Earlier this week, I welcomed officers and directors from across the United States to Nashville, TN. From a stage (and not a Zoom), I asked them:

What are your options as we head into the Fall? No, not your personal ability to buy or sell an asset or security. Rather, the options you, as a leaders of your bank, see for the institution you are a part of today?

Strategically speaking, this is a fundamental issue for those in a leadership position to address.

Sure, there are topics that will dominate boardroom discussions — such as diversifying earnings streams and differentiating the bank’s reputation relative to others.

But let me ask you: who are your competitors? By extension, who are the peer groups that you should be basing your performance against? Once answering these, what options do you know are available, right now, that can put space between your bank and their business? Further, what options do you need to create in order to stay both relevant, and competitive in the months ahead?

Creating “optionality” is a concept that continues to rattle around in my mind. Indeed, it ties into the concept of franchise value and is one that members of a bank’s board need to prioritize. It opens conversations around delivery methods and channels, business relationships and partnerships — and yes, growth opportunities (be it organic or through acquisition).

As we talked about in Nashville, banks are under enormous pressure to prepare for an unknown future. Ahead of this year’s exclusive in-person event, I came up with three basic questions I find timely and relevant. Take a read and let me know if you agree.

WASHINGTON, DC — Over the past few months, I’ve shared several transformative technology deals in the financial sector on this site and in virtual presentations. From Visa acquiring Plaid to MasterCard picking up Finicity, big name players paid big time premiums to acquire technology companies to boost their games with consumers. As CEOs and their boards wrestle with competitive pressures and explore new paths to remain relevant, a huge announcement in the health space caught my attention. In fact, it reminds me of a recent bank M&A deal.

Why This Deal Matters: The Changing Competitive Landscape

Much as last year’s deal between SunTrust and BB&T — which resulted in Truist — reflected the pressures of our digital-first world, so too does one struck in another heavily regulated (and also incredibly important) industry. This one, between Livongo and Teladoc, impacts the whole digital healthcare market, creating a combined entity worth $38 billion.

As shared on CIO.com, Teladoc already has a significant presence in hospitals, many of whom are white-labeling the Teladoc platform for providing telehealth services, often using the Teladoc physician network to complement their network of doctors within the system.

In parallel, Livongo’s success in remote management of chronic care appears a natural complement to that business. Indeed, their whole-person platform empowers people with chronic conditions to live better and healthier lives.

As the merger release makes clear, “the highly complementary organizations will combine to create substantial value across the healthcare ecosystem, enabling clients everywhere to offer high quality, personalized, technology-enabled longitudinal care that improves outcomes and lowers costs across the full spectrum of health.”

Here, two words stand out: technology-enabled.

Put another way, we are talking about digital transformation, which, as I recall, anchored SunTrust/BB&T’s deal.

Another Example That Scale Is Good — But How You Leverage It Is Key

Last February, BB&T and SunTrust Banks’ all-stock transaction (valued at $66 billion) was the largest U.S. bank merger in over a decade. It spawned Truist, the sixth-largest bank in the U.S. by assets and deposits. In the initial press release, both banks’ CEOs cited the desire for greater scale in order to invest in innovation and technology to create compelling digital offerings.

While Teladoc and Livongo have both been acquiring smaller startups to expand their capabilities in virtual care and digital patient engagement, it appears both are falling in Truist’s steps. Together, the new organization promises to offer a broader set of digitally-enabled services and capabilities across an individual’s health journey.

Given the incredible size of the combined digital health entity, I am reminded of a special episode of Looking Ahead with Keith Pagnani of the law firm Sullivan & Cromwell and Andrew Rymer of the investment bank Centerview Partners. Filmed last year at Nasdaq’s MarketSite, the three of us talked about what’s driving healthcare deals and what the regulatory process looks like for transactions. While we focused on the combination of CVS and Aetna, I think you’ll find the rationale applies for Teladoc and Livongo.

