Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Reduce and Redirect

authored by Al Dominick since 2010

Sharing a few bank-inspired observations from Asheville, North Carolina on a glorious Saturday evening.

Earlier this week, I welcomed officers and directors from across the United States to Nashville, TN. From a stage (and not a Zoom), I asked them:

What are your options as we head into the Fall? No, not your personal ability to buy or sell an asset or security. Rather, the options you, as a leaders of your bank, see for the institution you are a part of today?

Strategically speaking, this is a fundamental issue for those in a leadership position to address.

Sure, there are topics that will dominate boardroom discussions — such as diversifying earnings streams and differentiating the bank’s reputation relative to others.

But let me ask you: who are your competitors? By extension, who are the peer groups that you should be basing your performance against? Once answering these, what options do you know are available, right now, that can put space between your bank and their business? Further, what options do you need to create in order to stay both relevant, and competitive in the months ahead?

Creating “optionality” is a concept that continues to rattle around in my mind. Indeed, it ties into the concept of franchise value and is one that members of a bank’s board need to prioritize. It opens conversations around delivery methods and channels, business relationships and partnerships — and yes, growth opportunities (be it organic or through acquisition).

As we talked about in Nashville, banks are under enormous pressure to prepare for an unknown future. Ahead of this year’s exclusive in-person event, I came up with three basic questions I find timely and relevant. Take a read and let me know if you agree.

WASHINGTON, DC — Since March, I’ve talked with quite a few bank CEOs about their interest in modern and secure technologies. The underlying focus? Improving the experience provided to their customers.

In parallel to such one-on-one conversations, my colleague, Emily McCormick, surveyed 157 independent directors, chief executive officers, chief operating officers and senior technology executives of U.S. banks to understand how technology drives strategy at their institutions — and how those plans have changed due to the Covid-19 pandemic.

She conducted the survey in June and July — and we just released the results in Bank Director’s 2020 Technology Survey, sponsored by CDW. Here are a few key takeaways:

Focus on Experience

Eighty-one percent of respondents say improving the customer experience drives their bank’s technology strategy; 79% seek efficiencies.

Driving the Strategy Forward

For 64% of respondents, modernizing digital applications represents an important piece of their bank’s overall technology strategy. While banks look to third-party providers for the solutions they need, they’re also participating in industry groups (37%), designating a high-level executive to focus on innovation (37%) and engaging directors through a board-level technology committee (35%). A few are taking internal innovation even further by hiring developers (12%) and/or data scientists (9%), or building an innovation lab or team (15%).

Room for Improvement

Just 13% of respondents say their small business lending process is fully digital, and 55% say commercial customers can’t apply for a loan digitally. Retail lending shows more progress; three-quarters say their process is at least partially digital.

Spending Continues to Rise

Banks budgeted a median of $900,000 for technology spending in fiscal year 2020, up from $750,000 last year. But financial institutions spent above and beyond that to respond to Covid-19, with 64% reporting increased spending due to the pandemic.

Impact on Technology Roadmaps

More than half say their bank adjusted its technology roadmap in response to the current crisis. Of these respondents, 74% want to enhance online and mobile banking capabilities. Two-thirds plan to upgrade — or have upgraded — existing technology, and 55% prioritize adding new digital lending capabilities.

Remote Work Permanent for Some

Forty-two percent say their institution plans to permanently shift more of its employees to remote work arrangements following the Covid-19 crisis; another 23% haven’t made a decision.

Interestingly, this survey reveals that fewer banks rely on their core provider to drive their technology strategy. Forty-one percent indicated that their bank relies on its core to introduce innovative solutions, down from 60% in last year’s survey. Sixty percent look to non-core providers for new solutions. Interested to learn more? I invited you to view the full results of the survey on BankDirector.com.

