WASHINGTON, DC — Last month, our team celebrated ten years of “Bank Director 2.0.” As I look back on what we’ve accomplished, a few projects stand out. Today, I’m shining a light on the development of our FinXTech Platform, which we built specifically for financial institutions.

Bank Director’s FinXTech debuted on March 1, 2016 at Nasdaq’s MarketSite in Times Square. Positioned at the intersection of Financial Institutions and Technology Leaders, FinXTech connects key decision makers across the financial sector around shared areas of interest.

We initially focused on bank technology companies providing solutions geared to Security, leveraging Data + Analytics, making better Lending decisions, getting smarter with Payments, enhancing Digital Banking, streamlining Compliance and/or improving the Customer Experience.

As our brand (and team) grew, we heard from a number of bank executives about the challenges they faced in discovering potential technology partners and solutions. To help solve this issue, we built FinXTechConnect.

Sorting through the technology landscape is no easy feat. Nor is finding, comparing and vetting potential technology partners. But week-by-week, and month-by-month, we added to this proprietary platform by engaging with bankers and fintech executives alike. All the while, asking (whenever we could) bankers who they wanted to learn more about at events like our annual Summit or Experience FinXTech events.

Banks today are in the eye of a digital revolution storm. A reality brought about, in no small part, by this year’s Covid-19 pandemic. So I am proud that the work we do helps banks make smarter business decisions that ultimately help their clients and communities. To wit, the various relationships struck up between banks and fintechs to turn the SBA’s PPP program into a reality.

As we look ahead, I’m excited to see Bank Director’s editorial team continue to carefully vet potential partners with a history of financial performance and proven roster of financial industry clients. For those companies working with financial institutions that would like to be considered for inclusion in FinXTech Connect, I invite you to submit your company for consideration.

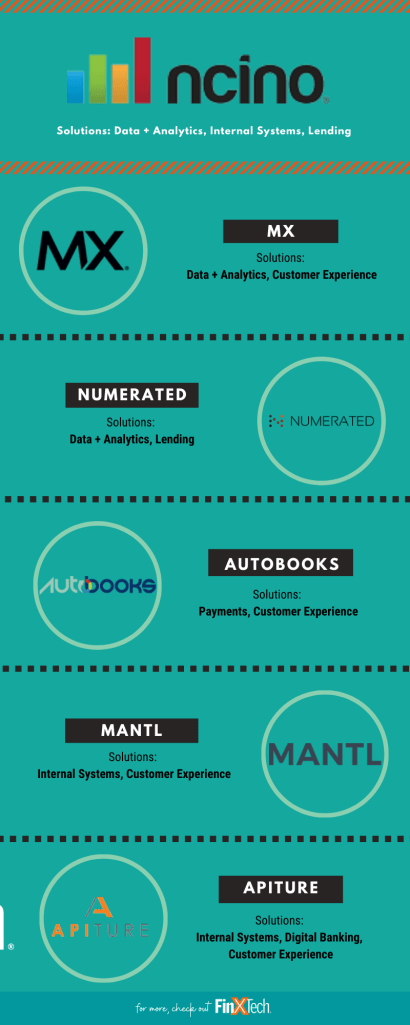

WASHINGTON, DC — With this week’s news that nCino is readying itself for an IPO, I thought to postulate about who “the next nCino” might be in the fintech space. By this, I mean the tech company about whom bank executives cite as doing right by traditional institutions.

For context, nCino developed a cloud-based operating system for financial institutions. The company’s technology enables both customers and financial institutions to work on a single platform that’s optimized for both retail and commercial accounts. In simple terms, they provide everything from retail and commercial account opening to portfolio management for all of a bank’s loans.

In its IPO filing, the company says it works with more than 1,100 financial institutions globally — whose assets range in size from $30 million to $2 trillion. Personally, I remember their start and been impressed with their growth. Indeed, I’ve known about nCino since its early Live Oak Bankdays. I’ve gotten to know many on their executive team, and just last Fall shared a stage with their talented CEO, Pierre Naudé, at our annual Experience FinXTech conference in Chicago.

