Jim Collins once wrote “good is the enemy of great,” opining that the vast majority of companies “never become great, precisely because the vast majority become quite good – and that is their main problem.” I have heard many use the title of today’s piece to explain the unexpected; most recently, while talking with a friend about Jurgen Klinsmann’s decision to exclude Landon Donovan from his 23-man World Cup roster (hence today’s picture c/o USA Today). While I’ll steer clear of any soccer talk until the U.S. takes the field against Ghana in a few weeks, Collins’ statement sparked the three thoughts I share today. Indeed, being “just good” will not cut it in our highly competitive financial industry.

Let’s Be Real — Times Remain Tough

Let’s Be Real — Times Remain Tough

In yesterday’s Wall Street Journal, Robin Sidel and Andrew Johnson began their “Big Profit Engines for Banks Falter” with a simple truth: “it is becoming tougher and tougher being a U.S. bank. Squeezed by stricter regulations, a sputtering economy and anemic markets, financial institutions are finding profits hard to come by on both Main Street and Wall Street.” Now, the U.S. financial sector and many bank stocks have “staged a dramatic recovery from the depths of the financial crisis;” as the authors point out, “historically low-interest rates aren’t low enough to spur more mortgage business and are damping market volatility, eating into banks’ trading profits.” While I’ve written about the significant challenges facing most financial institutions – e.g. tepid loan growth, margin compression, higher capital requirements and expense pressure & higher regulatory costs — the article provides a somber reminder of today’s banking reality.

Still, for Banks Seeking Fresh Capital, the IPO Window is Open

Given how low-interest rates continue to eat into bank profits, its not surprising to hear how “opportunistic banks capable of growing loans through acquisition or market expansion” are attracting investor interest and going public. To wit, our friends at the Hovde Group note that seven banks have filed for initial public offerings (IPOs) already this year, putting 2014 on pace to become the most active year for bank IPOs in a decade. Based on the current market appetite for growth, “access to capital is becoming a larger consideration for management and boards, especially if it gives them a public currency with which to acquire and expand.” If you’re interested in the factors fueling this increase in IPO activity, their “Revival of the Bank IPO” is worth a read.

Mobile Capabilities Have Become Table Stakes

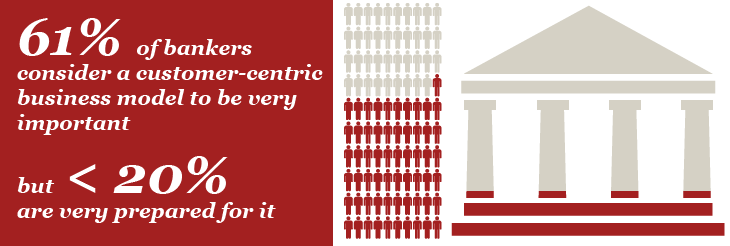

I’m on the record for really disliking the word “omnichannel.” So I smiled a big smile while reading through a new Deloitte Center for Financial Services report (Mobile Financial Services: Raising the Bar on Customer Engagement) that emphasizes the need for banks to focus more on a “post-channel” world rather than the omnichannel concept. As their report says, this vision is “where channel distinctions are less important and improving customer experience becomes the supreme goal, no matter where or how customer interactions occur, whether at a branch, an ATM, online, or via a mobile device.” As mobile is increasingly becoming the primary method of interaction with financial institutions, the information shared is both intuitive and impactful.

##

To comment on today’s column, please click on the green circle with the white plus sign on the bottom right. If you are on twitter, I’m @aldominick. Aloha Friday!