Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

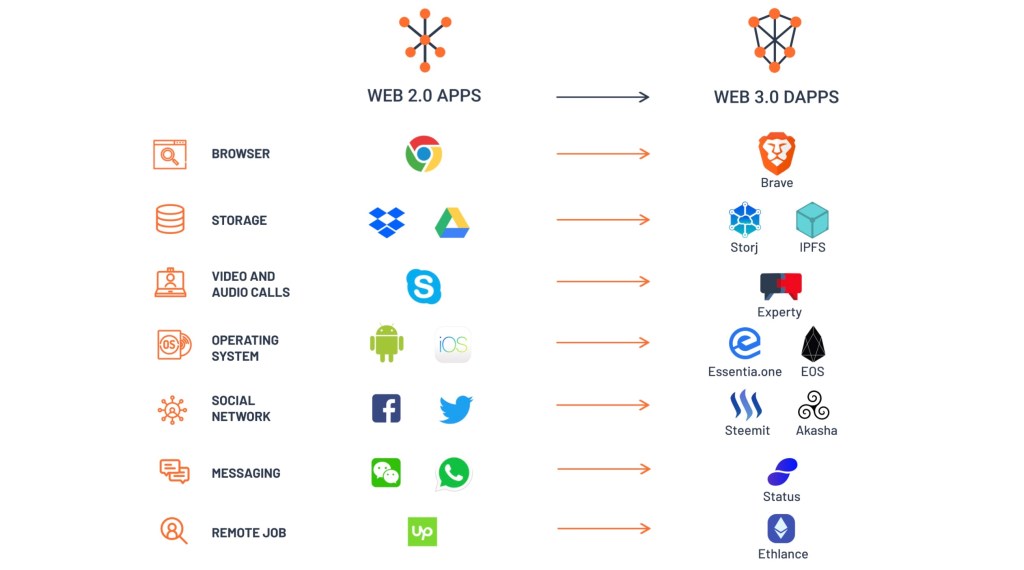

If I’d asked 100 different people at this week’s Acquire or Be Acquired to define DeFi, I’d bet $10,000 worth of ETH I’d get 100 different responses.

As I shared in yesterday morning’s remarks, decentralized finance is a complex area, with interest and usage growing exponentially over the past two years. Many aspects of financial services will be reinvented in a decentralized way — with numerous vendors working on new concepts. Given the current state of bank technology (coupled with a complex regulatory environment), financial markets are riddled with inefficiencies that new companies want to exploit.

Ours is a huge market being transformed by DeFi. But by no means the only industry being impacted. So as we wrap up our time in the Arizona desert, let me re-share one of my slides that shows changes taking place today.

Given the various investments taking place, and developments being announced, I encourage those 1,403 who joined us here to:

— Learn about smart contracts — and how these potentially replace banks and third parties in executing transactions.

— Tackle questions like “what are the benefits of incorporating blockchain technology into my services — and what are the inherent risks?”

— Focus on this year’s “wallet wars;” whereby wallet providers like Kraken, Crypto.com, MetaMask, etc. up their customer experiences to compete for clients.

This year’s event made good on my early prediction that diversification, differentiation and decentralization would be major themes. To the third one, we are just scratching the surface in terms of what’s now — and what’s next.

Earlier this week, I welcomed officers and directors from across the United States to Nashville, TN. From a stage (and not a Zoom), I asked them:

What are your options as we head into the Fall? No, not your personal ability to buy or sell an asset or security. Rather, the options you, as a leaders of your bank, see for the institution you are a part of today?

Strategically speaking, this is a fundamental issue for those in a leadership position to address.

Sure, there are topics that will dominate boardroom discussions — such as diversifying earnings streams and differentiating the bank’s reputation relative to others.

But let me ask you: who are your competitors? By extension, who are the peer groups that you should be basing your performance against? Once answering these, what options do you know are available, right now, that can put space between your bank and their business? Further, what options do you need to create in order to stay both relevant, and competitive in the months ahead?