WASHINGTON, DC — How should you position your bank for the future — or, for that matter, the present? This is one of the most perplexing questions challenging leadership teams right now. It is not a new consideration; indeed, the industry has been in a constant state of evolution for as long as anyone on our team can remember. Yet lately, it has taken on a new, possibly more existential sense of urgency.

Fortunately, there are examples of banks, of different sizes and a variety of business models, keeping pace with changing consumer expectations and commercial clients’ needs. The industry seems to be responding to the ongoing digital revolution in banking in three ways.

#1: Forge Your Own Digital Frontier

The biggest banks—those like JPMorgan Chase & Co., Bank of America Corp. and Wells Fargo & Co.—have the resources to forge their own paths on the digital frontier. These banks spend as much as $11 billion a year each on technology. Each hires thousands of programmers to conceptualize digital solutions for customers. And you know what? Their results are impressive.

As many as three-quarters of deposit transactions are completed digitally at these banks (take a minute and let that number sink in). A growing share of sales, account openings and money transfers take place over these banks’ digital channels as well. This allows these banks to winnow down their branch networks meaningfully while still gaining retail deposit market share.

*IMO, the next step in their evolution is to combine digital delivery channels with insights gleaned from data. It’s by marrying the two, I believe, that banks can gain a competitive advantage by improving the financial lives of their customers.

#2: Look Outside For Tailored Solutions

Just below the biggest banks are super-regional and regional banks. They too are fully embracing technology, although they tend to look outside their organizations for tailored solutions that will help them compete in this new era (rather than develop the solutions themselves).

These banks talk about integration as a competitive advantage. They argue that they can quickly and nimbly integrate digital solutions developed elsewhere—growing without a burdensome branch network while also benefiting from the latest technologies without bearing the risk and cost of developing many of those solutions themselves. It is a way, in other words, for them to have their cake and eat it too.

U.S. Bancorp and PNC Financial Services Group fall into this category. Both are reconfiguring their delivery channels, reallocating funds that would be spent on expanding and updating their branch networks to digital investments.

In theory, this makes it possible for these banks to expand into new geographic markets with far fewer branches. Indeed, U.S. Bancorp announced recently that it will use a combination of digital channels and new branches to establish a physical retail beachhead in Charlotte, North Carolina. PNC Financial is doing the same in Dallas, Texas, among other markets.

#3: Go Off-the-Shelf

Finally, smaller community banks are adopting off-the-shelf solutions offered by their core providers—Fidelity National Information Services (FIS), Fiserv and Jack Henry & Associates.

This approach can be both a blessing and a curse. It is a blessing because these solutions have enabled upwards of 90 percent of community banks to offer mobile banking applications—table stakes nowadays in the industry. It is a curse because it further concentrates the reliance of community banks on a triumvirate of service providers.

In the final analysis, however, it is important to appreciate that smaller banks based outside of major metropolitan areas still have a leg up when it comes to tried-and-true relationship banking. Their share of loans and deposits in their local markets could even grow if the major money-center banks continue fleeing smaller markets in favor of big cities.

Smaller regional and community banks dominate small business loans in their markets—a fact that was recently underscored by LendingClub Corp.’s decision to close its small business lending unit. These loans still require local expertise—the type of expertise that resides in their hometown banks. The same is true of agriculture loans.

Let’s Not Forget: Banks Are Still Banks

Trust is still the top factor cited by customers in the selection process. And loans must still be underwritten in a responsible way if a bank wants to survive the irregular, but not infrequent, cycles that define our economy. The net result is that some community banks are not only surviving in this new digital era, they are thriving.

But this isn’t a call to complacency—far from it.

Quickly:

PHOENIX — Many financial institutions face a creativity crisis. Legacy systems and monolithic structures stifle real change at many traditional banks — while newer technology leaders move quickly to pick up the slack. During the first day of our annual FinXTech Summit at the Phoenician, I picked up on a few practical ideas to break down a few of the most common barriers to innovation inside financial institutions.