*If you’re interested in M&A and IPO activity in the health sector, our DirectorCorps team recently introduced “The Deal on Healthcare.” A bi-monthly communique, it rounds up the most notable announcements. To sign up for this free newsletter, click here.

Dreaming of a trip to Phoenix, and the Acquire or Be Acquired Conference, next January doesn’t seem so odd this summer.

WORKING FROM HOME — For decades, business leaders began to book their travel to the Arizona desert — for Bank Director’s Acquire or Be Acquired Conference — in early August. As evidenced by the nearly 1,400 at the Arizona Biltmore earlier this year, the annual event has become a true stomping ground for CEOs, executives and board members. Many laud it as the place to be for those that take the creation of franchise value seriously. I’ve even heard it referred to as the unofficial kickoff of banking’s new year.

Just seven months ago, Acquire or Be Acquired once again brought together industry leaders from across the United States to explore merger opportunities, acquisition trends and financial growth ideas. With 418 banks represented, participants considered strategies specific to lending, deposit gathering and brand-building. They talked regulation, met with exceptional fintechs and networked with their peers under sunny skies.

Not one openly worried about a global pandemic.

Yet here we are, all of us dealing with fast-moving challenges and unimaginable risks.

So what can we do to help?

This is the question that proved the catalyst for our new AOBA Summer Series. Indeed, we created this free, on-demand, compilation of thought leadership pieces to provide pragmatic information and real-world insight.

With CEOs and leadership teams being called upon to make decisions they have never been trained for, we realized the type of information typically shared in January has immediate merit this summer. So instead of waiting until winter, this new Summer Series provides both color and context to the tough decisions — those with profound long-term consequences — that confront executives every day.

Ten videos comprise the AOBA Summer Series, with topics appropriate for the C-suite’s or board’s consideration. Streaming on BankDirector.com, we talk about how important scale has become in the banking industry… how one’s technology strategy cannot be delegated… how it certainly seems that there will be banks that come out of this in a bigger, stronger state. Here’s a screen-grab of what you’ll come across:

In one-on-one conversations like these, we acknowledge how net interest margins are compressing — which will drive up efficiency ratios — and credit costs are climbing. And we look at leadership, appreciating that many are leading in new, more positive and impactful ways. In addition, this new series provides:

A SNAPSHOT ON CURRENT CONDITIONS At our January Acquire or Be Acquired Conference, Tom Michaud, President & CEO, Keefe, Bruyette & Woods, A Stifel Company, provided his outlook for the industry. Now, we ask him to update his perspectives on M&A activity and share his take on the potential implications of the pandemic.

HOW FINTECHS FIT A growing number of technology companies have been founded to serve the banking industry. Not all of them have what it takes to satisfy bankers. During various sessions we learn how a variety of banks approach innovation — and the specific attributes a leadership team should look for in a new fintech relationship.

THE LEVERS OF VALUE CREATION With nCino’s CMO, Jonathan Rowe, our Editor-in-Chief talks about the levers of creating value vis-a-vis the flywheel of banking. Together, they explain how certain technologies promote efficiency, which promotes prudence, thereby promoting profits, which can then be invested in technology, starting the cycle all over again.

Hearing from investment bankers, attorneys, accountants, fintechs, investors and — yes, other bankers — about the outlook for growth and change in the industry proves a hallmark for Acquire or Be Acquired, be it in-person or online.

As this new series makes clear, The future is being written in ways unimaginable just a few months ago. We invite you to watch how industry leaders are making sense of the current chaos for free on BankDirector.com.

PHOENIX —When Bank Director first introduced our Acquire or Be Acquired Conference 25 years ago, some 15,000 banks operated in the United States. While that number has shrunk considerably — there are 5,120 banks today — the inverse holds true for the importance of this annual event. What follows are two short videos from our first day in the desert that surface a few key ideas shared with our 1,300+ attendees.

Three Interesting Stats:

Of the 5,120 banks in the U.S., 4,631 are under $1Bn in asset size and 489 are over that amount.

Two years ago, we talked about the sweet spot of banking being banks between $5B and $10B in asset size; now, its those with assets of $50B+.