Creating “optionality” is a concept that continues to rattle around in my mind. Indeed, it ties into the concept of franchise value and is one that members of a bank’s board need to prioritize. It opens conversations around delivery methods and channels, business relationships and partnerships — and yes, growth opportunities (be it organic or through acquisition).

As we talked about in Nashville, banks are under enormous pressure to prepare for an unknown future. Ahead of this year’s exclusive in-person event, I came up with three basic questions I find timely and relevant. Take a read and let me know if you agree.

Quickly:

WASHINGTON, DC — This past week, I had the distinct pleasure of visiting San Antonio, Texas. As I flew home on Thursday, I found myself reflecting on how purpose-driven companies (like the one I visited) focus on what their customers truly care about. By extension, I spent time reflecting on how a board might best support and encourage this mindset.

As I wrote for a piece that posted on BankDirector.com yesterday morning, one of my favorite proverbs when talking about the value of high-performing teams is to go fast, go alone; to go far, go together. Now, as my team prepares to head out to Chicago to welcome some 200 people to the Four Seasons Chicago for our annual Bank Board Training Forum, this mindset once again came front and center.

Given the financial industry’s rapid pace of change, one would be forgiven to think the best course of action would be to go fast at certain challenges. However, at the board level, navigating an industry marked by both consolidation and emerging threats demands coordinated, strategic planning.

Since I re-joined our company in September of 2010, I’ve noticed five key elements characterize many boards at high-performing banks. Some are specific to the individual director; others, to the team as a whole.

#1: The Board Sees Tomorrow’s Challenges as Today’s Opportunities

Despite offering similar products and services, a small number of banks consistently outperform others in the industry. One reason: their boards realize we’re in a period of significant change, where the basic premise of “what is a bank” is under considerable scrutiny. Rather than cower, they’ve set a clear vision for what they want to be and hold their team accountable to concepts such as efficiency, discipline and the smart allocation of capital.

#2: Each Board Member Embraces a Learner’s Mindset

Great leaders aren’t afraid to get up from their desks and explore the unknown. Brian Moynihan, the chairman and CEO of Bank of America, recently told our Executive Editor that “reading is a bit of a shorthand for a broader type of curiosity. The reason I attend conferences is to listen to other people, to pick up what they’re talking and thinking about… it’s about being willing to listen to people, think about what they say. It’s about being curious and trying to learn… The minute you quit being educated formally your brain power starts to shrink unless you educate yourself informally.”

(*Spoiler alert: you can read more from Bank Director’s exclusive conversation with Moynihan in the upcoming 4th quarter issue of Bank Director magazine.)

#3: The Board Prizes Efficiency

In simplest terms, an efficiently run bank earns more money. This allows it to write better loans, to suffer less during downturns in a credit cycle, to position it to buy less-prudent peers at a discount all while gaining economies of scale.

#4: Each Board Member Stays Disciplined

While discipline applies to many issues, those with a laser focus on building franchise value truly understand what their bank is worth now — and might be in the future. Each independent director prizes a culture of prudence, one that applies to everything from underwriting loans to third-party relationships.

#5: The Board Adheres to a People-Products-Performance Approach

Smart boards don’t pay lip service to this mindset. Collectively, they understand their institution needs to (a) have the right people, (b) strategically set expectations around core concepts of how the bank makes money, approaches credit, structures loans, attracts deposits and prices its products in order to (c) perform on an appropriate and repeatable level.

Looking ahead, I feel a sixth pillar could emerge for leading institutions; namely, diversity of talent. Now, I’m not talking diversity for the sake of diversity. I’m looking at getting the best people with different backgrounds, experiences and talents into the bank’s leadership ranks. Unfortunately, while many talk the talk on diversity, far fewer walk the walk. For instance, a recent New York Times piece that revealed female executives generally still lack the same opportunities to move up the ranks and there are still simply fewer women in the upper management pipeline at most companies.