As our managing editor, Jake Lowary, wrote for BankDirector.com this morning, “the cultural and philosophical divides between banks and fintech companies is still very apparent, but the two groups have generally come to agree that it’s far more lucrative to establish positive relationships that benefit each, as well as their customers, than face off on opposite ends of the business landscape.”

So with this in mind, I invite you to follow the conference conversations via our social channels, where our team continues to shares ideas and information from Day 2 of this event using @BankDirector and @Fin_X_Tech on Twitter. In addition, you can search & follow #FinXTech18 to see what’s being shared with (and by) our attendees.

Quickly:

WASHINGTON, DC — I’m hard pressed to find anyone willing to contest the notion that technology continues to disrupt traditional banking models. Now, I realize the “D” word jumped the shark years ago. Personally, I try my best to keep my distance from employing the adjective to describe what’s taking place in the financial world vis-a-vis technology. However, banks of all sizes continue to reassess, and re-imagine, how financial services might be structured, offered and embraced given the proliferation of new digital offerings and strategies.

As I reflect on the first quarter of 2018, it strikes me that we’re living in an industry marked by both consolidation and displacement. Yes, many bank executives have fully embraced the idea that technology — and technological innovation — is a key strategic imperative. However, few banks have a clear strategy to acquire the necessary talent to fully leverage new technologies. On the flip side, I get the sense that a number of once-prominent FinTech companies are struggling to scale and gain customer adoption at a level needed to stay in business. Nonetheless, the divide between both parties remains problematic given the potential to help both sides grow and remain relevant.

While banks explore new ways to generate top-line growth and bottom-line profits through partnerships, collaboration and technology investments, I have some concerns. For instance, the digital expectations of consumers and small & mid-sized businesses may become cost-prohibitive for banks under $1Bn in assets. So allow me to share what’s on my mind given recent conversations, presentations and observations about the intersection of fin and tech.

Significant technological changes continue to impact the financial community. In the weeks to come, I’ll relay what I learn about these five issues in subsequent posts. If you’re interested, I tweet @AlDominick and encourage you to check out @BankDirector and @FinXTech for more.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech.

