Quickly:

- A bank’s CEO, Chairman and board of directors face a number of challenges in today’s ever competitive, highly regulated and rapidly evolving financial services industry.

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech

ATLANTA — Complex regulations, technological innovations and a highly competitive environment that leaves little room for error have placed unprecedented demands on the time and talents of bank boards. Still, no one I’m with today seems interested in pity or sympathy. To wit, I’m in Atlanta, at the Ritz-Carlton Buckhead, as we host Bank Director’s annual Bank Board Training Forum. With us are 200+ men and women committed to strengthening their bank’s performance by enhancing the skills and abilities of their boards.

I’m buoyed by their collective optimism, especially having surfaced myriad governance issues, compliance challenges, audit responsibilities, risk concerns and areas of potential liability. What follows are five takeaways from presentations made today that are growth, risk or team-oriented.

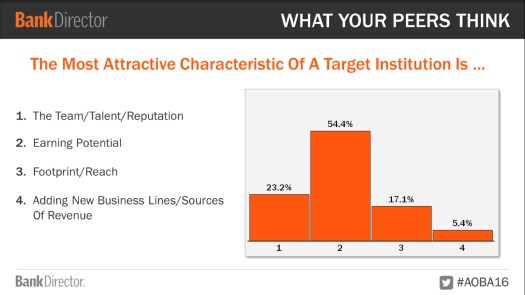

- When it comes to growing one’s bank, an acquisition of another institution certainly helps a buyer achieve operating scale efficiencies, which in turn increases its valuation.

- In addition to traditional M&A as a driver of growth, we are seeing more partnerships with (and outright acquisitions of) non-banks in order to enhance non-interest income and the expansion of net interest margins.

- Personally, I appreciated Jim McAlpin (a partner at the law firm of Bryan Cave) for elaborating on the phrase “Strong Governance Culture.” As he explained, the regulatory community takes this to mean a well developed system of internal oversight and a board culture focused on risk management.

- When it comes to risk, financial institutions face a quite a few. Indeed, Eve Rogers, a Partner at Crowe Horwath, touched on cybersecurity, economic factors, regulatory changes, shrinking margins and fee restrictions. As she made clear, proactively identifying, mitigating, and, in some cases, capitalizing on these risks provides a distinct advantage to the banks here with us.

- In terms of compensation, a good checklist for all banks includes (a) the bank’s compensation philosophy, (b) specific details for how to incorporate a performance plan against a strategic plan and (c) details around how one’s compensation peer group was formed — and when was it last updated.

Tomorrow morning, I share some new ideas for approaching technology in terms of growth and efficiency given the digital distribution of financial goods and services. As I noted from the stage, we’re seeing some banks, rather than hire from the ground up, take a plug-and-play approach for partnering (or acquiring) FinTech companies. While I certainly intend to talk about the culture and team aspects of technology tomorrow, my focus goes to how and where machine learning, RegTech, payments, white labeling opportunities and core providers allow financial institutions to present a cutting-edge looks and feels to its customers under the bank’s brand. (*If you’re interested, click here.)