Al Dominick, CEO of Bank Director + FinXTech, Frank Sorrentino, Chairman & CEO of ConnectOne Bank and Pierre Naude, CEO of nCino at 2019’s Experience FinXTech Conference in Chicago, IL.

So as I think about who might become “the next” nCino in bankers’ minds across the United States, I begin by thinking about those offering solutions geared to a bank’s interest in Security, leveraging Data + Analytics, making better Lending decisions, getting smarter with Payments, enhancing Digital Banking, streamlining Compliance and/or improving the Customer Experience. Given their existing roster of bank clients, I believe the “next nCino” might be one of these five fintechs:

While I have spent time with the leadership teams from each of these companies, my sense that they might be “next” reflects more than personal insight. Indeed, our FinXTech Connect platform sheds light on each company’s work in support of traditional banks.

For instance, personal financial management (PFM) tools are often thought of as a nice perk for bank customers, designed to improve their experience and meet their service expectations. But when a PFM is built with data analytics backing it, what was seen as a perk can be transformed into a true solution — one that’s more useful for customers while producing revenue-generating insights for the bank. The money management dashboard built by Utah-based MX Technologies does just that.

Spun out of Eastern Bank in 2017 (itself preparing for an IPO), Boston-based Numerated designed its offering to digitize a bank’s credit policy, automate the data-gathering process and provide marketing and sales tools that help bank clients acquire new small business loans. Unlike many alternative lenders that use a “black box” for credit underwriting, Numerated has an explainable credit box, so its client banks understand the rules behind it.

Providing insight is something that Autobooks helps small business with. As a white-label product that banks can offer to their small-business customers, Autobooks helps to manage business’s accounting, bill pay and invoicing from within the institution’s existing online banking system. Doing so removes the need for small businesses to reconcile their financial records and replaces traditional accounting systems such as Quickbooks.

The New York-based MANTL developed an account opening tool that comes with a core integration solution banks can use to implement this and other third- party products. MANTL allows a bank to keep its existing core infrastructure in place while offering customers a seamless user experience. It also drives efficiency & automation in the back-office.

Finally, Apiture’s digital banking platform includes features such as digital account opening, personal financial management, cash flow management for businesses and payments services. What makes Apiture’s business model different from most, though, is that each of those features can also be unbundled from the platform and sold as individual modules that can be used to upgrade any of the bank’s existing systems.

Of course, these are but five of hundreds of technology companies with proven track records of working with financial institutions. Figuring out what a bank needs — and who might support them in a business sense — is not a popularity contest. But I’m keen to see how banks continue to engage with these five companies in the months to come.

The challenges faced by financial institutions today are as numerous as they are nuanced. Be it data security, emerging technology, fraud, crisis management and/or the effectiveness of internal controls, I opened the 12th annual Bank Audit & Risk Committees Conference by laying out a number of key governance, risk and compliance issues and trends.

CHICAGO — While a sophomore at Washington & Lee University, a professor loudly (and unexpectedly) chastised a close friend of mine for stating the obvious. With a wry laugh, he thanked my classmate “for crashing through an open door.” Snark aside, his criticism became a rallying cry for me to pause and dive deeper into apparently simple questions or issues.

I shared this anecdote with some 400 attendees earlier today; indeed, I teed up Bank Director’s annual program by reminding everyone from the main stage that:

We’re late in the economic cycle;

Rates are rising; and

Pressure on lending spreads remains intense.

Given the composition of this year’s audience, I acknowledged the obvious nature of these three points. I did so, however, in order to surface three trends we felt all here should have on their radar. I followed that up with three emerging issues to make note of.

TREND #1:

Big banks continue to roll-out exceptional customer-facing technology.