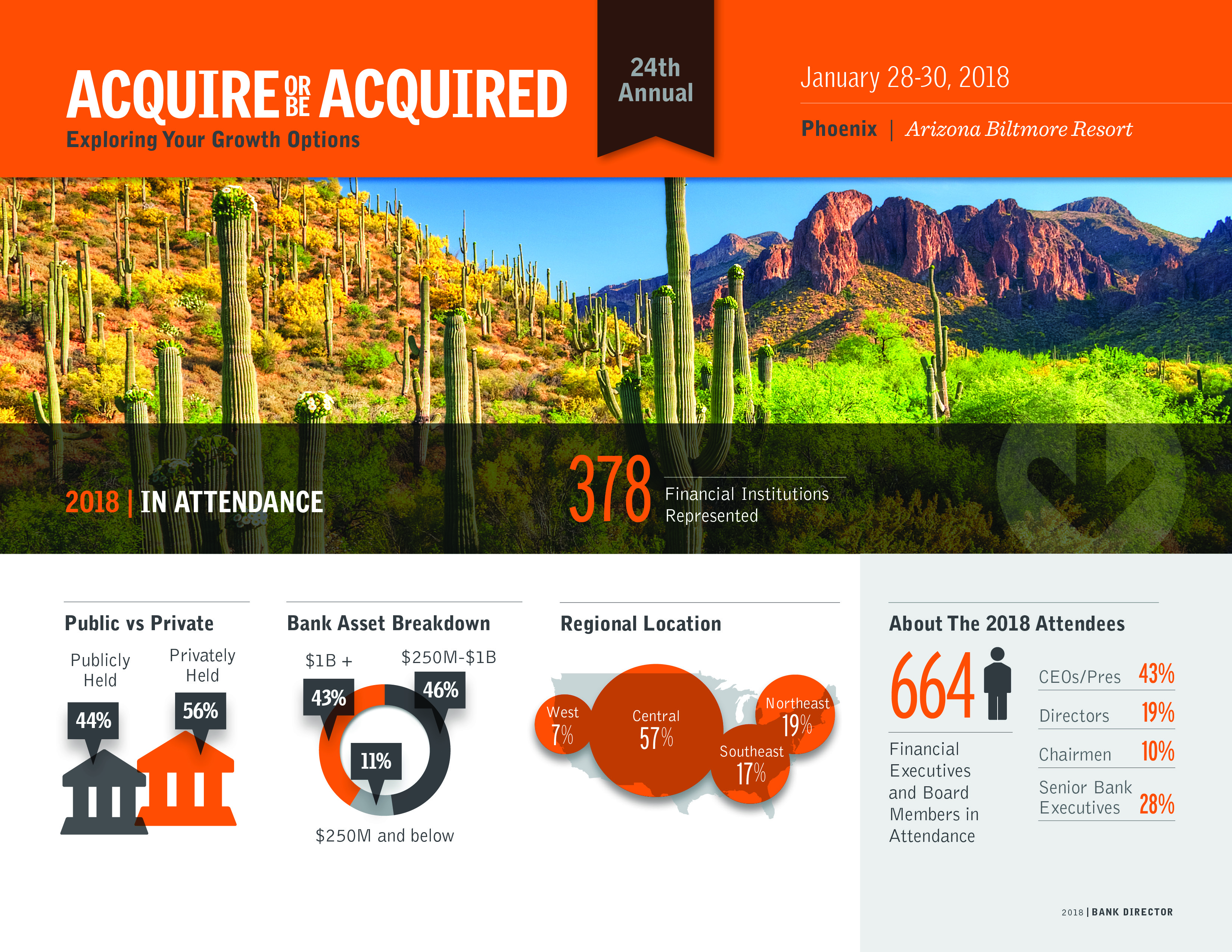

PHOENIX, AZ — As the sun comes up on the Arizona Biltmore, I have a huge smile on my face. Indeed, our team is READY to host the premier financial growth event for bank CEOs, senior management and members of the board: Bank Director’s 24th annual Acquire or Be Acquired Conference. This exclusive event brings together key leaders from across the financial industry to explore merger & acquisition strategies, financial growth opportunities and emerging areas of potential collaboration.

The festivities begin later today with a welcoming reception on the Biltmore’s main lawn for all 1,125 of our registered attendees. But before my team starts to welcome people, let me share what I am looking forward to over the next 72 hours:

For those of you interested in following the conference conversations via our social channels, I invite you to follow me on Twitter via @AlDominick, the host company, @BankDirector and our @Fin_X_Tech platform, and search & follow #AOBA18 to see what is being shared with (and by) our attendees.

Quickly:

By Al Dominick, CEO of DirectorCorps — parent co. to Bank Director & FinXTech

WASHINGTON, DC — J.P. Morgan’s CEO, Jamie Dimon, recently threw some big time shade at bitcoin. However, as the Wall Street Journal shared this morning, he’s “still enamored with the technology that underpins it and other virtual currencies.” For those wondering about where and why blockchain might revolutionize the business of banking, take a look at our just-released Q4 issue of Bank Director Magazine. We dedicated our cover story to “Understanding Blockchain,” and this post teases out some of the key concepts bank executives and board members might focus in on. Authored by John Engen, the full piece can be found, for free, here. As you’ll read, the article covers three major points:

If you’re on the board of a typical U.S. bank, odds are that you don’t know much about blockchain, or distributed ledgers, except that there’s a heavy buzz around the space—and a lot of big bets being made. As John Engen wrote, being a know-nothing might be fine for now, but going forward could be untenable.

At its most basic, blockchain is a digital-ledger technology that allows market participants, including banks, to transfer assets across the internet quickly and without a centralized third party.