Digital channels drive 35% of primary banking relationship moves, while branches drive only 26%.

_ _ _

Whether you are able to join us in person or are simply interested in following the conference conversations via our social channels, I invite you to follow@AlDominick@BankDirectorand@Fin_X_Techon Twitter. Search & follow#AOBA19to see what is being shared with and by our attendees.

WASHINGTON, DC — So, there’s this guy named Warren Buffet who has a few thoughts on business. This Nebraska-based investor once opined “I’d rather pay a fair price for a wonderful company than a wonderful price for a fair company.” Quite sagacious — and appropriate to share in advance of our 25th annual Acquire or Be Acquired Conference which takes place January 27-29 at the JW Marriott Phoenix Desert Ridge in Arizona.

Since we last hit the desert, several regional banks have been active in the M&A market — and may continue to look for merger opportunities to build up scale. In addition, we’ve seen how tax reform had a big impact on the industry, with many making investments to grow their business.

Now, with the government shutdown straining our economy, big banks beating community banks on the digital front and shifting team & cultural dynamics, we have a lot of ground to cover over two-and-a-half days. Interested to see what we have planned? Take a look at the full agenda.

While I am excited to reconnect with quite a few folks, I am particularly interested in a number of strategic issues that will be discussed. For instance:

Since the stock market doesn’t always reward longer-term thinking, what does a bank’s CEO needs to focus on, especially with many stocks being valued as if a recession is imminent;

How can regional and local banks boost their deposits given the biggest banks 2018 deposit gather successes;

How laggards to the digital movement can catch up with their peers? (One suggestion: take a look at Finxact, a “Tesla-like” financial technology company that offers an innovative, open-core banking platform. I believe it will quickly become a legitimate challenger to FIS, Jack Henry and Fiserv);

The M&A outlook for 2019;

How institutions can gain/acquire/rent the skills needed to vet and negotiate with potential FinTech partners;

When we might see IPOs — realizing the SEC has to re-open before this occurs; and

How many new bank applications will be approved by the FDIC, realizing that 14 were last year.

For those joining us in Arizona, I encourage men to bring a sports coat or a jacket for the evenings as we plan to be outside for our receptions and the desert quickly cools off once the sun sets. In addition, the rumors of people being in their seats at 7:15 – 7:30 on Sunday morning? 100% true. We start at 7:45 AM and there are quite a few pictures from last January’s event if you need visual proof.

Finally, the digital materials for the conference can be found on BankDirector.com. Once you register on-site, you’ll be given a passcode to access the materials that can be used throughout the event.

_ _ _

Whether you are able to join us in person or are simply interested in following the conference conversations via our social channels, I invite you to follow @AlDominick@BankDirector and @Fin_X_Tech on Twitter. Search & follow #AOBA19 to see what is being shared with and by our attendees. If you are going to be with us in Arizona and we’re not already connected here on LinkedIn, drop me a note and let’s fix that.