Wells Fargo has been kicked around a lot in the press this year, but to see how big banks continue to pile up retail banking wins, take a look at Greenhouse by Wells Fargo, their app designed to attract younger customers to banking.

TREND #2:

Traditional core IT providers — Fiserv, Jack Henry & FIS — are under fire.

As traditional players move towards digital businesses, new players continue to emerge to help traditional banks become more nimble, flexible and competitive. Here, FinXact and Nymbus provide two good examples of legitimate challengers to legacy cores.

TREND #3:

Amazon lurks as the game changer.

Community banker’s fear Amazon’s potential entry into this market; according to Promontory Interfinancial Network’s recent business outlook, it is their greatest threat.

In addition to these trends, I surfaced three immediate issues that banks must tackle

ISSUE #1:

Big banks attract new deposits at a much faster pace than banks with less than $1 billion assets.

If small banks can’t easily and efficiently attract deposits, they basically have no future. ‘Nuf said.

ISSUE #2: Bank boards need to know if they want to buy, sell or grow independently.

In a recent newsletter, Tom Brown of Second Curve Capital opined that “if you have less than $5 billion in assets, an efficiency ratio north of 65%, deposit costs above 60 basis points, and earn a return on equity in the single digits, this really is time to give some thought to selling.” As I shared on LinkedIn yesterday, the 3 biggest bank M&A deals of the year took place in May: Fifth Third Bancorp’s $4.6 billion purchase of MB Financial, Cadence Bancorp’s $1.3 billion acquisition of State Bank Financial and Independent Bank Group’s $1 billion agreement to buy Guaranty Bancorp. I don’t see the pace of consolidation slowing any time soon — and know that banks need to ask if they want (and can) be buyers or sellers.

ISSUE #3:

The risk of data breaches across industries continues to increase.

Be it risk management, internal control or third-party security considerations, every aspect of an institution is susceptible to a data breach — and managing these threats and identifying appropriate solutions takes a village that includes the most senior leaders of an organization.

##

Just as banks need to develop their audit and risk capabilities, skills and talents, so too do officers and directors have both an opportunity and the responsibility to stay abreast of various trends and topics. Bank Director’s event continues tomorrow with some fascinating presentations. To see what’s been shared already, take a look at Twitter, where I’m tweeting using @aldominick and #BDAudit18.

When it comes to talk about bank mergers and acquisitions, It has been written that the questions rarely change — but the conversations prove irresistible.

PHOENIX, AZ — If you’re with us here at the Arizona Biltmore for Bank Director’s annual Acquire or Be Acquired Conference, you’ve heard that banks with low‐cost core deposits continue to attract interest from acquirers. So as banks wrestle with increased funding costs, that observation sparked an idea about what constitutes the “three Cs” of banking today:

Compliance

Cost Control

Consolidation

For instance, having good on-going relations with one’s regulators is hugely important. In fact, I heard several prominent attorneys share that regulatory risk remains the greatest obstacle to completing an M&A deal. So having the bank in position to act quickly and confidently when an opportunity arises is a major advantage in today’s competitive M&A environment. I take this to mean no enforcement actions, satisfactory CRA, good HCR results, etc.

As was discussed yesterday afternoon, when an acquirer can present a credible narrative that a potential deal is consistent with a well-considered strategy — and that the company has the infrastructure appropriate to the new organization, you find a well received merger.

In terms of consolidation, we saw a number of presentations note the 261 bank M&A deals, worth an aggregate $26.38 billion, announced in 2017. As a point of reference, 241 deals were announced — worth an aggregate $26.79 billion — in 2016. According to S&P Global Market Intelligence, the median deal value-to-tangible common equity ratio climbed significantly in 2017 to 160.6%, compared to 130.6% for 2016. Last December alone, 32 deals worth a combined $1.84 billion were announced and the median deal value-to-tangible common equity ratio was 156.5%.

