Dreaming of a trip to Phoenix, and the Acquire or Be Acquired Conference, next January doesn’t seem so odd this summer.

WORKING FROM HOME — For decades, business leaders began to book their travel to the Arizona desert — for Bank Director’s Acquire or Be Acquired Conference — in early August. As evidenced by the nearly 1,400 at the Arizona Biltmore earlier this year, the annual event has become a true stomping ground for CEOs, executives and board members. Many laud it as the place to be for those that take the creation of franchise value seriously. I’ve even heard it referred to as the unofficial kickoff of banking’s new year.

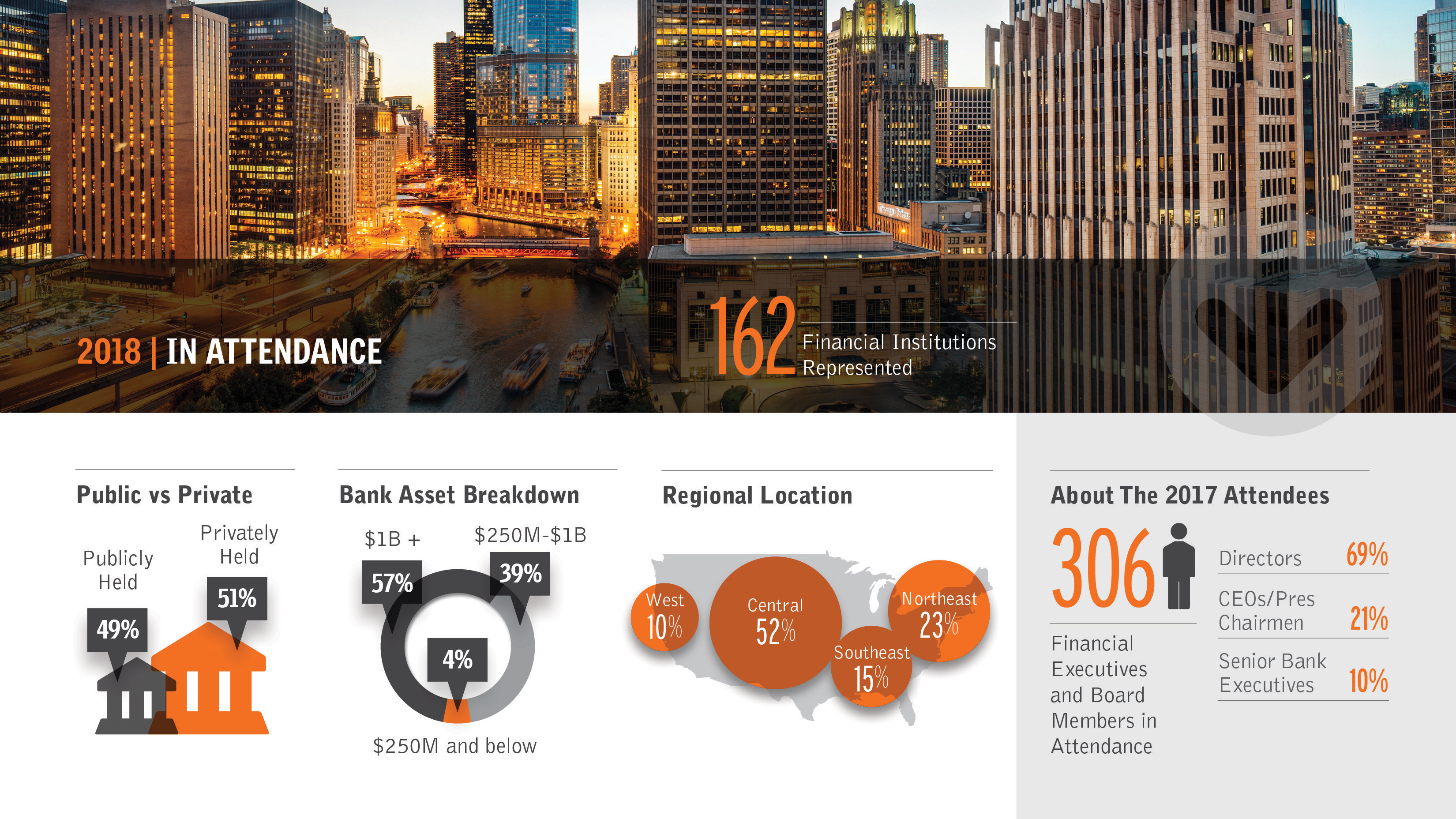

Just seven months ago, Acquire or Be Acquired once again brought together industry leaders from across the United States to explore merger opportunities, acquisition trends and financial growth ideas. With 418 banks represented, participants considered strategies specific to lending, deposit gathering and brand-building. They talked regulation, met with exceptional fintechs and networked with their peers under sunny skies.

Not one openly worried about a global pandemic.

Yet here we are, all of us dealing with fast-moving challenges and unimaginable risks.

So what can we do to help?

This is the question that proved the catalyst for our new AOBA Summer Series. Indeed, we created this free, on-demand, compilation of thought leadership pieces to provide pragmatic information and real-world insight.