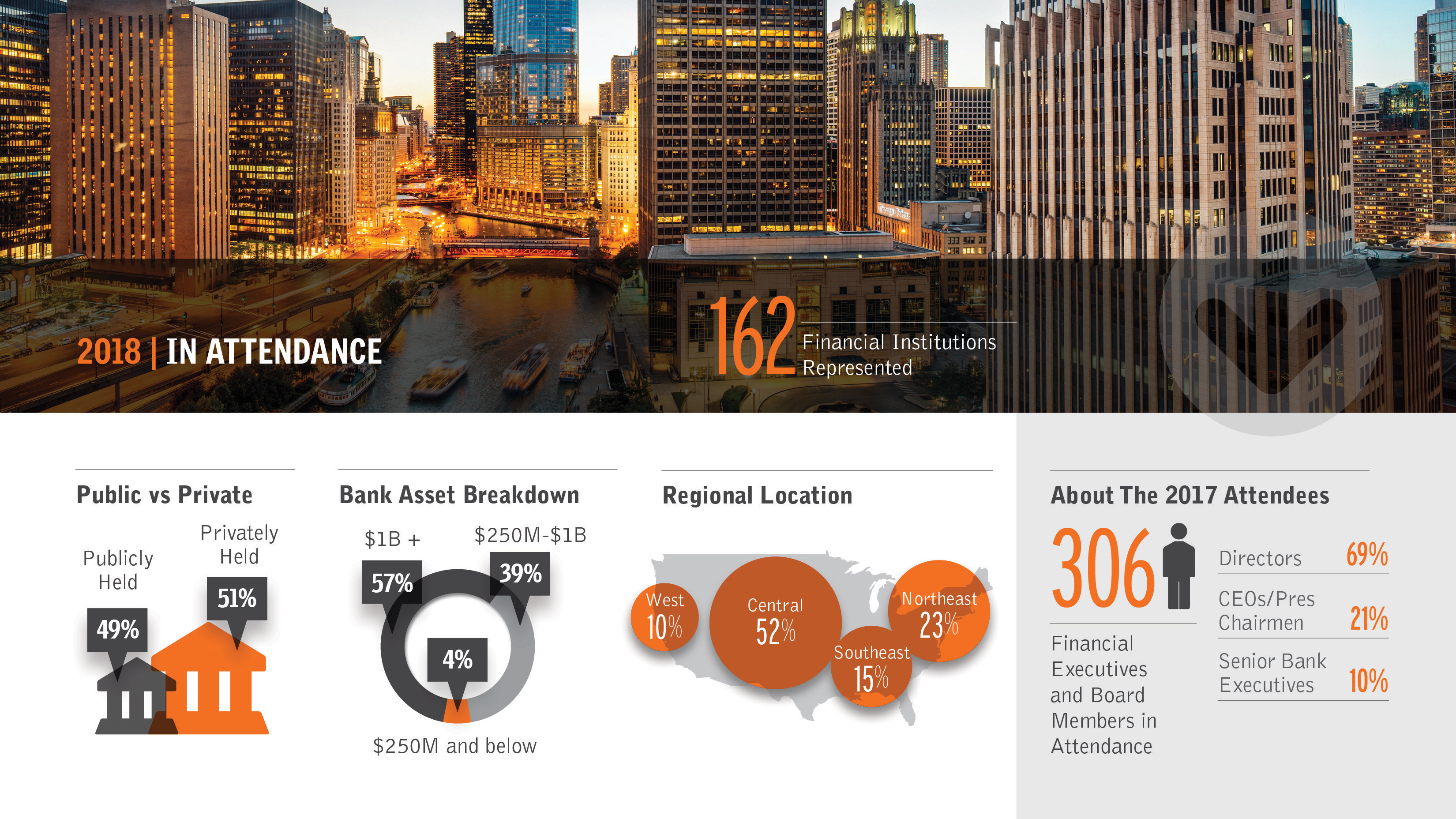

WASHINGTON, DC — Can community banks out-compete JP Morgan, BofA and Wells Fargo? This is the elephant in the room awaiting 853 bank executives and board members — representing 432 Banks — at our upcoming Acquire or Be Acquired Conference. The lights don’t officially come up on our 25th annual event at the JW Marriott Phoenix Desert Ridge until Sunday, January 27. So in advance, three big questions I anticipate fielding in the desert.

Does 2019 Become the Year of BigTech?

As noted by H2 Ventures and KPMG, Amazon is providing payment services and loans to merchants on its platform, while Facebook recently secured an electronic money licence in Ireland. Alibaba, Baidu and Tencent have become dominant operators in China’s $5.5 trillion payments industry. Add in Fiserv’s recent $22B acquisition of First Data and Plaid’s of Quovo and we might be seeing the start of a consolidation trend in the financial technology sector. Will such investments and tie-ups draw the attention of big technology companies to the financial services industry?

Has the window to sell your bank already closed?