At Bank Director, we believe ambitious bank boards see the call for greater diversity as a true opportunity to create a competitive advantage. This aligns with Bank Director’s 2018 Compensation Survey, where 87 percent of bank CEOs, executives and directors surveyed believe a diverse board has a positive impact on the performance of the bank. Yet, just 5 percent of CEOs above $1 billion in assets are female, 77 percent don’t have a single diverse member on their board and only 20 percent have a woman on the board.

So as we prepare to explore the strong board, strong bank concept in Chicago, I’m reminded of another adage, this one from Henry Ford. If all you ever do is all you’ve ever done, then all you’ll ever get is all you’ve ever got…

##

If you’re curious about what we’re talking about in Chicago, I encourage you to follow the conversation on social media, where we’re using #BDTrain18 to tag shared ideas on LinkedIn and Twitter.

Quickly:

PHOENIX — I’ve spent the past few days with bank leaders, technology executives, investors and analysts interested to explore emerging trends, opportunities and challenges facing many as they look to grow and scale their businesses. So as I prepare to head home to DC after some wonderfully exciting days at Bank Director’s annual FinXTech Summit, a few highlights from my time in the desert.

For me, one of the signature pieces of this year’s program occurred on Thursday evening. Under the stars, we recognized ten partnerships, each of which exemplified how banks and financial technology companies work together to better serve existing customers, attract new ones, improve efficiencies, bolster security and promote innovation. The finalists for this year’s Best of FinXTech Awards can be seen in this video.

We introduced these awards in 2016 to identify and recognize those partnerships that exemplify how collaborative efforts can lead to innovative solutions and growth in the banking industry. This year, we focused on three areas of business creativity:

The winners? Radius Bank and Alloy for Startup Innovation, CBW Bank and Yantra Financial Technology for Innovative Solution of the Year and Citizens Financial Group and Fundation for Best of FinXTech Partnership. To learn more about each, check out this cover story on BankDirector.com

https://twitter.com/ValidisGlobal/status/994635200331177984

Well played with the ZZ Top reference — now we just needs to grow out that beard and drop a pair of RayBans into the shot.

During our time in the desert, we shared a number of videos on BankDirector.com. The page with all videos can be found on FinXTech Annual Summit: Focusing on What’s Possible. To get a sense of what these short videos look like, here is an example:

Thanks to all those who joined us at the Phoenician. For more ideas and insight from this year’s event, I invite you to take a look at what we’ve shared on BankDirector.com (*no registration required).

Quickly:

PHOENIX — Many financial institutions face a creativity crisis. Legacy systems and monolithic structures stifle real change at many traditional banks — while newer technology leaders move quickly to pick up the slack. During the first day of our annual FinXTech Summit at the Phoenician, I picked up on a few practical ideas to break down a few of the most common barriers to innovation inside financial institutions.

As our managing editor, Jake Lowary, wrote for BankDirector.com this morning, “the cultural and philosophical divides between banks and fintech companies is still very apparent, but the two groups have generally come to agree that it’s far more lucrative to establish positive relationships that benefit each, as well as their customers, than face off on opposite ends of the business landscape.”

So with this in mind, I invite you to follow the conference conversations via our social channels, where our team continues to shares ideas and information from Day 2 of this event using @BankDirector and @Fin_X_Tech on Twitter. In addition, you can search & follow #FinXTech18 to see what’s being shared with (and by) our attendees.