Some describe it as the next, inevitable step in the evolution of the internet; a structure to help confront concerns about security, trust and complexity that have emerged from a technology that has opened the world to sharing information. To others, it looks more like business-process improvement software—a way to improve transparency, speed up transaction times and eliminate billions of dollars in expenses that markets pay to reconcile things like credit default swaps, corporate syndicated debt and other high-volume assets.

“Trying to guess how blockchain is going to affect us in the next 20 years is kind of like standing in 1995 and trying to imagine mobile-banking technology,” said Amber Baldet, New York-based JPMorgan Chase & Co.’s blockchain program leader, in an online interview. “I’m sure the ultimate applications are things we can’t even imagine right now.”

For now, the space certainly has the feel of the 1990s internet, with hundreds of startups and billions of investment dollars chasing distributed-ledger initiatives. Armonk, New York-based IBM Corp., a big blockchain supporter, estimates that 90 percent of “major” banks in the world—mostly those with trading, securities, payments, correspondent banking and trade finance operations—are experimenting with blockchain in some way.

Most large banks are involved in consortiums with names like Ripple, Hyperledger, R3 and Enterprise Ethereum Alliance. Smaller banks are taking more of a wait-and-see approach. For all the promise of speed and efficiency, blockchain’s real power lies in its transparency, which makes data both trackable and immutable. Ultimately, blockchain could usher in new business models, which require different ways of thinking.

##

For members of a bank’s board, we created this “Blockchain 101” video. In it, I touch on the potential application of blockchain in terms of digital identities, digital banking and cross-border payments. In addition, the ten minute video surfaces key concepts and business ideas that remain material to many today.

*This video is just one of the offerings found in our Bank Services program designed to help board members and senior executives develop strategies to help their bank grow, while demonstrating excellence in corporate governance that shareholders and customers deserve and today’s regulators demand.

Quickly:

“USAA was the first major financial institution to allow customers to deposit physical checks by taking a picture of them on their smartphones, rolling out the service in August 2009. It wasn’t until months later that Bank of America Corp., the nation’s second biggest bank by assets, said it would test the same functionality, by which point upward of 40,000 USAA members had already used the software to deposit more than 100,000 checks. And it wasn’t until the following year that JPMorgan Chase & Co., the nation’s biggest bank by assets, followed suit.

This was neither the first nor the last time that USAA, a niche player in the financial services industry serving current and former members of the military and their families, had beaten larger rivals to the punch in introducing a big, transformative idea. In 2015, the $78 billion asset company became the first major U.S. financial institution to roll out facial and voice recognition technology that allows members to log in to its mobile app without entering a password.

What is it about USAA that explains how it’s regularly at the forefront of big ideas? Is it serendipity, or is there something more at play? And if it’s the latter, are there aspects of USAA’s approach that can be replicated by other banks that want to accelerate their own internal innovation engines?

One explanation for USAA’s success is that the company has always had to think creatively about distribution because of its dispersed member base. With members stationed at military installations around the world, some in active combat zones, simply building more branches has never been a viable distribution strategy. It has a single bank branch at its headquarters in San Antonio, and it wasn’t until 2009 that it began opening a small collection of financial centers near domestic military bases—there are 17 of these centers currently. This is why USAA so readily embraced mobile banking, which enables its members to access their accounts irrespective of location.

Yet, chalking up USAA’s accomplishments in the sphere of innovation to the idea that “necessity is the mother of all invention” doesn’t do the story justice. More than any other major company in the financial services space, USAA has made it a priority to harness each of its 30,000 employees in order to stay on the cutting edge. It began doing so in earnest in 2010 by launching a so-called ideas platform on the company’s intranet. Anyone from the CEO to frontline personnel to security guards can post and vote on ideas that have been entered on the platform. Between 10,000 and 11,000 ideas were submitted in each of the last two years. Ideas that get at least 1,000 favorable employee votes are escalated to USAA’s in-house innovation team overseen by Zack Gipson, USAA’s chief innovation officer. Last year, 1,206 employee ideas were implemented, while 189 of them have come to fruition thus far in 2017.