When I heard the rumor that BBVA might be buying UK-based Atom Bank — one of the proverbial European challenger banks — I started to look at acquisition trends here in the U.S. Case-in-point, we put together the following graphic in December for BankDirector.com

We know that some community banks have been holding out hopes of higher pricing multiples or for a strategic partner. These institutions might find the window of opportunity to stage an exit isn’t as open as it was just a few years ago. This doesn’t mean the window has shut — but I do think an honest assessment of what’s realistic, at the board level, is appropriate.

Wither the bond market?

A NY Times op-ed piece posits that the bond market reveals growing cracks in the financial system. Authored by Sheila Bair, the former chairwoman of the FDIC, and Gaurav Vasisht, director of financial regulation at the Volcker Alliance, it warns that “regulators are not doing enough to make sure that banks are prepared.” While the duo calls for thicker capital cushions for big banks and tighter leveraged loan underwriting standards, I wonder how executives joining us in Arizona feel about this potential threat to our economy?

_ _ _

As the premier bank M&A event for bank CEOs, senior management and board members, Bank Director’s 25th annual Acquire or Be Acquired Conference brings together key bank leaders from across the country to explore merger & acquisition strategies and financial growth opportunities. If you’re joining us in the desert, I’ll share a few FYIs later this week. If you’re unable to join us in Phoenix, AZ, I’ll be tweeting from @aldominick and using #AOBA19 when sharing on social platforms like LinkedIn.

The challenges faced by financial institutions today are as numerous as they are nuanced. Be it data security, emerging technology, fraud, crisis management and/or the effectiveness of internal controls, I opened the 12th annual Bank Audit & Risk Committees Conference by laying out a number of key governance, risk and compliance issues and trends.

CHICAGO — While a sophomore at Washington & Lee University, a professor loudly (and unexpectedly) chastised a close friend of mine for stating the obvious. With a wry laugh, he thanked my classmate “for crashing through an open door.” Snark aside, his criticism became a rallying cry for me to pause and dive deeper into apparently simple questions or issues.

I shared this anecdote with some 400 attendees earlier today; indeed, I teed up Bank Director’s annual program by reminding everyone from the main stage that:

We’re late in the economic cycle;

Rates are rising; and

Pressure on lending spreads remains intense.

Given the composition of this year’s audience, I acknowledged the obvious nature of these three points. I did so, however, in order to surface three trends we felt all here should have on their radar. I followed that up with three emerging issues to make note of.

TREND #1:

Big banks continue to roll-out exceptional customer-facing technology.

Wells Fargo has been kicked around a lot in the press this year, but to see how big banks continue to pile up retail banking wins, take a look at Greenhouse by Wells Fargo, their app designed to attract younger customers to banking.

TREND #2:

Traditional core IT providers — Fiserv, Jack Henry & FIS — are under fire.

As traditional players move towards digital businesses, new players continue to emerge to help traditional banks become more nimble, flexible and competitive. Here, FinXact and Nymbus provide two good examples of legitimate challengers to legacy cores.

TREND #3:

Amazon lurks as the game changer.

Community banker’s fear Amazon’s potential entry into this market; according to Promontory Interfinancial Network’s recent business outlook, it is their greatest threat.

In addition to these trends, I surfaced three immediate issues that banks must tackle

ISSUE #1:

Big banks attract new deposits at a much faster pace than banks with less than $1 billion assets.

If small banks can’t easily and efficiently attract deposits, they basically have no future. ‘Nuf said.

ISSUE #2: Bank boards need to know if they want to buy, sell or grow independently.