Quickly:

PHOENIX — Tomorrow morning, we kick off our annual FinXTech Summit. As I wrote yesterday, this annual event serves as our “in-person” bridge between banks and qualified technology companies. Personally, I am so impressed to witness numerous financial institutions transforming how they offer banking products and services to businesses and individuals. As such, I find myself eager to engage in tomorrow’s conversations around:

Joining us at the Phoenician are senior executives from high-performance banks like Capital One, Customers Bank, Dime Community Bancshares, First Interstate Bank, IBERIABANK, Mechanics Bank, Mutual of Omaha Bank, PacWest, Pinnacle Financial, Seacoast National Bank, Silicon Valley Bank, South State Bank, TCF National Bank, Umpqua, Union Bank & Trust, USAA and US Bancorp. Long-time tech players like Microsoft share their opinions alongside strong upstarts like AutoBooks during this two-day program. So before I welcome nearly 200 men and women to this year’s conference, allow me to share a few of my preliminary thoughts going into the event:

For those with us here in Arizona, you’ll find nearly every presentation explores what makes for a strong, digitally-solid bank. So to see what’s trending, I invite you to follow the conference conversations via our social channels. For instance, I am @AlDominick on Twitter — and our team shares ideas and information through @BankDirector plus our @Fin_X_Tech platform. Finally, search & follow #FinXTech18 to see what’s being shared with (and by) our attendees.

Quickly:

PHOENIX — When I last stepped foot in Arizona, it was to host Bank Director’s annual Acquire or Be Acquired Conference. The January event attracts a hugely influential audience focused on mergers, acquisitions and growth strategies & tactics. While there, we noticed quite a few presentations explored how and where financial institutions might invest in, or better integrate, digital opportunities. So, as a complement to Acquire or Be Acquired, I’m back in the desert to dive deeper into myriad ideas for banks to improve profitability and efficiency with the help of technology firms.

As we prepare to host our FinXTech Annual Summit at the Phoenician, take note: smart banks are investing and/or partnering with technology companies because they realize it’s cheaper and faster than building something themselves. Further, the largest banks in the U.S. are rapidly evolving with advances in artificial intelligence across chatbots, robo-advisors, claims, underwriting, IoT and soon blockchain — all of which add another layer of potential to further shake-up traditional business models. In fact, there was a palatable sense among bankers at AOBA about the evolution in financial technology.

Nonetheless, many banks, especially those between $500M and $30Bn in assets, are on the outside looking in — and this is where FinXTech’s Summit story begins.

From exploring data to leveraging cognitive computing to gaining efficiencies in backroom processes, this year’s event surfaces a number of potent ideas. For instance, we shine a light on how bank leadership can truly unleash the potential of a technology partner. Further, we pull current quotes and issues like these to discuss and debate:

One thing I love about customers is that they are divinely discontent. Their expectations are never static — they go up. It’s human nature. We didn’t ascend from our hunter-gatherer days by being satisfied. People have a voracious appetite for a better way, and yesterday’s ‘wow’ quickly becomes today’s ‘ordinary’

— Jeff Bezos, Founder and Chief Executive Officer

Likewise, we share our takes on key acquisitions — like JP Morgan’s acquisition of WePay — while identifying how institutions leverage newer technologies to improve efficiency ratios and in some cases, boost franchise valuations.

In a sense, FinXTech’s Summit serves as our “in-person” bridge between banks and qualified technology companies. For those joining us, we’ll touch on various products and services for security, data & analytics, infrastructure, lending, mobile banking, payments and regtech while convening an exceptionally senior audience of 200+. Throughout the event, I’ll share my thoughts via Twitter, where I’m @AlDominick and using #FinXTech18. Finally, I’ll author a daily update on this site with my observations from the conference.

Quickly:

WASHINGTON, DC — I’m hard pressed to find anyone willing to contest the notion that technology continues to disrupt traditional banking models. Now, I realize the “D” word jumped the shark years ago. Personally, I try my best to keep my distance from employing the adjective to describe what’s taking place in the financial world vis-a-vis technology. However, banks of all sizes continue to reassess, and re-imagine, how financial services might be structured, offered and embraced given the proliferation of new digital offerings and strategies.

