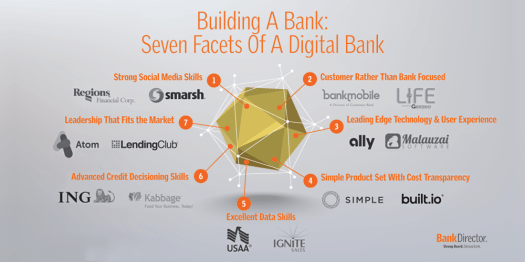

The fabric of the financial industry continues to evolve as new technology players emerge and traditional participants transform their business models. Through partnerships, acquisitions or direct investments, incumbents and upstarts alike have many real and distinct opportunities to grow and scale. If 2015 was all about startups talking less about disruption and more about cooperation, I see 2016 as the year that banks reciprocate.

By Al Dominick, President & CEO, Bank Director

Next Tuesday, at Nasdaq’s MarketSite in Time Square, our team hosts our annual “FinTech Day.” With so many new companies pushing their way into markets and product lines that traditionally have been considered the banking industry’s turf, we look at what fintech means for traditional banks. Likewise, we explore where emerging fintech players may become catalysts for significant change with the support of traditional players. When it comes to trends like the personalization of banking, the challenges of scaling a company in our highly regulated industry and what shifting customer expectations portend for banks and fintechs alike, we have a full day planned. Take a look at some of the issues we will address.

Riding The Wave Of Change

Al Dominick, President & CEO, Bank Director

Robert H. McCooey, Jr., Senior Vice President of Listing Services, Nasdaq

At a time when changing consumer behavior and new technologies are inspiring innovation throughout the financial services community, we open this year’s program with a look at how collaboration between traditional institutions and emerging technology firms bodes well for the future.

Banking’s New DNA

Michael M. Carter, CEO, BizEquity

Vivian Maese, Partner, Latham & Watkins

Eduardo Vergara, Head of Payments Services & Global Treasury Product Sales, Silicon Valley Bank

Moderated by: Al Dominick, President & CEO, Bank Director

With continuous pressure to innovate, banks today are learning from new challengers, adapting their offerings and identifying opportunities to collaborate. With this opening session, we focus on the most pressing issues facing banks as they leverage new tools and technologies to compete.

Who Has the Power to Transform Banking

Jeana Deninger, Senior Vice President, Marketing, CoverHound, Inc.

Brooks Gibbins, Co-Founder & General Partner, FinTech Collective

Colleen Poynton, Vice President, Core Innovation Capital

Moderated by: Al Dominick, President & CEO, Bank Director

While fintech startups continue to spearhead the technological transformation of financial services, recent efforts by systemically important financial institutions call into question who reallly has the power to tranform banking. From an investment perspective, recent market turmoil may put some opportunities on hold – while others now have a higher, sharper bar to clear. In this session, we talk to investors about the traits that they look for when backing a venture in the context of a changing economic environment.

Opportunities to Reinvigorate the Banking Industry

Tom Kimberly, General Manager, Betterment Institutional

Thomas Jankovich, Principal & Innovation Leader, US Financial Services Practice, Deloitte Consulting LLP

Pete Steger, Head of Business Development, Kabbage, Inc.

Moderated by: Al Dominick, President & CEO, Bank Director

Many fintech companies are developing strategies, practices and new technologies that will dramatically influence how banking gets done in the future. However, within this period of upheaval – where considerable market share will be up for grabs – ambitious banks can leapfrog both traditional and new rivals. During this hour, we explore various opportunities for financial services companies to reinvigorate the industry.

Opportunities to Financially Participate in Fintech

Joseph S. Berry, Jr., Managing Director, Co-Head of Depositories Investment Banking, Keefe, Bruyette & Woods, Inc. A Stifel Company

Kai Martin Schmitz, Leader FinTech Investment LatAm, Global FinTech Investment Group, International Finance Corporation

Moderated by: Al Dominick, President & CEO, Bank Director

While large, multinational banks have made a series of investments in the fintech community, there is a huge, untapped market for banks to become an early-stage investor in fintech companies. Based on the day’s prior conversations, this session looks at opportunities for banks to better support emerging companies looking to grow and scale with their support.

##

While this special event on March 1 is sold out, you can follow the conversations by using #Fintech16 @aldominick @bankdirector @finxtech and @bankdirectorpub. And as a fun fact, I’ll be ringing the closing bell next Tuesday flanked by our Chairman and our Head of Innovation. So if you are by a television and can turn on CNN, MSNBC, Fox, etc at 3:59, you’ll see some smiling faces waving at the cameras.