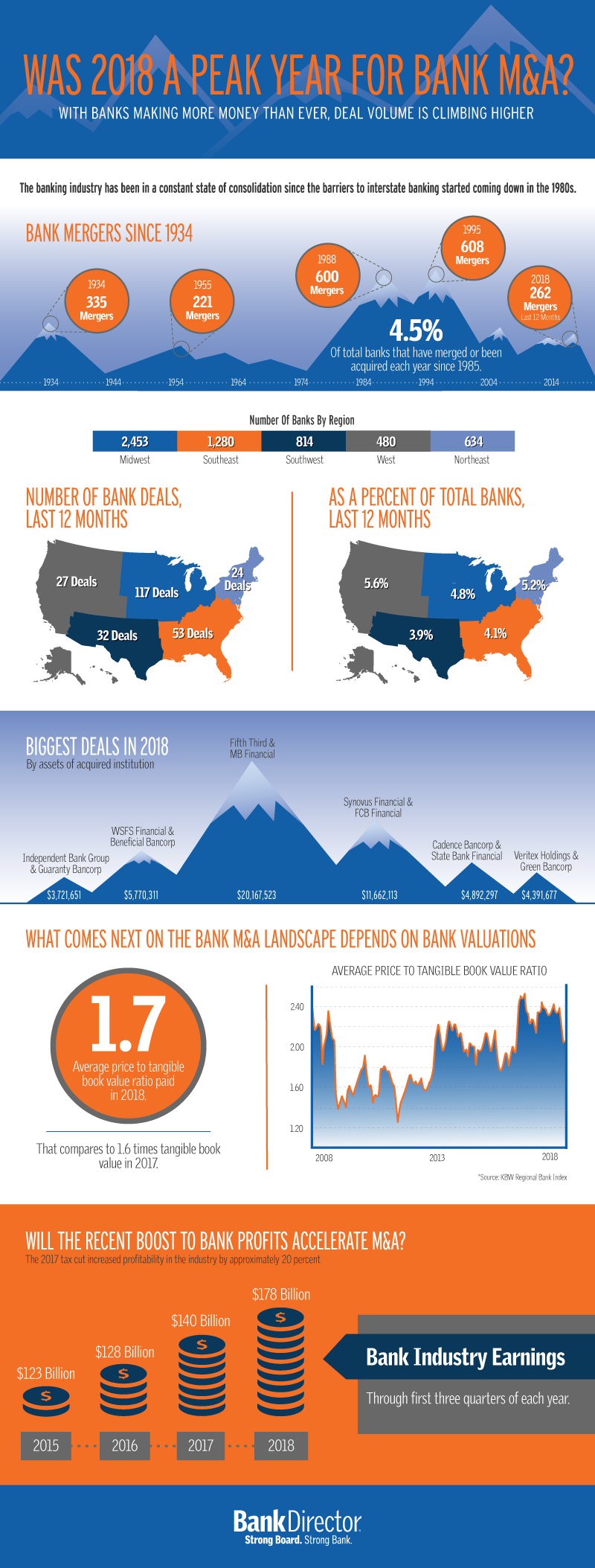

In a recent newsletter, Tom Brown of Second Curve Capital opined that “if you have less than $5 billion in assets, an efficiency ratio north of 65%, deposit costs above 60 basis points, and earn a return on equity in the single digits, this really is time to give some thought to selling.” As I shared on LinkedIn yesterday, the 3 biggest bank M&A deals of the year took place in May: Fifth Third Bancorp’s $4.6 billion purchase of MB Financial, Cadence Bancorp’s $1.3 billion acquisition of State Bank Financial and Independent Bank Group’s $1 billion agreement to buy Guaranty Bancorp. I don’t see the pace of consolidation slowing any time soon — and know that banks need to ask if they want (and can) be buyers or sellers.

ISSUE #3:

The risk of data breaches across industries continues to increase.

Be it risk management, internal control or third-party security considerations, every aspect of an institution is susceptible to a data breach — and managing these threats and identifying appropriate solutions takes a village that includes the most senior leaders of an organization.

##

Just as banks need to develop their audit and risk capabilities, skills and talents, so too do officers and directors have both an opportunity and the responsibility to stay abreast of various trends and topics. Bank Director’s event continues tomorrow with some fascinating presentations. To see what’s been shared already, take a look at Twitter, where I’m tweeting using @aldominick and #BDAudit18.

When it comes to talk about bank mergers and acquisitions, It has been written that the questions rarely change — but the conversations prove irresistible.

