WASHINGTON, DC — With this week’s news that nCino is readying itself for an IPO, I thought to postulate about who “the next nCino” might be in the fintech space. By this, I mean the tech company about whom bank executives cite as doing right by traditional institutions.

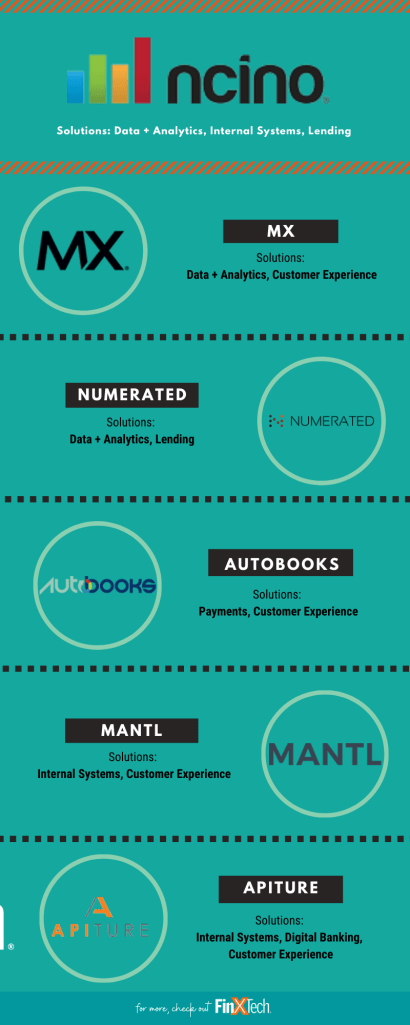

For context, nCino developed a cloud-based operating system for financial institutions. The company’s technology enables both customers and financial institutions to work on a single platform that’s optimized for both retail and commercial accounts. In simple terms, they provide everything from retail and commercial account opening to portfolio management for all of a bank’s loans.

In its IPO filing, the company says it works with more than 1,100 financial institutions globally — whose assets range in size from $30 million to $2 trillion. Personally, I remember their start and been impressed with their growth. Indeed, I’ve known about nCino since its early Live Oak Bank days. I’ve gotten to know many on their executive team, and just last Fall shared a stage with their talented CEO, Pierre Naudé, at our annual Experience FinXTech conference in Chicago.

So as I think about who might become “the next” nCino in bankers’ minds across the United States, I begin by thinking about those offering solutions geared to a bank’s interest in Security, leveraging Data + Analytics, making better Lending decisions, getting smarter with Payments, enhancing Digital Banking, streamlining Compliance and/or improving the Customer Experience. Given their existing roster of bank clients, I believe the “next nCino” might be one of these five fintechs:

While I have spent time with the leadership teams from each of these companies, my sense that they might be “next” reflects more than personal insight. Indeed, our FinXTech Connect platform sheds light on each company’s work in support of traditional banks.

For instance, personal financial management (PFM) tools are often thought of as a nice perk for bank customers, designed to improve their experience and meet their service expectations. But when a PFM is built with data analytics backing it, what was seen as a perk can be transformed into a true solution — one that’s more useful for customers while producing revenue-generating insights for the bank. The money management dashboard built by Utah-based MX Technologies does just that.

Spun out of Eastern Bank in 2017 (itself preparing for an IPO), Boston-based Numerated designed its offering to digitize a bank’s credit policy, automate the data-gathering process and provide marketing and sales tools that help bank clients acquire new small business loans. Unlike many alternative lenders that use a “black box” for credit underwriting, Numerated has an explainable credit box, so its client banks understand the rules behind it.

Providing insight is something that Autobooks helps small business with. As a white-label product that banks can offer to their small-business customers, Autobooks helps to manage business’s accounting, bill pay and invoicing from within the institution’s existing online banking system. Doing so removes the need for small businesses to reconcile their financial records and replaces traditional accounting systems such as Quickbooks.

The New York-based MANTL developed an account opening tool that comes with a core integration solution banks can use to implement this and other third- party products. MANTL allows a bank to keep its existing core infrastructure in place while offering customers a seamless user experience. It also drives efficiency & automation in the back-office.

Finally, Apiture’s digital banking platform includes features such as digital account opening, personal financial management, cash flow management for businesses and payments services. What makes Apiture’s business model different from most, though, is that each of those features can also be unbundled from the platform and sold as individual modules that can be used to upgrade any of the bank’s existing systems.

Of course, these are but five of hundreds of technology companies with proven track records of working with financial institutions. Figuring out what a bank needs — and who might support them in a business sense — is not a popularity contest. But I’m keen to see how banks continue to engage with these five companies in the months to come.