#AOBA17 conference intel (Friday)

By Al Dominick, CEO of Bank Director | @aldominick

Quickly

- The “bank of the future” is not about technology, it is all about customers.

- For many financial institutions, the time may be right to retire legacy systems for cloud-based platforms.

- Numerous financial technology companies are developing new strategies, practices and products that will dramatically influence the future of banking..

_ _ _

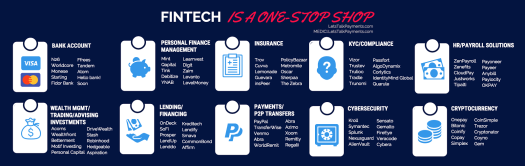

The intersection of technological innovation with strong depository franchises may lead to more efficient banking processes, reductions in fraud and a win/win/win for banks, financial technology firms (fintechs) and consumers. Globally, nearly $23 billion of venture capital and growth equity has been deployed to fintechs over the past five years, and this number is growing quickly. Still, the nature and extent of impact that fintechs have on the industry remains unclear.

Throughout this week’s Acquire or Be Acquired conference, bank CEOs talked about the continually changing nature of financial services — with fintech often front and center. For many, collaboration between traditional institutions and emerging technology firms bodes well for their future. Here, Bank Director’s FinXTech provides authoritative, relevant and trusted content to a hugely influential audience, specifically:

- Fintechs who view banks as potentially valuable channels or distribution partners;

- Banks looking to grow and/or innovate with fintech companies’ help and support; and

- Institutional investors, venture capitalists, state & federal regulators, government officials and academicians helping to shape the future of banking.

We designed FinXTech as a peer-to-peer resource that connects this hugely influential audience around shared areas of interest and innovation. As a host of FinTech Week in New York City this April 24 – 28 (along with Empire Startups), we bring together senior executives from banks, technology companies and investment firms from across the U.S. to shine a light on what is really generating top line growth and bottom line profits through partnerships, collaboration and investments.

Given the changing nature of banking today, this week-long event in New York City looks at the various issues impacting banks, non-banks and technology companies alike. So as we move towards FinTech Week in New York City, I invite you to follow me on Twitter via @AlDominick, FinXTech’s President, Kelsey Weaver @KelseyWeaverFXT, @BankDirector and our @Fin_X_Tech platform and/or check out the FinTech Week New York website for more.