Throughout the fourth quarter, there were 74 bank deals announced in the US, which was the most active quarter since 83 deals were announced in the fourth quarter of 2015. However, last quarter’s $4.4 billion aggregate deal value was the lowest since the third quarter of 2015, which totaled $3.43 billion.

These are by no means the only Cs in banking. Credit, core technology providers, (tax) cuts… all, huge issues. So along these lines, I made note of a few more issues for buyers, for sellers — and for those wishing to remain independent. Take a look:

If you are interested in following the final day of the conference via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector, or search #AOBA18 to see what is being shared with (and by) our nearly 1,200 attendees.

Until Friday, Thomas Curry, head of the OCC, had taken a firm stance toward FinTechs, making it clear that he would hold them to the standards and regulations written for incumbent financial services institutions. So as the OCC considers the benefits such firms might provide, I’m not surprised the agency will, for the first time, “start granting banking licenses to fintech firms, giving them greater freedom to operate across the country without seeking state-by-state permission or joining with brick-and-mortar banks.”

Now, FinTech is just one area of regulation that is a-changin’. As our Editor-in-Chief, Jack Milligan, recently wrote on BankDirector.com, “one of the more intriguing story lines of the banking industry’s consolidation since the financial crisis is the persistent belief that federal regulators privately want a more concentrated industry with fewer banks because it would be easier for them to supervise, and they signal their support for this laissez-faire policy every time they approve an acquisition.”

Against this backdrop, I am looking forward to hearing Vice President Joe Biden speak at Georgetown’s McDonough School of Business this afternoon. I have a lot of respect for the Vice President, and find his remarks on “The Importance of Sound Financial Sector Regulation” to fit the timely and relevant standards that we prize at Bank Director and FinXTech. Thanks to the business school’s Center for Financial Markets and Policy for inviting me. As appropriate, I will share my takeaways from this presentation via twitter – @aldominick — and with a follow up post on this blog ASAP.

A quick check-in from the Swissotel in Chicago, where we just wrapped up the main day of Bank Director’s 10th annual Bank Audit & Risk Committees Conference. This is a fascinating event, one focused on key accounting, risk and regulatory issues aligned with the information needs of a bank’s Chairman, CEO, Bank Audit Committee, Bank Risk Committee, CFO, CRO and internal auditor. Risk + strategy go hand in hand; today, we spent considerable time debating risk in the context of growing the bank.

Earlier today, while moderating a panel discussion, I referenced a KPMG report that suggests “good risk management and governance can be compared to the brakes of a car. The better the brakes, the faster the car can drive.” With anecdotes like this ringing in my head, allow me to share three key takeaways:

A company’s culture & code of conduct are critical factors in creating an environment that encourages compliance with laws and regulations.

Risk appetite is a widely accepted concept that remains difficult, in practice, to apply.

As a member of the board, do not lose sight of the need to maintain your skepticism.

This year’s program brings together 150+ financial institutions and more then 300 attendees. The demographics reflect the audience we serve, so I thought to share three additional trends. Clearly, boards of directors are under pressure to evolve. Financial institutions need the right expertise and experience and benefit greatly when their directors have diverse backgrounds.

Further, as more regulatory rules are written, board members need to understand what they mean and how they can affect their bank’s business. Finally, technology strategies and risks are inextricably linked to corporate strategy; as such, the level of board engagement needs to increase.

Given the many issues — both known and unknown — a bank faces as our industry evolves, today made clear how challenging it can be for an audit or risk committee member to get comfortable addressing risk and issues. Staying compliant requires a solid defense and appreciation for what’s now. Staying competitive? This requires a sharper focus given near constant pressures to reduce costs while dealing with increasing competition and regulation.

##

To see what we’re sharing on our social networks, I encourage you to follow @bankdirector@fin_x_tech and @aldominick. Questions or comment? Feel free to leave me a note below.

