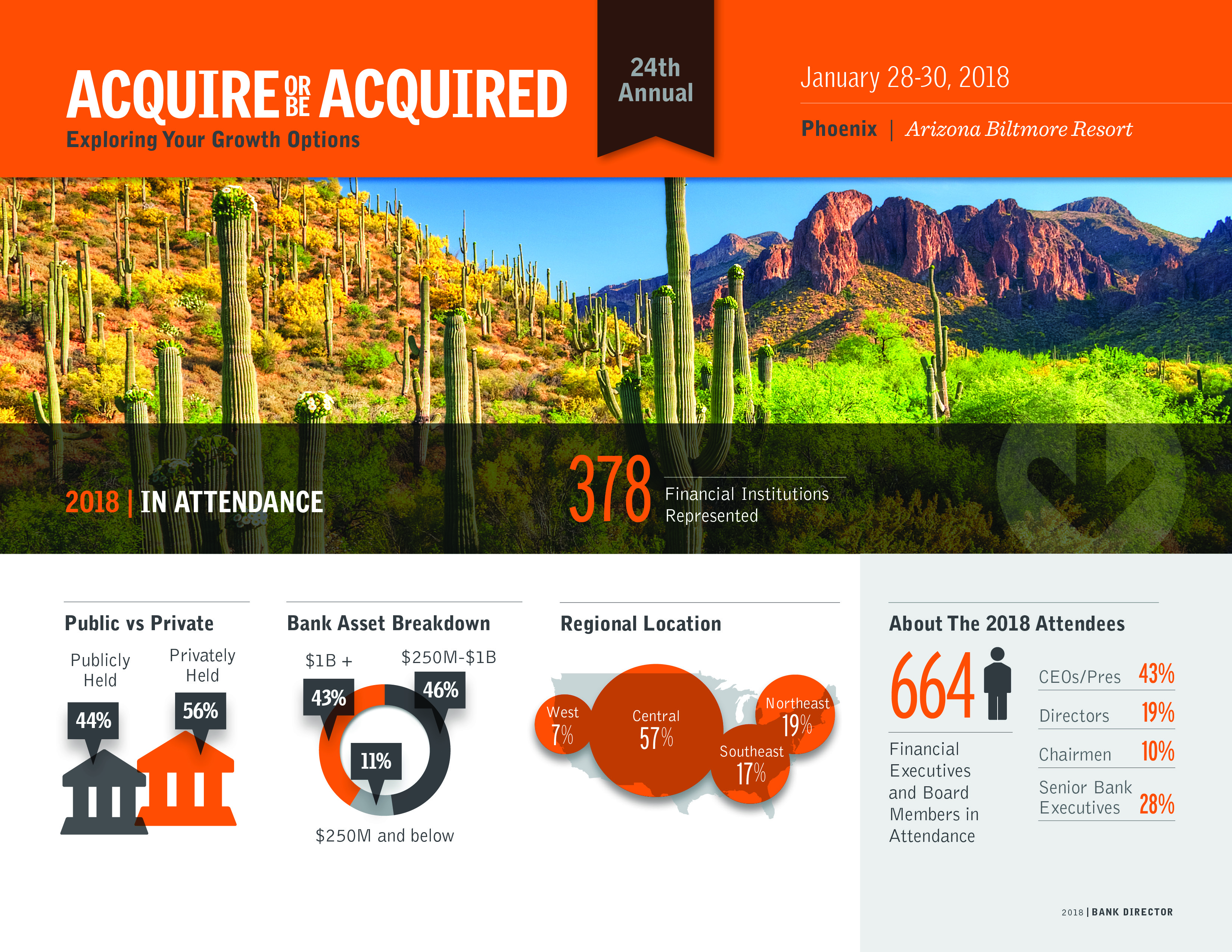

PHOENIX, AZ — As the sun comes up on the Arizona Biltmore, I have a huge smile on my face. Indeed, our team is READY to host the premier financial growth event for bank CEOs, senior management and members of the board: Bank Director’s 24th annual Acquire or Be Acquired Conference. This exclusive event brings together key leaders from across the financial industry to explore merger & acquisition strategies, financial growth opportunities and emerging areas of potential collaboration.

The festivities begin later today with a welcoming reception on the Biltmore’s main lawn for all 1,125 of our registered attendees. But before my team starts to welcome people, let me share what I am looking forward to over the next 72 hours:

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech

Quickly:

_ _ _

So much of this morning was spent talking about growth through mergers and acquisitions (M&A) that I couldn’t help but flash back to January’s Acquire or Be Acquired conference. Thematically, I went into that event expecting the unexpected. Given this morning’s presentations on growing one’s bank, I believe that mindset still holds water.

For example, Tom Michaud, the president and CEO of Keefe, Bruyette & Woods, described 2016 and 2017 as one bumpy ride. From recession fears to lower-for-longer rates, the initial euphoria after the presidential election (at least in terms of stock prices, which went up 27% – 30%) to the uncertainty of regulatory relief, he reminded us of where we are coming from relative to where we might be heading. I am always curious to hear what Tom thinks about the state of banking; below, ten things I learned from him this morning:

Following Tom’s presentation, we doubled down on growing-the-bank type topics with a session involving Rick Childs, a partner at Crowe Horwath, Jim Ryan, the CFO at Old National Bancorp, Jim Consagra, EVP and COO at United Bancshares and Bryce Fowler, chief financial officer at Triumph Bancorp.

From pricing discipline to acquisitions of privately-held/closely-held companies, the guys made clear that “there are only so many deals out there.” They shared how boards need to determine the size they want to be, honestly assess the talent they have relative to such aspirations and determine how growth through M&A aligns with enterprise risk management positioning. Essentially, their remarks made clear that a successful merger or acquisition involves more than just finding the right match and negotiating a good deal.

##

As I shared with yesterday’s post, my thanks to Crowe Horwath, Stifel, Keefe Bruyette & Woods and Luse Gorman for putting together this year’s Bank Leadership and Profitability Improvement Conference at The Inn at Spanish Bay in Pebble Beach, California.