Over the past few years, I have seen significant change within the banking community — much of it defensive or in response to government intervention and oversight. According to a white paper recently published by McLagan, “a great deal has been said about the excesses and errors of the past; however (sic), the current focus for banks, in particular, must be on the need to innovate or risk becoming stagnant and losing the ability to compete for exceptional talent.” This morning’s column focuses on the “innovator’s dilemma,” vis-a-vis three questions.

Do We Need Sustainable or Disruptive Technology ?

Do We Need Sustainable or Disruptive Technology ?

I have talked with a number of Chairmen and CEOs about their strategic plans that leverage financial technology to strengthen and/or differentiate their bank. After one recent chat, I went to my bookshelf in search of Clayton Christensen’s “The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail.” His book inspired today’s title — and fuels this first question. Christensen writes about two types of technologies: sustaining and disruptive. Sustaining technologies are those that improve product performance. As he sees it, these are technologies that most large companies are familiar with; technologies that involve improving a product that has an established role in the market. Most large companies are adept at turning sustaining technology challenges into achievements. However, large companies have problems dealing with disruptive technologies — an observation that, in my view, does not bode well for many traditionally established banks.

“Discovering markets for emerging technologies inherently involves failure, and most individual decision makers find it very difficult to risk backing a project that might fail because the market is not there.”

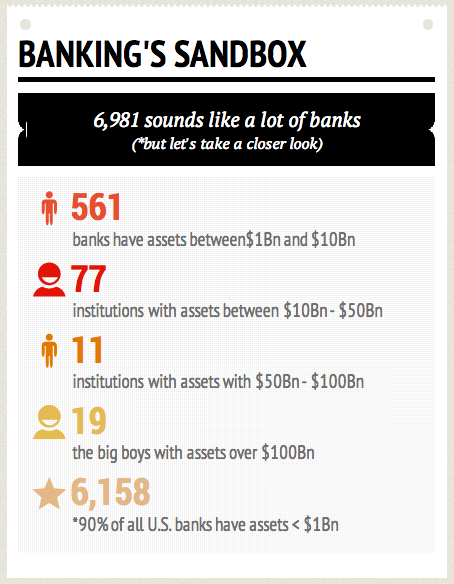

While risk is inherent to banks of all sizes, taking chances on emerging technologies continues to challenge many officers and directors. To this end, I thought about the themes explored in Christensen’s book after spending time in Microsoft’s New York City offices last week. While there, I heard how big banks are generating revenues by acquiring new customers while retaining, up-selling and cross-selling to existing customers. I left impressed by the various investments being made by the JP Morgans of the banking world, at least in terms of customer relationships and experience management along with analytics and core system modernization. I do, however, wonder how any entrenched bank can realistically embrace something “uber-esque” (read: disruptive) that could truly transform the industry.

Do We Have the Staff We Need?

Consider the following question from the perspective of a relatively new hire: “I have a great idea for a product or service… who can I talk with?” A few months ago, Stephen Steinour, the President & Chief Executive Officer at Huntington Bancshares, keynoted Bank Director’s annual Bank Executive & Board Compensation conference and addressed this very thing. As he shared to an audience of his peers: “the things I assumed from my era of banking are no longer valid.” Rather than tune out ideas from the field in favor of age and experience, he explained how his $56Bn+ institution re-focused on recruiting “the right” employees for the company they wanted (not necessarily what they had), with a particular emphasis on attracting the millennial generation into banking. He admitted it’s a challenge heightened by public perception of the industry as one that “takes advantage of people and has benefited from government bailouts.” Still, he made clear the team they are hiring for reflects a new cultural and staffing model designed to drive real, long-term change. I wonder how many banks would (or could) be so bold?

Do We Have The Right Business Model?

I’ve heard it said that “forces of change” will compel banks to reinvent their business models. Take the business model of core retail banking. According to a piece authored by McKinsey (Why U.S. Banks Need a New Business Model), over the past decade, banks continued to invest in branches as a response to free checking and to the rapid growth in consumer borrowing. But regulations “undermining the assumptions behind free checking and a significant reduction in consumer borrowing have called into question the entire retail model. In five years, branch banking will probably look fundamentally different as branch layouts, formats, and employee capabilities change.” Now, I’m not sure banking’s overall business model needs a total overhaul; after all, it still comes back to relationships and reputations. Nonetheless, many smaller banks appear ripe for a change. And yes, the question of how they have structured their business is one some are beginning to explore.

##

To comment on this piece, click on the green circle with the white plus sign on the bottom right. Looking ahead, expect a daily post on About That Ratio next week. I’ll be in Nashville at the Hermitage Hotel for Bank Director’s Bank Board Training Program. Leading up to, and at, this educational event, I’ll provide an overview on the various issues being covered. Namely, risk management and auditing issues, compensation, corporate governance, regulation and strategic planning. Thanks for reading, and Aloha Friday!