PHOENIX, AZ — If you’re with us here at the Arizona Biltmore for Bank Director’s annual Acquire or Be Acquired Conference, you’ve heard that banks with low‐cost core deposits continue to attract interest from acquirers. So as banks wrestle with increased funding costs, that observation sparked an idea about what constitutes the “three Cs” of banking today:

Compliance

Cost Control

Consolidation

For instance, having good on-going relations with one’s regulators is hugely important. In fact, I heard several prominent attorneys share that regulatory risk remains the greatest obstacle to completing an M&A deal. So having the bank in position to act quickly and confidently when an opportunity arises is a major advantage in today’s competitive M&A environment. I take this to mean no enforcement actions, satisfactory CRA, good HCR results, etc.

As was discussed yesterday afternoon, when an acquirer can present a credible narrative that a potential deal is consistent with a well-considered strategy — and that the company has the infrastructure appropriate to the new organization, you find a well received merger.

In terms of consolidation, we saw a number of presentations note the 261 bank M&A deals, worth an aggregate $26.38 billion, announced in 2017. As a point of reference, 241 deals were announced — worth an aggregate $26.79 billion — in 2016. According to S&P Global Market Intelligence, the median deal value-to-tangible common equity ratio climbed significantly in 2017 to 160.6%, compared to 130.6% for 2016. Last December alone, 32 deals worth a combined $1.84 billion were announced and the median deal value-to-tangible common equity ratio was 156.5%.

Throughout the fourth quarter, there were 74 bank deals announced in the US, which was the most active quarter since 83 deals were announced in the fourth quarter of 2015. However, last quarter’s $4.4 billion aggregate deal value was the lowest since the third quarter of 2015, which totaled $3.43 billion.

These are by no means the only Cs in banking. Credit, core technology providers, (tax) cuts… all, huge issues. So along these lines, I made note of a few more issues for buyers, for sellers — and for those wishing to remain independent. Take a look:

If you are interested in following the final day of the conference via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector, or search #AOBA18 to see what is being shared with (and by) our nearly 1,200 attendees.

PHOENIX, AZ — For all the talk of bank consolidation, there are still 5,700+ banks in the United States. But let’s not kid ourselves. For many community banks today, earnings pressures + regulatory and compliance costs + the continued impact of technology = a recurring challenge.

While the number of banks in business will inevitably shrink over the next 10 years — perhaps being cut in half — I remain bullish on the overall future of this industry. If December’s tax reform spurs capital spending and job creation by small- and medium-sized businesses, many of the banks joining us here in Arizona stand to benefit. But will the recent tax cut induce companies to invest more than they already planned to? This is but one of a number of questions I look forward to asking on stage through the first day of Bank Director’s Acquire or Be Acquired Conference.

Below, ten more questions I anticipate asking:

Are FinTechs the industry’s new de novos?

What does it mean that the banking world is deposit rich yet asset poor?

Why are certain credit unions thinking about about buying banks?

In terms of technology spending levels, where are dollars being earmarked and/or spent?

With respect to small business lending, do credit unions or FinTechs pose a more immediate challenge to community banks?

What is an appropriate efficiency ratio for a bank today?

Will big M&A buyers get back in the game this year?

What are some of the critical items in due diligence that are under appreciated?

What does an activist investor look for in a bank?

Is voice recognition the next huge source of growth for banks?

We have an exciting — and full day — coming up at the Arizona Biltmore. To keep track of the conversations via Twitter, I invite you to follow @AlDominick@BankDirector and @Fin_X_Tech. In addition, to see all that is shared with (and by) our attendees, we’re using the conference hashtag #AOBA18.

We could see over 200 merger transactions despite a declining number of banks in 2017.

There is a clear trend on M&A pricing multiples being driven by bank profitability and asset quality.

For banks, too little capital is not the only issue — too much capital and the inability to produce sufficient returns on capital is equally problematic.

_ _ _

What is my bank worth? How will the changing tax environment affect bank values? When is the right time to buy (or sell) a bank? What are the most significant factors affecting bank value? These were just some of the questions surfaced this morning here in Arizona. In this video recap of Sunday morning’s presentations at Bank Director’s Acquire or Be Acquired Conference, I share a few observations about the conversations taking place around issues such as these.

