By Al Dominick, CEO of DirectorCorps (parent co. to Bank Director & FinXTech) | @aldominick

Quickly:

- I’m in from Dallas at the Consumer Bankers’ Association “CBA Live!”

- Thanks to Richard Hunt, the CEO of the CBA, for inviting me to participate. Richard spoke at our Acquire or Be Acquired conference in January + I hope to live up to his great speaking standards when I’m given a mic tomorrow.

- The rapid pace of change in the financial sector took center stage during yesterday’s opening session.

_ _ _

Since arriving in Big D on Sunday evening, I’ve met quite a few interesting men & women from great financial institutions at this annual event for the retail banking industry. This year, more than 1,300 are at the Gaylord Texan (with some 550 being senior-level bankers) to talk shop. Personally, I’m looking forward to presenting on “Economic States of America” with Amy Crews Cutts (Chief Economist, Equifax), Robert Dye (Chief Economist) of Comerica Bank and Cathy Nash, the CEO of Woodforest National Bank tomorrow morning. From credit trends to banking consolidation, if you’re in Dallas, I invite you to join us for this Super Session as we explore the economic state of our union.

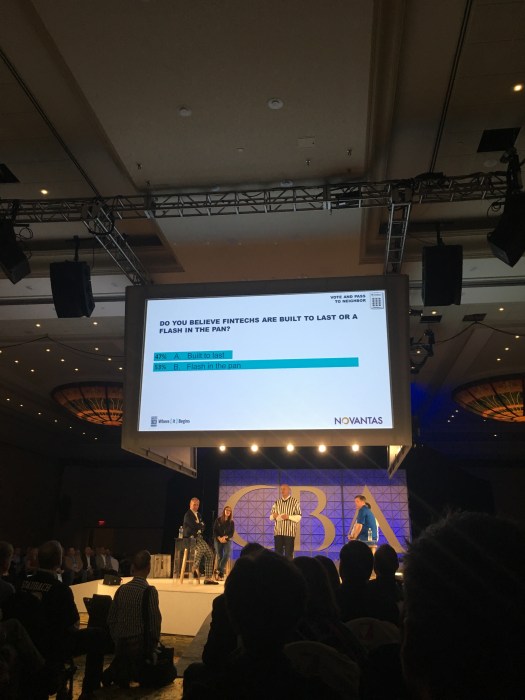

Before then, I thought to share a few interesting takeaways from a “FinTech vs. Bank” general session that pit SoFi and Kabbage “against” PNC and BBVA. As part of the panel discussion, CBA posed a number of interesting questions to the audience; most notably, “do you believe fintechs are built to last.” Given our upcoming FinXTech Summit in NYC, I thought the answer (which reflects the thoughts of many of the biggest banks in the U.S.) was interesting, but not surprising.

Further, I found the results of this question pretty telling (given we asked a similar question at this year’s Acquire or Be Acquired conference and received a similar response from an audience of CEOs, CFOs, and members of a bank’s board).

Finally, I think the results of this question best represent the types of conversations I’ve found myself in when I explain what I do + who I meet with.

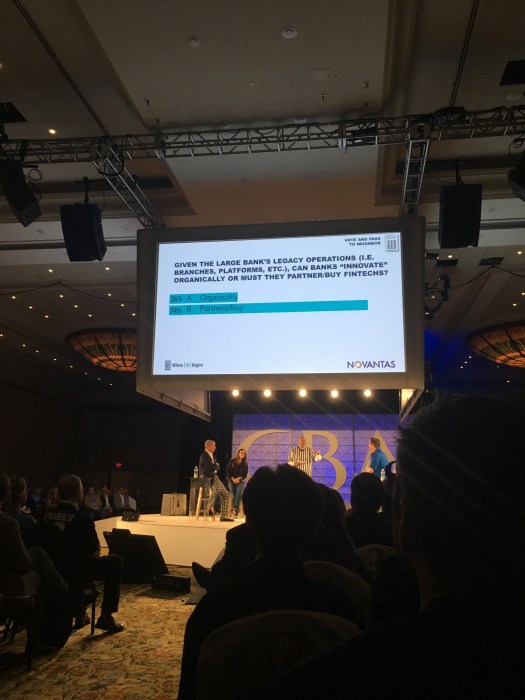

As I’ve shared in recent posts, an increasing number of financial institutions are using partnerships with technology companies to improve operations and better meet customer needs. Given the input on these questions from various heads of retail, product lines and product development + compliance, risk and internal audit, I feel these three pictures are worth noting — and sharing. Agree or disagree? Feel free to leave a comment…