As I reflect on the first quarter of 2018, it strikes me that we’re living in an industry marked by both consolidation and displacement. Yes, many bank executives have fully embraced the idea that technology — and technological innovation — is a key strategic imperative. However, few banks have a clear strategy to acquire the necessary talent to fully leverage new technologies. On the flip side, I get the sense that a number of once-prominent FinTech companies are struggling to scale and gain customer adoption at a level needed to stay in business. Nonetheless, the divide between both parties remains problematic given the potential to help both sides grow and remain relevant.

While banks explore new ways to generate top-line growth and bottom-line profits through partnerships, collaboration and technology investments, I have some concerns. For instance, the digital expectations of consumers and small & mid-sized businesses may become cost-prohibitive for banks under $1Bn in assets. So allow me to share what’s on my mind given recent conversations, presentations and observations about the intersection of fin and tech.

Significant technological changes continue to impact the financial community. In the weeks to come, I’ll relay what I learn about these five issues in subsequent posts. If you’re interested, I tweet @AlDominick and encourage you to check out @BankDirector and @FinXTech for more.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech

WASHINGTON, DC — It is with tremendous pride that I share the results of Bank Director’s year-long study on America’s 10 largest banks. As my colleague, Bill King, wrote to open our inaugural Ranking Banking, we felt that a truly comprehensive analysis of the largest banks was missing, one that includes not just profitability or customer satisfaction ratings, but also compiles numerous measures of strength and financial health — a project to rank each of the largest banks for each major line of business based on qualities that all big banks need.

For instance, we decided to rank banks for branch networks, mobile banking, innovation and wealth management. We analyzed corporate banking and small business lending. We interviewed experts in the field and did secret shopper visits to the biggest banks to find out what the customer experience was like. Unlike other rankings, we even included complaints lodged with the Consumer Financial Protection Bureau as one of many customer satisfaction metrics that we analyzed. In other words, there is little about the biggest banks in the nation that we left out.

So who came out on top?

JPMorgan Chase & Co. topped Bank Director’s 2018 Ranking Banking study.

In fact, Chase won five of the ten individual categories and ranked near the top in three more, and was judged by Bank Director to be the most worthy claimant of the title Best of the Biggest Banks. The individual category winners are:

Best Branch Network: Wells Fargo & Co.

Despite its well-publicized unauthorized account opening scandal, Wells Fargo topped the branch category by showing the best balance of deposit growth and efficiency, and scored well on customer experience reports from Bank Director’s on-site visits.

In ranking the boards of directors of the big banks, Bank Director analyzed board composition by factors such as critical skill sets, diversity, median compensation relative to profitability and independence. Citigroup’s board best balanced all components.

Best Brand: JPMorgan Chase & Co.

Chase and runner-up Capital One Financial Corp. stood out for their media spend as a percentage of revenue, and both exhibited strong customer perception metrics.

Best Mobile Strategy: JPMorgan Chase & Co.

Chase has been successful in driving new and existing customers to its mobile products, leading to an impressive digital footprint, measured through mobile app downloads. The bank’s app also scored well with consumers.

Best Core Deposit Growth Strategy: BB&T Corp.

BB&T had a low cost of funds compared to the other ranked banks, and its acquisitions played a strong role in its core deposit growth, which far surpassed the other banks in the ranking.

Most Innovative: JPMorgan Chase & Co.

Chase most successfully balanced actual results with sizeable investments in technological innovation. These initiatives include an in-residence program and a financial commitment to the CFSI Financial Solutions Lab. Chase has also been an active investor in fintech companies.

Chase barely edged out fast-growing Capital One to take the credit card category, outpacing most of its competitors in terms of credit card loan volume and the breadth of its product offering. Chase also scored well with outside brand and market perception studies.

Best Small Business Program: Wells Fargo & Co.

Wells Fargo has long been recognized as a national leader in banking to small businesses, largely because of its extensive branch structure, and showed strong loan growth, which is difficult to manage from a large base. Wells Fargo is also the nation’s most active SBA lender and had the highest volume of small business loans.

Best Bank for Big Business: JPMorgan Chase & Co.