With CEOs and leadership teams being called upon to make decisions they have never been trained for, we realized the type of information typically shared in January has immediate merit this summer. So instead of waiting until winter, this new Summer Series provides both color and context to the tough decisions — those with profound long-term consequences — that confront executives every day.

Ten videos comprise the AOBA Summer Series, with topics appropriate for the C-suite’s or board’s consideration. Streaming on BankDirector.com, we talk about how important scale has become in the banking industry… how one’s technology strategy cannot be delegated… how it certainly seems that there will be banks that come out of this in a bigger, stronger state. Here’s a screen-grab of what you’ll come across:

In one-on-one conversations like these, we acknowledge how net interest margins are compressing — which will drive up efficiency ratios — and credit costs are climbing. And we look at leadership, appreciating that many are leading in new, more positive and impactful ways. In addition, this new series provides:

A SNAPSHOT ON CURRENT CONDITIONS

At our January Acquire or Be Acquired Conference, Tom Michaud, President & CEO, Keefe, Bruyette & Woods, A Stifel Company, provided his outlook for the industry. Now, we ask him to update his perspectives on M&A activity and share his take on the potential implications of the pandemic.

HOW FINTECHS FIT

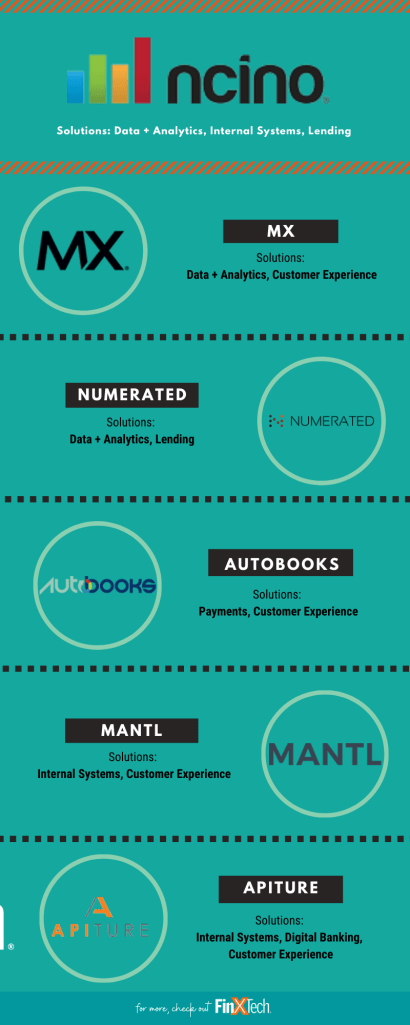

A growing number of technology companies have been founded to serve the banking industry. Not all of them have what it takes to satisfy bankers. During various sessions we learn how a variety of banks approach innovation — and the specific attributes a leadership team should look for in a new fintech relationship.

THE LEVERS OF VALUE CREATION

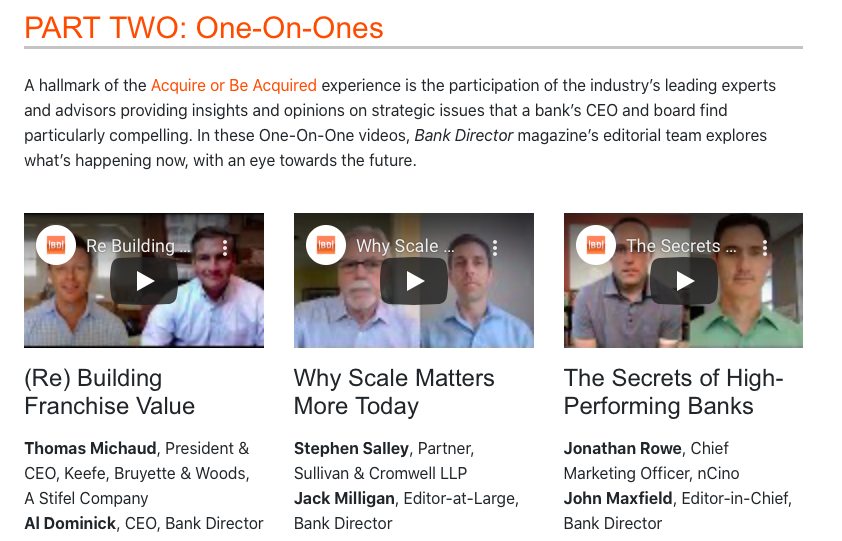

With nCino’s CMO, Jonathan Rowe, our Editor-in-Chief talks about the levers of creating value vis-a-vis the flywheel of banking. Together, they explain how certain technologies promote efficiency, which promotes prudence, thereby promoting profits, which can then be invested in technology, starting the cycle all over again.

Hearing from investment bankers, attorneys, accountants, fintechs, investors and — yes, other bankers — about the outlook for growth and change in the industry proves a hallmark for Acquire or Be Acquired, be it in-person or online.

As this new series makes clear, The future is being written in ways unimaginable just a few months ago. We invite you to watch how industry leaders are making sense of the current chaos for free on BankDirector.com.