As my colleague Jack Milligan writes in our 2nd quarter issue of Bank Director magazine, just because a bank can’t own a car dealership doesn’t mean there isn’t “enormous flexibility in determining a bank’s strategy.” Curious what this means? Read on.

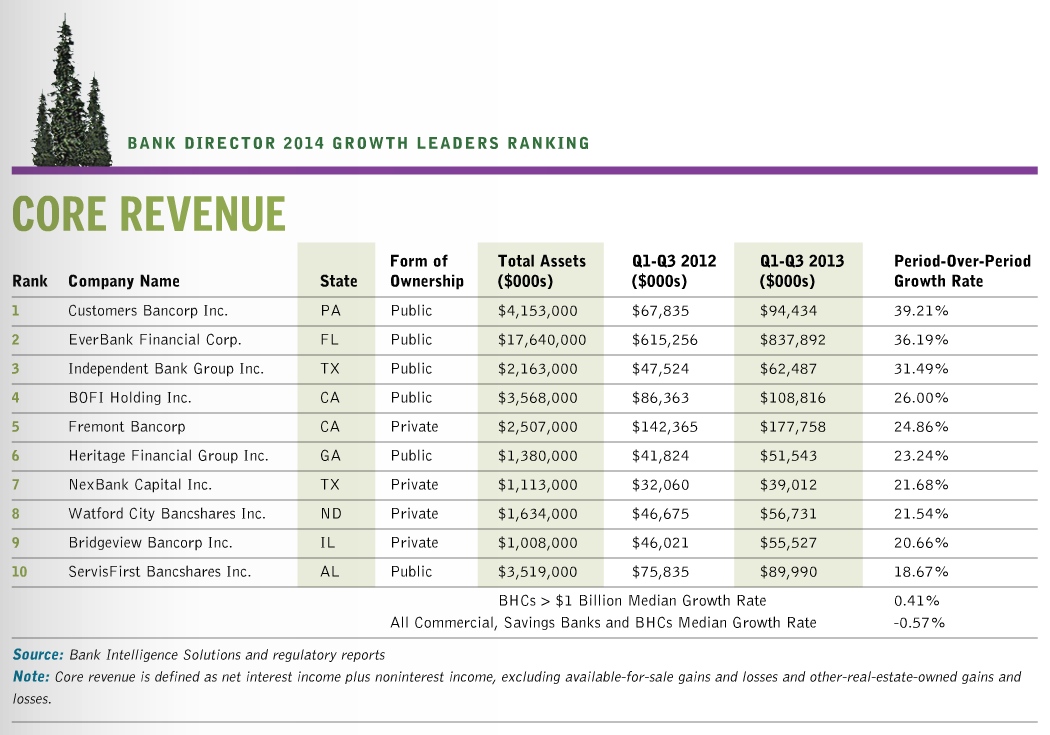

A Sneak Peek at the Core Revenue Champs

Each year, Bank Director magazine looks at all U.S. banks and thrifts to identify the strongest growth banks. We rank the top performers across four separate categories: core deposits, core noninterest income, net loans and leases and the most important, core revenue. Since the magazine mails today, I thought to offer a sneak peek of the results:

What I find interesting about the top two banks on this very strong list: both Customers Bank and EverBank Financial designed their business models around technology from their very beginnings.

Find Your Balance

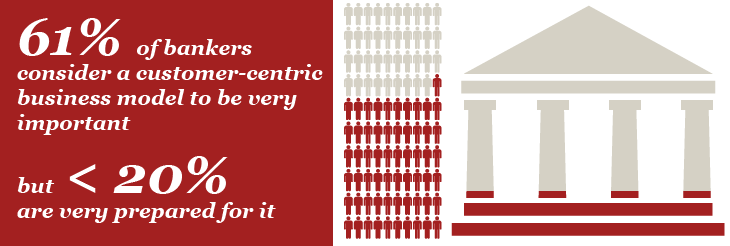

As I read through an advance copy of the issue, it strikes me that many business areas that historically provided revenue growth are simply not growing fast enough to overcome new capital and regulatory requirements. In this light, you can understand why many say times couldn’t be more challenging for growth in community or regional banking. The corollary to this? Balancing organic and external growth is a key focus area for bank management and boards.

Increasingly, I hear that growth-focused banks are considering (or implementing) strategies that create revenue growth from both net interest income and fee based revenue business lines — think government guaranteed lending, asset based lending, leasing, trust and wealth management services. Clearly, as interest margins and loan volumes remain subject to compression and intense competition, the “optimization” of fee-based revenue is becoming pivotal in enhancing shareholder value.

‘Sup Big Easy

True, a number of banks seek to extend their footprint and franchise value through acquisition. Yet, many more aspire to build the bank internally. Some show organic growth as they build their base of core deposits and expand their customer relationships; others leverage product innovation or focus on their branch network. I bring these approaches up in advance of next week’s Growth Conference at the Ritz-Carlton, New Orleans. We designed this event to showcase strategies, structures, processes and technologies that a bank’s CEO and board might consider to fuel their own growth.

Unlike trade shows and other events, we limit participation to a financial institution’s key officers and directors to ensure those joining us are not just committed to distinguishing their performance and reputation, but also are appropriate peers to share time and ideas with. From companies like StrategyCorps, Ignite Sales and VerifyValid to PwC, Fiserv and IBM, we have a tremendous roster of companies joining us in Louisiana to share “what’s working” at the myriad banks they support. As I’ve done for our other events (e.g. the sister conference to Growth, Acquire or Be Acquired), I’ll be posting a number of pieces next week from the Crescent City and invite you to follow along on Twitter via @aldominick, @bankdirector and using #BDGrow14.

Aloha Friday!