Big banks serve big businesses well, and finding qualitative differences among the biggest players in this category—Chase, Bank of America and Citigroup—is difficult. But Chase takes the category due to its high level of deposit share, loan volume and market penetration.

Best Wealth Management Program: Bank of America Corp.

With Merrill Lynch fueling its wealth management division, Bank of America topped the category by scoring highly in a variety of metrics, including number of advisors (more than 18,000 at last count) and net revenue for wealth and asset management, as well as earning high marks for market perception and from Bank Director’s panel of experts.

FWIW…

The 10 largest U.S. retail banks play an enormously important role in the nation’s economy and the lives of everyday Americans. For example, at the end of 2016, the top 10 banks accounted for over 53 percent of total industry assets, and 57 percent of total domestic deposits, according to the Federal Deposit Insurance Corp. The top four credit card issuers in 2016—JPMorgan Chase & Co., Bank of America Corp., Citigroup and Capital One Financial Corp.—put more than 303 million pieces of plastic in the hands of eager U.S. consumers, according to The Nilson Report.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech

ATLANTA — Complex regulations, technological innovations and a highly competitive environment that leaves little room for error have placed unprecedented demands on the time and talents of bank boards. Still, no one I’m with today seems interested in pity or sympathy. To wit, I’m in Atlanta, at the Ritz-Carlton Buckhead, as we host Bank Director’s annual Bank Board Training Forum. With us are 200+ men and women committed to strengthening their bank’s performance by enhancing the skills and abilities of their boards.

I’m buoyed by their collective optimism, especially having surfaced myriad governance issues, compliance challenges, audit responsibilities, risk concerns and areas of potential liability. What follows are five takeaways from presentations made today that are growth, risk or team-oriented.

Tomorrow morning, I share some new ideas for approaching technology in terms of growth and efficiency given the digital distribution of financial goods and services. As I noted from the stage, we’re seeing some banks, rather than hire from the ground up, take a plug-and-play approach for partnering (or acquiring) FinTech companies. While I certainly intend to talk about the culture and team aspects of technology tomorrow, my focus goes to how and where machine learning, RegTech, payments, white labeling opportunities and core providers allow financial institutions to present a cutting-edge looks and feels to its customers under the bank’s brand. (*If you’re interested, click here.)

Quickly:

“USAA was the first major financial institution to allow customers to deposit physical checks by taking a picture of them on their smartphones, rolling out the service in August 2009. It wasn’t until months later that Bank of America Corp., the nation’s second biggest bank by assets, said it would test the same functionality, by which point upward of 40,000 USAA members had already used the software to deposit more than 100,000 checks. And it wasn’t until the following year that JPMorgan Chase & Co., the nation’s biggest bank by assets, followed suit.

This was neither the first nor the last time that USAA, a niche player in the financial services industry serving current and former members of the military and their families, had beaten larger rivals to the punch in introducing a big, transformative idea. In 2015, the $78 billion asset company became the first major U.S. financial institution to roll out facial and voice recognition technology that allows members to log in to its mobile app without entering a password.

What is it about USAA that explains how it’s regularly at the forefront of big ideas? Is it serendipity, or is there something more at play? And if it’s the latter, are there aspects of USAA’s approach that can be replicated by other banks that want to accelerate their own internal innovation engines?

One explanation for USAA’s success is that the company has always had to think creatively about distribution because of its dispersed member base. With members stationed at military installations around the world, some in active combat zones, simply building more branches has never been a viable distribution strategy. It has a single bank branch at its headquarters in San Antonio, and it wasn’t until 2009 that it began opening a small collection of financial centers near domestic military bases—there are 17 of these centers currently. This is why USAA so readily embraced mobile banking, which enables its members to access their accounts irrespective of location.