USAA also hosts events and challenges for employees that are designed to elicit ideas for new or improved products and services. There are 28 such activities planned this year, taking the form of multi-week coding and design challenges as well as single-day hackathons where teams are tasked with solving a specific problem, says Lea Sims, assistant vice president of employee and member innovation. At an event in 2015, USAA happened upon the idea for voice-guided remote deposit capture, which uses voice commands to guide visually impaired members through the process of depositing checks on a mobile device. The service went live in July of 2016.

On top of these specific initiatives, USAA uses incentives and a consistent messaging campaign to encourage employees to brainstorm and share innovative ideas. Rewards are handed out to winners of challenges, as well as to any employee behind an idea that gets 1,000 votes on the ideas platform—an additional reward is meted out if the idea is implemented, explains Sims. These rewards come in the form of company scrip, which can be redeemed for actual products. A total of 94 percent of USAA employees have participated one way or another in its various innovation channels, with three quarters of a million votes submitted on its internal ideas platform in 2016 alone. “We put a premium on innovation,” says Sims. “It starts in new employee orientation as soon as you walk in the door to be part of our culture.”

USAA has taken steps to crowdsource ideas from its 12 million members, or customers, as well. In February it introduced USAA Labs, where members can sign up to share innovative ideas and participate in pilot programs of experimental products. “The goal of our membership channel is, quite frankly, to replicate the success of our employee channel,” says Sims. Thus far, over 770 members have signed onto the program, which is still in its early stages but could become a major part of USAA’s innovation channel in the future.

Last but not least, sitting atop USAA’s employee and member-based innovation channels is a team of 150 employees who focus solely on bringing new ideas to life. This is its strategic innovation group, which executes on crowdsourced ideas but spends most of its time brainstorming and implementing large, disruptive concepts such as remote deposit capture and biometric logins. It’s this final component of USAA’s strategy that adheres most closely to the institutional structure articulated by Harvard professor Clayton Christensen, a leading expert on the process of innovation. In his seminal book, The Innovator’s Dilemma, Christensen makes the case that established firms should vest the responsibility to bring ideas to life in organizationally independent groups. This is especially important when it comes to disruptive ideas that threaten to cannibalize other products and services sold by the firm, not unlike the way that remote deposit capture reduces the need for physical branches.

In short, the reason USAA has consistently been at the forefront of innovation in the financial services industry has next to nothing to do with serendipity. It traces instead to the company’s strategy of engaging all of its stakeholders in the idea generation process, harnessing the creative power of 30,000 employees, 12 million members and a select team of internal innovators who focus on nothing but bringing new ideas to life. It’s this structural approach to innovation, and the focus on employee engagement in particular, that offers a valuable model for other banks to follow. Indeed, out of the many big ideas USAA has introduced over the years, its strategy of crowdsourcing innovation may very well be the biggest.”

*John J. Maxfield is a writer and frequent contributor to Bank Director. To read more of this month’s issue (for free), click here. In full disclosure, I’m a loyal USAA member — as is my entire family — tracing back to my father’s days at the Naval Academy. I can attest to the “awesomeness” of the bank’s various mobile offerings — like facial recognition, remote check deposit, the integration of Coinbase (that lets me see the balance of my bitcoin and ethereum balances alongside my checking and savings accounts), etc.

By Al Dominick, CEO of DirectorCorps (parent co. to Bank Director & FinXTech) | @aldominick

Quickly:

_ _ _

If you have been to any of our conferences, you’ve probably heard me (and others) encourage participants to get up & out from their offices to see what’s happening with their customers, potential partners and competition. I do my best to practice what is preached — and have recent trips to San Francisco, New York City and Austin to prove it. As I re-read hand written notes, dog-eared white papers and highlighted sections of annual reports, I realize just how much time I’ve spent talking about technology-driven trends shaping the financial industry. To me, three of the bigger issues being discussed right now involve:

To these three trends, both our editor-in-chief, Jack Milligan, and I agree that most bankers understand the imperative to innovate around key aspects of their business, whether it’s payments, mobile in all its many permutations, lending, new account onboarding or data.

