WASHINGTON, DC — In 2017, Bank Director magazine featured a story titled “The API Effect.” It showed how banks could earn revenue by using application programming interfaces, or APIs. It considered the pros (and cons) of banks turning themselves into technology platforms. And it concluded with a prediction:

APIs will be so prevalent in five years that banks who are not leveraging them will be similar to banks that don’t offer a mobile banking application.

Less than three years later, the banking industry is on a fast track to proving that hypothesis.

Let’s start with the basics. An application program interface, or API, controls interactions between software and systems. As the American Banker recently shared, “APIs are the glue of the internet and allow digital businesses to interact seamlessly. Banks create a digital-first business model by offering services, such as treasury or loan origination, through APIs in an open-banking system.”

So to help bank executives better understand the promise and potential of APIs, our team developed a special FinXTech Intelligence Report. In it, we explore use cases with a focus on banking, and detail the forces driving adoption of the technology among financial institutions of all sizes.

Divided into five parts, we explore:

— Market trends driving the adoption of APIs;

— Actionable API use cases for growing revenue and creating efficiencies;

— An in-depth case study of TAB Bank, which reimagined its data infrastructure with APIs;

— Key considerations for leadership teams developing an API strategy; and

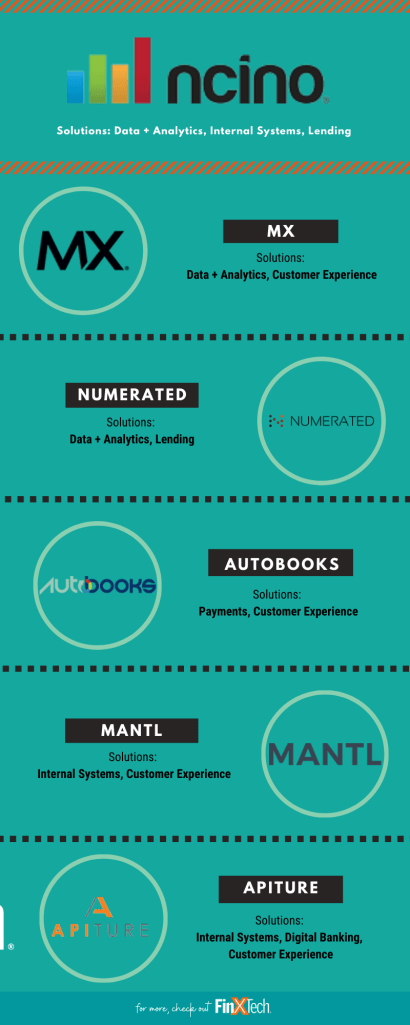

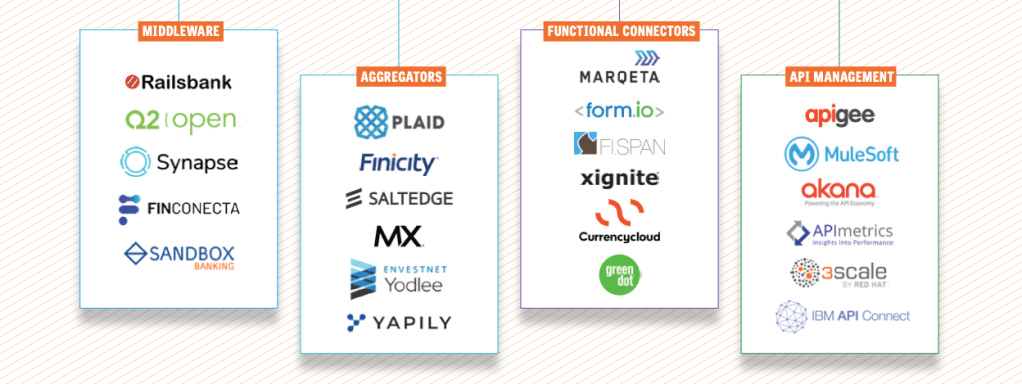

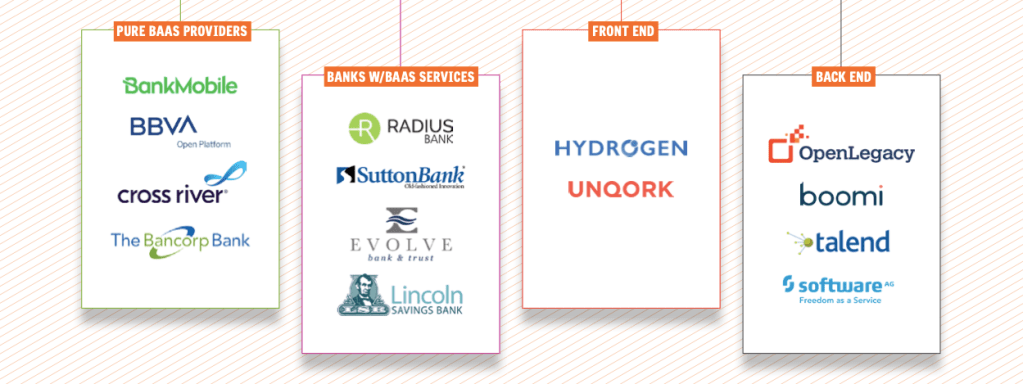

— A map of the API provider landscape, highlighting the leading companies enabling API transformation.

Kudos to the talented Amber Buker for spearheading this effort. As she makes clear, there are several ways for banks to implement APIs. Some will work with their cores (e.g. FIS, Fiserv and Jack Henry) to access the necessary connectivity. Ready-made APIs from fintech providers can quickly address the most common connectivity requirements.

For more complex use cases — like large banks running on old mainframes — the line from systems of record to end users could be longer, with several providers along the path. Regardless of where you are on your journey, understanding the landscape of API providers helps banks get a firmer grasp on the technology and start conceptualizing the scale and design of their potential API project.

To learn more about how banks use APIs, I invited you to download, for free, our FinXTech Intelligence Report, APIs: New Opportunities for Revenue and Efficiency.