Yet, chalking up USAA’s accomplishments in the sphere of innovation to the idea that “necessity is the mother of all invention” doesn’t do the story justice. More than any other major company in the financial services space, USAA has made it a priority to harness each of its 30,000 employees in order to stay on the cutting edge. It began doing so in earnest in 2010 by launching a so-called ideas platform on the company’s intranet. Anyone from the CEO to frontline personnel to security guards can post and vote on ideas that have been entered on the platform. Between 10,000 and 11,000 ideas were submitted in each of the last two years. Ideas that get at least 1,000 favorable employee votes are escalated to USAA’s in-house innovation team overseen by Zack Gipson, USAA’s chief innovation officer. Last year, 1,206 employee ideas were implemented, while 189 of them have come to fruition thus far in 2017.

USAA also hosts events and challenges for employees that are designed to elicit ideas for new or improved products and services. There are 28 such activities planned this year, taking the form of multi-week coding and design challenges as well as single-day hackathons where teams are tasked with solving a specific problem, says Lea Sims, assistant vice president of employee and member innovation. At an event in 2015, USAA happened upon the idea for voice-guided remote deposit capture, which uses voice commands to guide visually impaired members through the process of depositing checks on a mobile device. The service went live in July of 2016.

On top of these specific initiatives, USAA uses incentives and a consistent messaging campaign to encourage employees to brainstorm and share innovative ideas. Rewards are handed out to winners of challenges, as well as to any employee behind an idea that gets 1,000 votes on the ideas platform—an additional reward is meted out if the idea is implemented, explains Sims. These rewards come in the form of company scrip, which can be redeemed for actual products. A total of 94 percent of USAA employees have participated one way or another in its various innovation channels, with three quarters of a million votes submitted on its internal ideas platform in 2016 alone. “We put a premium on innovation,” says Sims. “It starts in new employee orientation as soon as you walk in the door to be part of our culture.”

USAA has taken steps to crowdsource ideas from its 12 million members, or customers, as well. In February it introduced USAA Labs, where members can sign up to share innovative ideas and participate in pilot programs of experimental products. “The goal of our membership channel is, quite frankly, to replicate the success of our employee channel,” says Sims. Thus far, over 770 members have signed onto the program, which is still in its early stages but could become a major part of USAA’s innovation channel in the future.

Last but not least, sitting atop USAA’s employee and member-based innovation channels is a team of 150 employees who focus solely on bringing new ideas to life. This is its strategic innovation group, which executes on crowdsourced ideas but spends most of its time brainstorming and implementing large, disruptive concepts such as remote deposit capture and biometric logins. It’s this final component of USAA’s strategy that adheres most closely to the institutional structure articulated by Harvard professor Clayton Christensen, a leading expert on the process of innovation. In his seminal book, The Innovator’s Dilemma, Christensen makes the case that established firms should vest the responsibility to bring ideas to life in organizationally independent groups. This is especially important when it comes to disruptive ideas that threaten to cannibalize other products and services sold by the firm, not unlike the way that remote deposit capture reduces the need for physical branches.

In short, the reason USAA has consistently been at the forefront of innovation in the financial services industry has next to nothing to do with serendipity. It traces instead to the company’s strategy of engaging all of its stakeholders in the idea generation process, harnessing the creative power of 30,000 employees, 12 million members and a select team of internal innovators who focus on nothing but bringing new ideas to life. It’s this structural approach to innovation, and the focus on employee engagement in particular, that offers a valuable model for other banks to follow. Indeed, out of the many big ideas USAA has introduced over the years, its strategy of crowdsourcing innovation may very well be the biggest.”

*John J. Maxfield is a writer and frequent contributor to Bank Director. To read more of this month’s issue (for free), click here. In full disclosure, I’m a loyal USAA member — as is my entire family — tracing back to my father’s days at the Naval Academy. I can attest to the “awesomeness” of the bank’s various mobile offerings — like facial recognition, remote check deposit, the integration of Coinbase (that lets me see the balance of my bitcoin and ethereum balances alongside my checking and savings accounts), etc.