Good things come in threes — like insightful/inspiring meetings in New York, Nashville and D.C. this week. By extension, keep an eye out for a Sunday, Monday and Tuesday post on About That Ratio. Yes, I’m heading to Chicago for Bank Director’s annual Chairman/CEO Peer Exchange at the Four Seasons (#chair14) and plan to share my thoughts and observations on issues like strategic planning, risk management and leveraging emerging technologies each day. Finally, I hope the three points I share today (e.g. a look at what the future holds for branches to a rise in public offerings) prove my original sentiment correct.

I’ve been surprised… by the # of conversations I’ve had about branch banking.

With many of the mega and super-regional banks focused on expense control, I find myself talking fairly regularly about how these institutions are taking a “fresh look” at reducing their branch networks. Typically, these conversations trend towards well-positioned regional and community banks — and how many now look to branch acquisitions as low risk and cost effectives ways to enter a new market or bolster an existing market. I expect these conversations to continue next week in Chicago — but thought to share today as it again came to the fore earlier this week in NYC. While there, I had a chance to catch up on PwC’s latest offerings and perspectives. Case-in-point, one of their current research pieces shows that, despite the emergence of new competitors and models:

“the traditional bank has a bright future – the fundamental concept of a trusted institution acting as a store of value, a source of finance and as a facilitator of transactions is not about to change. However, much of the landscape will change significantly, in response to the evolving forces of customer expectations, regulatory requirements, technology, demographics, new competitors, and shifting economics.”

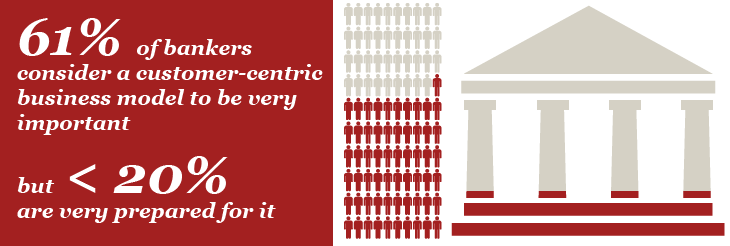

The two images above come from an information-rich micro-site (Retail Banking 2020) PwC shares. Personally, I found these statistics fascinating and foreshadow my second point about creative approaches to win new business.

I’ve been thinking about… fin’tech companies + their “solutions.”

Here, I want to give major props to our friends at the William Mills Agency in Atlanta. Their annual “Bankers as Buyers” report shares ideas, concepts and research about financial technology from 30 of the top influencers in the country and those forces driving change today. This year’s report lays out trends for the coming year, including:

- Branch Network Transformation;

- Mobile 3.0;

- Big Data Drives Marketing & Fights Fraud;

- Payments Technology Stampede;

- Banks Focus on Underbanked and Wealthy; and

- Compliance Strategies.

Take a look at their work and download the free report if you’re interested.

I’ve been talking about… the number of banks going public.

Is 2014 the year of the bank IPO? According to Tom Michaud, the president and CEO of Stifel Financial’s KBW, it just might be. I had a chance to get together with Tom earlier this week and he got me thinking about how many are going to pursue a public market to raise capital versus doing so privately. He shared the story of Talmer Bancorp (TLMR), which went public on Valentine’s Day. When it did, it marked the biggest bank IPO in three years (yes, KBW’s Banking & Capital Markets teams completed the $232 million Initial Public Offering, acting as joint bookrunner). As he shared their story with me, it became clear that as more banks go public, we will see more buyers entering into the M&A market — since most bank deals are being done with stock these days. It strikes me that going public presents an alternative for private banks… rather than sell now, they might find a more receptive market should their story be a good one.

Aloha Friday!