Earlier this month, at Bank Director’s FinTech Day at Nasdaq’s MarketSite in New York City, I noted how many technology firms are developing strategies, practices and tools that will dramatically influence how banking gets done in the future. Concomitantly, I expressed an optimism that banks are learning from these new players, adapting their offerings and identifying opportunities to collaborate with new “digital-first” businesses. Unfortunately, with great opportunity comes significant risk (and today’s post looks at a major one challenging bank CEOs and their boards).

By Al Dominick, President & CEO, Bank Director

To grow your revenue, deposits, brand, market size and/or market share requires both strong leadership and business strategy. Right now, there are a handful of banks developing niche vertical lines of business to compete with the largest institutions. For instance, East West Bancorp, EverBank Financial, First Republic Bank, Opus Bank, PacWest Bancorp, Signature Bank and Texas Capital Bancshares.

Just as compelling as each bank’s approach to growing their business is the idea that new competitors in direct and mobile banking will spur the digitalization of our industry. I am a firm believer that through partnerships, acquisitions or direct investments, incumbents and upstarts alike have many real and distinct opportunities to grow and scale while improving the fabric of the financial community.

However, with myriad opportunities to leverage new technologies comes significant risk, a fact not lost on the bank executives and board members who responded to Bank Director’s 2016 Risk Practices Survey, sponsored by FIS. For the second year running, they indicate that cybersecurity is their top risk concern.

More respondents (34 percent) say their boards are reviewing cybersecurity at every board meeting, compared to 18 percent in last year’s survey, indicating an enhanced focus on cybersecurity oversight. Additionally, more banks are now employing a chief information security officer (CISO), who is responsible for day-to-day management of cybersecurity.

However, the survey results also reveal that many banks still aren’t doing enough to protect themselves—and their customers. Less than 20 percent of respondents say their bank has experienced a data breach, but those who do are just as likely to represent a small institution as a large one, further proof that cybersecurity can no longer be discussed as only a “big bank” concern.

For those thinking about the intersection of fintechs and banks, take a look at our just-released 2016 Risk Practices Survey. This year, we examine risk governance trends at U.S. banks, including the role of the chief risk officer and how banks are addressing cybersecurity. The survey was completed in January by 161 independent directors, chief risk officers (CRO), chief executive officers (CEO) and other senior executives of U.S. banks with more than $500 million in assets.

Key Findings Include:

Sixty-two percent of respondents indicate their bank has used the cybersecurity assessment tool made available by the Federal Financial Institutions Examination Council, and have completed an assessment. However, only 39 percent have validated the results of the assessment, and only 18 percent have established board-approved triggers for update and reporting. FWIW, bank regulators have started to use the tool in exams, and some states are mandating its use.

Seventy-eight percent indicate that their bank employs a full-time CISO, up from 64 percent in last year’s survey.

The majority, at 62 percent, say the board primarily oversees cybersecurity within the risk or audit committee. Twenty-six percent govern cybersecurity within the technology committee.

Forty-five percent indicate that detecting malicious insider activity or threats is an area where the bank is least prepared for a cyberattack or data breach.

Just 35 percent test their bank’s cyber-incident management and response plan quarterly or annually.

Clearly, banks are increasingly relying on complex models to support economic, financial and compliance decision-making processes. Considering the full board of a bank is ultimately responsible for understanding an institution’s key risks — and credibly challenging management’s assessment and response to those risks — I am pleased to share this year’s report as part of our commitment to providing timely & relevant information to the banking community.

With all of the information provided at this year’s Bank Audit & Risk Committees conference(#BDAudit14 via @bankdirector), I think it is fair to write that some attendees might be heading home thinking “man, that was like taking a refreshing drink from a firehose.” As I reflect on my time in Chicago this week, it strikes me that many of the rules and requirements being placed on the biggest banks will inevitably trickle down to smaller community banks. Likewise, the risks and challenges being faced by the biggest of the big will also plague the smallest of the small. Below, I share two key takeaways from yesterday’s presentations along with a short video recap that reminds bankers that competition comes in many shapes and sizes.