Personally, when it comes to knowing one’s customer (and potential customer), I find any good experience starts with great data. As Carl Ryden, the CEO and Co-Founder at PrecisionLender, made clear at their recent Bank of Purpose conference, “if you hold your data close to the vest and you don’t do anything with it, it’s not an asset. It’s a liability.”

So with that in mind, let me close by sharing a link to our newest issue of Bank Director magazine. This is our “Great Ideas” issue, one in which we highlight companies like USAA who crowdsource upwards of 10,000 ideas per year for products and new technology. At a time when banks of all sizes are starting to take advantage of platform-based services, this new digital issue is one that I am really proud to share.

By Al Dominick, CEO of DirectorCorps (parent co. to Bank Director & FinXTech) | @aldominick

Quickly

_ _ _

While I am bullish on the future of banking as a concept, I am admittedly concerned about what’s to come for many banks who struggle with cultural mindsets resistant to change. As I shared in an op-ed that kicked off last week’s FinTech Week NYC, the same dynamics that helped weather the last few years’ regulatory challenges and anemic economic growth may now prevent adoption of strategically important, but operationally risky, relationships with financial technology companies.

Most banks don’t have business models designed to adapt and respond to rapid change. So how should they think about innovation? I raised that question (and many others) at last Wednesday’s annual FinXTech Summit that we hosted at Nasdaq’s MarketSite. Those in attendance included banks both large and small, as well as numerous financial technology companies — all united around an interest in how technology continues to change the nature of banking.

More so than any regulatory cost or compliance burden, I sense that the organizational design and cultural expectations at many banks present a major obstacle to future growth through technology. While I am buoyed by the idea that smaller, nimble banks can compete with the largest institutions, that concept of agility is inherently foreign to most legacy players.

It doesn’t have to be.

Indeed, Richard Davis, the chairman and CEO of the fifth largest bank in the country, U.S. Bancorp, shared at our Acquire or Be Acquired Conference in Phoenix last January that banks can and should partner with fintech companies on opportunities outside of traditional banking while working together to create better products, better customer service and better recognition of customer needs.

The urgency to adapt and evolve should be evident by now. The very nature of financial services has undergone a major change in recent years, driven in part by digital transformation taking place outside banking. Most banks—big and small—boast legacy investments. They have people doing things on multi-year plans, where the DNA of the bank and culture does not empower change in truly meaningful ways. For some, it may prove far better to avoid major change and build a career on the status quo then to explore the what-if scenarios.

Here, I suggest paying attention to stories like those shared by our Editor-in-Chief Jack Milligan, who just wrote about PNC Financial Services Group in our current issue of Bank Director magazine. As his profile of Bill Demchak reveals, it is possible to be a conservative banker who wants to revolutionize how a company does business. But morphing from a low-risk bank during a time of profound change requires more than just executive courage. It takes enormous smarts to figure out how to move a large, complex organization that has always done everything one way, to one that evolves quickly.

Of course, it’s not just technological innovation where culture can be a roadblock. Indeed, culture is a long-standing impediment to a successful bank M&A deal, as any experienced banker knows. So, just as in M&A deals, I’d suggest setting a tone at the top for digital transformation. Here are three seemingly simple questions I suggest asking in an executive team meeting:

From here, it might be easy to create a strategic direction to improve efficiency and bolster growth in the years ahead. But be prepared for false starts, fruitless detours and yes, stretches of inactivity. As Fifth Third Bank CEO Greg Carmichael recently shared in an issue of Bank Director magazine, “Not every problem needs to be solved with technology… But when technology is a solution, what technology do you select? Is it cost efficient? How do you get it in as quickly as possible? You have to maintain it going forward, and hold management accountable for the business outcomes that result if the technology is deployed correctly.”

