WASHINGTON, DC — Can community banks out-compete JP Morgan, BofA and Wells Fargo? This is the elephant in the room awaiting 853 bank executives and board members — representing 432 Banks — at our upcoming Acquire or Be Acquired Conference. The lights don’t officially come up on our 25th annual event at the JW Marriott Phoenix Desert Ridge until Sunday, January 27. So in advance, three big questions I anticipate fielding in the desert.

Does 2019 Become the Year of BigTech?

As noted by H2 Ventures and KPMG, Amazon is providing payment services and loans to merchants on its platform, while Facebook recently secured an electronic money licence in Ireland. Alibaba, Baidu and Tencent have become dominant operators in China’s $5.5 trillion payments industry. Add in Fiserv’s recent $22B acquisition of First Data and Plaid’s of Quovo and we might be seeing the start of a consolidation trend in the financial technology sector. Will such investments and tie-ups draw the attention of big technology companies to the financial services industry?

Has the window to sell your bank already closed?

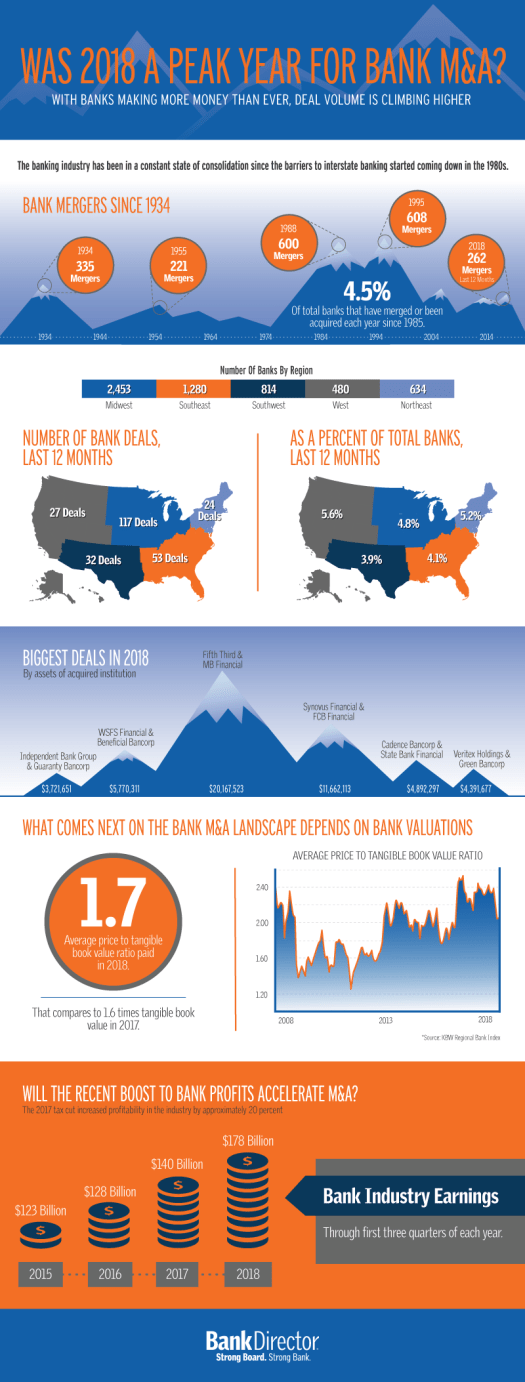

When I heard the rumor that BBVA might be buying UK-based Atom Bank — one of the proverbial European challenger banks — I started to look at acquisition trends here in the U.S. Case-in-point, we put together the following graphic in December for BankDirector.com

We know that some community banks have been holding out hopes of higher pricing multiples or for a strategic partner. These institutions might find the window of opportunity to stage an exit isn’t as open as it was just a few years ago. This doesn’t mean the window has shut — but I do think an honest assessment of what’s realistic, at the board level, is appropriate.

Wither the bond market?

A NY Times op-ed piece posits that the bond market reveals growing cracks in the financial system. Authored by Sheila Bair, the former chairwoman of the FDIC, and Gaurav Vasisht, director of financial regulation at the Volcker Alliance, it warns that “regulators are not doing enough to make sure that banks are prepared.” While the duo calls for thicker capital cushions for big banks and tighter leveraged loan underwriting standards, I wonder how executives joining us in Arizona feel about this potential threat to our economy?

_ _ _

As the premier bank M&A event for bank CEOs, senior management and board members, Bank Director’s 25th annual Acquire or Be Acquired Conference brings together key bank leaders from across the country to explore merger & acquisition strategies and financial growth opportunities. If you’re joining us in the desert, I’ll share a few FYIs later this week. If you’re unable to join us in Phoenix, AZ, I’ll be tweeting from @aldominick and using #AOBA19 when sharing on social platforms like LinkedIn.