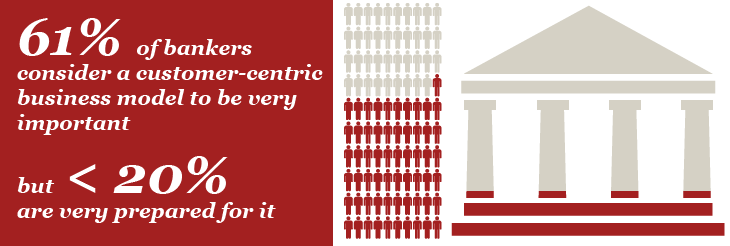

When I think about top performing banks, I typically consider those with the strongest organic growth in terms of core revenue, core noninterest income, core deposit growth and loan growth. Sure, there has been a lot of talk about growing through acquisition (heck, last week’s post, “Seeking Size and Scale” looked at BB&T’s recent acquisitions and my monthly column on BankDirector.com was entitled “Why Book Value Isn’t the Only Way to Measure a Bank“). But going beyond M&A, I’m always interested to dive into the strategies and tactics that put profits on a bank’s bottom line.

Build Your Brand or Build Your Branch

Earlier in the week, KBW’s Global Director of Research and Chief Equity Strategist, Fred Cannon, shared a piece entitled “Branch vs. Brand.” As he notes, “branch banking in the U.S. is at an inflection point; the population per branch has reached a record level in 2014 and is likely to continue to increase indefinitely. The volume of paper transactions peaked long ago and with mobile payment now accelerating the need for branches is waning. As a result, many banks see closing branches as a way to cut costs and grow the bottom line. However, branches have served as more than transactional locations for banks. The presence of branch networks has projected a sense of identity, solidity and ubiquity to customers that has been critical to maintaining a bank’s brand.” He then poses this doozy of a question:

“If branch networks are reduced, what is the replacement for a bank’s identity?”

Fred and his colleagues at KBW believe banks need to replace branches with greater investments in brand. As he shares, “some of this investment will be in marketing, (as) a brand is more than a logo. We believe banks will also need to invest in systems, people, and processes to project the sense of identity, solidity, and ubiquity that was projected historically by branch networks.”

United Bank, An Example of a High-Performing Bank

One example of a bank that I think is doing this well is United Bank. On Wednesday, I had the chance to check out their new financial center in Bethesda, MD. With dual headquarters in Washington, DC and Charleston, WV, the $12.1 billion regional bank holding company is ranked the 48th largest bank holding company in the U.S. based on market capitalization. NASDAQ-listed, they boast an astonishing 41 consecutive years of dividend increases to shareholders – only one other major banking company in the USA has achieved such a record. Their acquisition history is impressive — as is their post-integration success. United continues to outperform its peers in asset quality metrics and profitability ratios and I see their positioning as an ideal alternative to the offices Wells Fargo, SunTrust and PNC (to name just three) operate nearby.

A Universal Priority

Clearly, United’s success reflects a superior long-term total return to its shareholders. While other banks earn similar financial success, many more continue to wrestle with staying both relevant and competitive today. Hence my interest in Deloitte’s position that “growth will be a universal priority in 2015, yet strategies will vary by bank size and business line.” A tip of the hat to Chris Faile for sharing their 2015 Banking Outlook report with me. Released yesterday, they note banks may want to think about:

- Investing in customer analytics;

- Leveraging digital technologies to elevate the customer experience in both business and retail banking;

- Determining whether or not prudent underwriting standards are overlooked; and

- Learning from nonbank technology firms and establish an exclusive partnership to create innovation and a competitive edge.

With most banks exhibiting a much sharper focus on boosting profitability, I strongly encourage you to see what they share online.

Aloha Friday!