Given the focus of this three-day event, I anticipate many subsequent presentations building off of these points. For those interested in issues such as these, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and its @Fin_X_Tech platform, and search & follow #AOBA17 to see what is being shared with (and by) our attendees.

In the face of this month’s political transitions, bank executives and their boards face some major issues without clear answers. For instance, many continue to speculate on the Fed’s interest rate hikes while others pontificate on potential regulatory changes (hello CFPB). While convenient to cite November’s election results, keep in mind that we, as an industry, were already in a period of significant transformation. Still, it’s a titanic-sized understatement to say Republican presidential nominee Donald Trump’s surprise victory shook up the world.

While change remains a constant in life, I am personally and professionally excited to return to the Arizona desert later this month for a great tradition: Bank Director’s annual Acquire or Be Acquired Conference. With a record turnout joining us at “AOBA,” I’ve begun to assess various business models of institutions I know will be represented. For instance, those categorized by:

Organic Growth vs. Acquisitive Growth;

Branch Light Model vs. Traditional Models; and

CRE Focused Lenders vs. C&I Focused Lenders.

I am finding there are multiple dimensions to such business structures — and I anticipate conversations later this month will help me to better understand how the market values such companies.

As AOBA helps participants to explore their financial growth options, I am keen to hear perspectives on the “right size” of a bank today — especially if certain asset-based constraints (think $10B, $50B) are removed. Given a number of recent conversations, I expect increased IPOs and M&A activity in the banking space and look forward to hearing the opinions of others.

Finally, with the advance of digital services, I’m curious how technology trends might impact bank M&A, and more broadly, banking as a whole given the impact on branch networks. Indeed, as branches become less important, they become less valuable… which impacts deal valuations and pricing going forward.

According to Bank Director’s 2017 M&A Survey, price is the top reason that potential buyers and sellers have walked away from a deal in the past three years.

With the final days of November upon us, we are a mere 61 days away from hosting Bank Director’s annual Acquire or Be Acquired Conference. This three-day event explores the various financial growth options available to a bank’s CEO, executives and board members; accordingly, I thought to share some highlights from our just-released Bank M&A Survey that resonate with this audience.

This research project — sponsored by Crowe Horwath LLP and led by our talented Emily McCormick — reflects the opinions of 200+ CEOs, CFOs, Chairmen and directors of U.S. banks. As Rick Childs, a partner at Crowe, and someone I respect for his opinions and experiences shares, “good markets and good lending teams are the keys for many acquirers, and are the starting point for their analysis of potential bank partners.” While we cover a lot of ground with this survey, below are five points that stood out to me:

An increasing number of respondents feel that the current environment for bank M&A is stagnant or less active: 45% indicate that the environment is more favorable for deals, down 17 points from last year’s survey.

46% indicate that their institution is likely or very likely to purchase another bank by the end of 2017.

25% report that they’re open to selling the bank, considering a sale or actively seeking an acquirer. Of these potential sellers, 54% cite regulatory costs as the reason they would sell the bank, followed by shareholder demand for liquidity (48%) and limited growth opportunities (39%).

Price, at 38%, followed by cultural compatibility, at 26%, remain the two greatest challenges faced by boards as they consider potential acquisitions. Price is identified as the top reason that potential buyers and sellers have walked away from a deal in the past three years.

45% report that they are seeing a deterioration in loan underwriting standards within the industry, leading to possible credit quality issues in the future.

Driven by shareholder pressures in a low-growth and highly regulated environment, some community banks could be seeking an exit in the near future. But which banks are positioned to get the best price in today’s market? This survey provides potential answers to that question — foreshadowing certain conversations I’m sure will occur in January during our 23rd annual Acquire or Be Acquired conference.

##

My thanks to Rick and his colleagues at Crowe for their continued support of this research project. To see past year’s results — and other board-level research reports we’ve shared — I invite you to take a look at the free-to-access research section on BankDirector.com