Be aware that technology companies move at a different speed, and it’s imperative that you are nimble enough to change, and change again, as marketplace demands may be different in the future. Let your team know that you are comfortable taking on certain kinds of risk and will handle them correctly. Some aspects of your business may be harmed by new technology, and you will have to make difficult trade-offs. Just as in M&A, I see this is an opportunity to engage with regulators. Seek out your primary regulator and share what you’re looking for and help regulators craft an appropriate standard for dealing with fintech companies.

Culture should not be mistaken for a destination. If you know that change is here, digital is the expectation and you’re not where you want to be, don’t ignore the cultural roadblocks. Address them.

“If past history was all that is needed to play the game of money, the richest people would be librarians.” – Warren Buffett

#AOBA17 pre-conference intel

By Al Dominick, CEO of Bank Director | @aldominick

This may be a phenomenal—or scary year—for banks. Banks have benefited from rising stock prices and rising interest rates, which are expected to boost low net interest margins. Indeed, the change in the U.S. presidency has resulted in a steepened yield curve, as investors predict improved economic growth. Currently, many anticipate regulatory relief for banks and the prospect of major corporate tax cuts. Such change could have a significant impact on banks; however, those running financial institutions also need to keep an eye on potential challenges ahead.

As we head to our 23rd Acquire or Be Acquired Conference in Phoenix, Arizona, with a record breaking 1,058 attendees Jan. 29-Jan. 31, I am expecting the mood to be good. Why wouldn’t it be? But what is on the horizon are also fundamental changes in technology that will change the landscape for banking. What will your competitors be doing that you won’t be? Our conference has always been a meeting ground for the banking industry’s key leaders to meet, engage with each other and learn what they need to do deals. It is still that. Indeed, most of the sessions and speakers will be talking about M&A and growth.

But this year, more than 100 executives from fintech companies that provide products and services to banks join us in the desert, on our invitation. We want to help banks start thinking about the challenges ahead and how they might solve them.

Here are some things to consider:

To this last point, I intend to spotlight three companies that are changing the way their industries operate to inspire conversations about both the risks and rewards of pursuing a path of change. Yes, it’s OK to think a little bit beyond the banking industry.

Spotify

Rather than buying a CD to get their favorite songs, music-lovers today favor curated playlists where people pick, click and choose whom they listen to and in what order. There is a natural parallel to how people might bank in the future. Just as analytics enable media companies to deliver individually tailored and curated content, so too is technology available to banks that might create a more personalized experience. Much like Spotify gives consumers their choice of music when and where they want it, so too are forward-looking banks developing plans to provide consumer-tailored information “on-demand.”

Airbnb

The popular home-rental site Airbnb is reportedly developing a new service for booking airline flights. Adding an entirely new tool and potential revenue stream could boost the company’s outlook. For banks, I believe Airbnb is the “uber-type” company they need to pay attention to, as their expansion into competitive and mature adjacent markets parallels what some fear Facebook and Amazon might offer in terms of financial services.

WeChat

One of China’s most popular apps, the company counts 768 million daily active users (for context, that’s 55 percent of China’s total population). Of those users, roughly 300 million have added payment information to the wallet. So, WeChat Pay’s dominance in the person-to-person payments space is a model others can emulate. PayPal already is attempting such dominance, which Bank Director magazine describes in our most recent issue.

Many of those attending our conference also have done amazing things in banking. I can’t name all of them, but I’d be remiss to not mention CEO Richard Davis of U.S. Bank, our keynote speaker. After a decade leading one of the most phenomenal and profitable banks in the country, he is stepping down in April. We all have something to learn from him, I’m sure. Let us think about the lessons the past has taught us, but keep an eye on the future. Let’s expect the unexpected.

*note – this piece first ran on BankDirector.com on January 26, 2017