The Crown Fountain in Millennium Park

Trust, But Verify

To open her “New Audit Committee Playbook” breakout session, Crowe Horwath’sJennifer Burke reinforced lessons from previous sessions that a bank’s audit committee is the first line of defense for the board of directors and shareholders. Whether providing oversight to management’s design and implementation with respect to internal controls to consideration of fraud risks to the bank, she made clear the importance of an engaged and educated director. Let me share three “typical pitfalls” she identified for audit committee members to steer clear of:

Not addressing complex accounting issues;

Lack of open lines of communication to functional managers; and

Failure to respond to warning event.

To these points, let me echo her closing remarks: it is imperative that a board member understand his/her responsibility and get help from outside resources (e.g. attorneys, accountants, consultants, etc.) whenever needed.

Learn From High-profile Corporate Scandals

Many business leaders are increasingly aware of the need to create company-specific anti-fraud measures to address internal corporate fraud and misconduct. For this reason, our final session looked at opening an investigation from the board’s point-of-view. Arnold & Porter’s Brian McCormally kicked things off with a reminder that the high-profile cyber hacks of Neiman Marcus and Target aren’t the only high-profile corporate scandals that bankers can learn from. The former head of enforcement at the OCC warned that regulators today increasingly expect bank directors to actively investigate operational risk management issues. KPMG’s Director of Fraud Risk Management, Ken Jones, echoed his point. Ken noted the challenge for bank executives and board members is “developing a comprehensive effort to (a) understand the US compliance and enforcement mandates — and how this criteria applies to them; (b) identify the types of fraud that impact the organization; (c) understand various control frameworks and the nature of controls; (d) integrate risk assessments, codes of conduct, and whistleblower mechanisms into corporate objectives; and (e) create a comprehensive anti-fraud program that manages and integrates prevention, detection, and response efforts.”

A One-Minute Video Recap

##

To comment on this piece, click on the green circle with the white plus (+) sign on the bottom right. If you are on twitter, I’m @aldominick. P.S. — check back tomorrow for a special guest post on AboutThatRatio.com.

From the the appeal of spreading into new geographies to the attractiveness of acquiring exceptional talent to drive new sources of revenue, the need and desire to grow exists at virtually every financial institution. For those pursuing another bank, a merger or acquisition (M&A) provides an avenue to drive earnings while improving operating leverage, efficiency and scale. I have written about M&A from a potential buyers point-of-view (e.g. Acquire or Be Acquired – Sunday Recap); today’s piece flips the script and highlights three issues that may precipitate a sale.

2006

2011

2013

Compliance Costs

Banks are facing some very significant challenges in the years ahead — and not just from consolidation. As KPMG shared in its An Industry At a Pivot Point, “the costs and time stresses created by the regulatory environment are not going away, and will continue to affect four areas for banks: strategy and business models, interactions with customers and client assets, data and reporting structures, and governance and risk capabilities.” Certainly, the sharply increased cost of regulatory compliance might lead some to seek a buyer; others will respond by trying to get bigger through acquisitions so they can spread the costs over a wider base.

Capital Concerns

Some banks will have to raise capital just to meet the Basel III requirements, while others will have to raise capital to do an acquisition or support their organic growth. The required levels are so much higher now that banks will have to manage their capital much more closely than they did before. (*If you’re looking for a central resource for the many ongoing regulatory changes that are reshaping bank capital and prudential requirements in the United States, take a look at Davis Polk’s excellent Capital and Prudential Standards Blog.)

Earnings Pressure

As the attractiveness of branch networks and deposit franchises dwindles, lack of top-line growth will lead to further industry consolidation. With little overall changes in our economy, in-market mergers between banks with significant overlap in branches and operations offer tremendous cost-saving opportunities when done skillfully.

##

To comment on this piece, click on the green circle with the white plus sign on the bottom right. Aloha Friday!